Willis Towers Watson’s Thinking Ahead Institute (TAI) recently revealed what it considers the 15-extreme risks facing investors for 2019, as well as for the years ahead. The risks run the gamut from climate change to nuclear contamination.

TAI’s research suggests, broadly, there are three hedging strategies available to institutions:

- Hold cash. Over long historical periods cash has held its real value through both episodes of deflation and inflation but there is no guarantee that this will be the case in the future.

- Derivatives. It is worth mentioning that cost and usefulness are often in opposition. The cost of derivatives protection can often be reduced by specifying more precise conditions – but the more precise the conditions, the greater the chance that they are not exactly met and hence the ‘insurance’ does not pay out.

- Hold a negatively-correlated asset. There is no single asset that will work against all possible bad outcomes. Further, there is no guarantee that the expected performance of the hedge asset will actually transpire in the future event.

While we have regularly discussed the“value of holding cash,” and “hedging” within portfolios, for most investors there are only a limited number of options available. The problem becomes magnified by the lack of capital, and a disciplined investment strategy, to delve into and manage more complex risk mitigation strategies. Therefore, investors are simply told to “buy and hold,” and hope for the best.

Since institutions are actively hedging capital risk, it should be clear “buy and hold” strategies do not. However, there are actions you can take to navigate not only short-term market risk, but also long-term fundamental, economic, and environmental risks.

Navigating the Risks

Many of the risks detailed in the TAI report are emotional in nature. For example, climate change is a very long-term issue but has become a political football for the upcoming election. While comments about the“world ending in 12 years” will certainly get headlines, they could also lead individuals into making emotionally based investment decisions that could negatively affect their financial wealth over the longer term.

So, what can you do?

All market cycles ultimately end. What causes those endings are often unexpected events that abruptly disrupt the financial markets.

Since the current bull market cycle has returned more than 300% from the financial crisis lows, it is quite likely that by going to cash today an individual would outperform someone who stayed invested in the years ahead. The next “mean-reverting event,” when it occurs, will destroy most if not all of the returns accumulated over the last decade. (That isn’t a theoretical assumption. It’s historical fact.)

It is true you can’t “time the market,” but you can manage risk by adjusting market exposure at times when risk outweighs the potential for further reward. What’s important to avoid is the “time loss” required to “get back to even.” In the long run, the mitigation of risk should allow the portfolio to reach your investment goals.

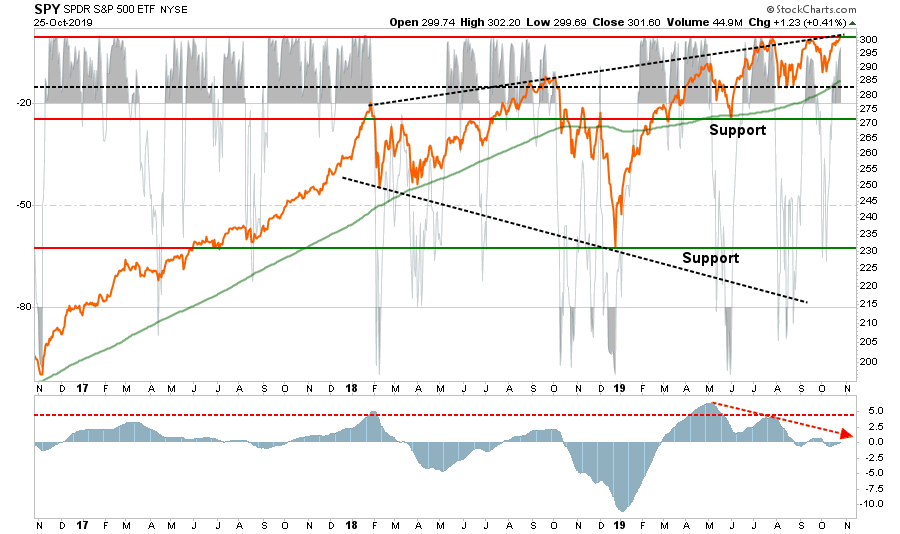

One way to visualize this is to use a moving average crossover as the trigger to increase or reduce exposure. The Timing Portfolio in the chart below is a simple switch between two assets. It invests in the Vanguard S&P 500 index when the market is above the 12-month moving average, and switches to the Vanguard Bond Fund when the market is below it. The Buy & Hold Portfolio stays 100% invested in the Vanguard S&P 500 for the duration. (You can run this backtest yourself at Portfolio Visualizer.)

