We’ve all been conditioned to think the balanced portfolio is a touchstone of investing. For many investors, it provides enough exposure to the stock market (60%) to produce a healthy return and enough exposure to the bond market (40%) to provide ballast and a little income to a portfolio. Along the way, advisors like to say that investors have counted on beating inflation by 4 or 5 percentage points. Supposedly.

But, as MarketWatch’s Brett Arends points out, a balanced portfolio hasn’t always performed as advertised, and the upcoming decade might be one of those times. That means investors should consider other allocations (depending on their individual circumstances, of course).

First, from 1938 to 1948, a balanced portfolio trailed inflation. Then, again, from 1968 through 1983, a balanced portfolio trailed inflation, eroding a third of its value in real terms, according to Arends. Basically, a balanced portfolio struggles against inflation. And while it’s obvious why inflation hurts bonds with their fixed dollar payments, it also tends to hurt stocks, despite their