It is very difficult for the average investor to manage a portfolio this way, but the chart shows the benefit of mitigating risk.

This is why we created RIAPro.net (Try FREE For 30-Days), where we provide investors with strategies for not only investment selection, but also risk management.

The same strategies we provide our subscribers, are what you can do to take control of your portfolio and investment related risk. Having a defined set of guidelines, and a disciplined investment process, can help reduce risk and create returns over time.

Here are the rules of thumb we follow in our management process at RIAPro.net.

- Cut losers short and let winner’s run. (Be a scale-up buyer into strength.)

- Set goals and be actionable. (Without specific goals, trades become arbitrary and increase overall portfolio risk.)

- Emotionally driven decisions void the investment process. (Buy high/sell low)

- Follow the trend. (80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

- Never let a “trading opportunity” turn into a long-term investment. (Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

- An investment discipline does not work if it is not followed.

- “Losing money” is part of the investment process. (If you are not prepared to take losses when they occur, you should not be investing.)

- The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

- Never, under any circumstances, add to a losing position. (As Paul Tudor Jones once quipped: “Only losers add to losers.”)

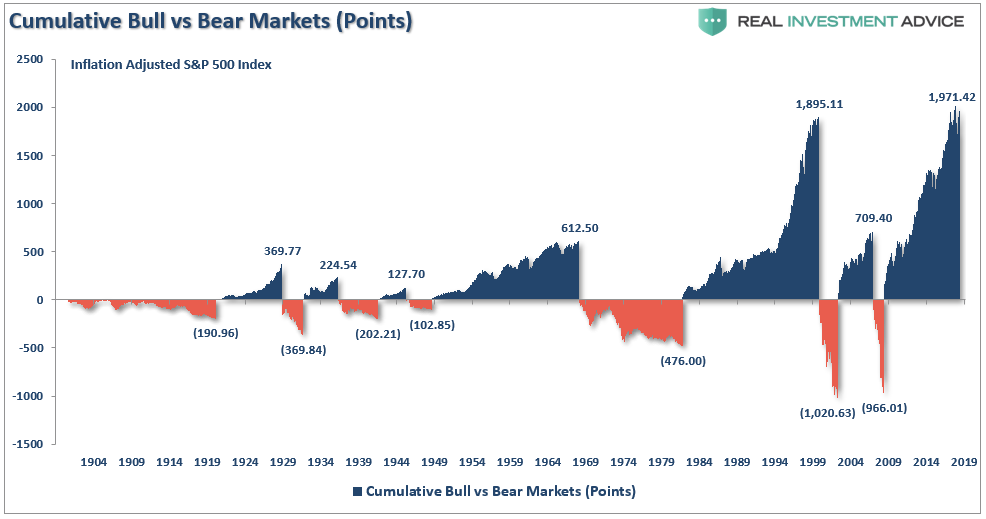

- Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short. (Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

- When markets are trading at, or near, extremes do the opposite of the “herd.”

- Do more of what works and less of what doesn’t. (Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

- “Buy” and “Sell” signals are only useful if they are implemented. (Managing a portfolio without a “buy/sell” discipline is designed to fail.)

- Strive to be a .700 “at bat” player. (No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

- Manage risk and volatility. (Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

We agree with Tim Hodgson’s conclusion:

“To navigate through this complex world, we suggest investors need to be open-minded, avoid concentrated risks, be sensitive to early warning signs, constantly adapt and always prepare for the worst.”

Investing is not a competition.

It is a game of long-term survival.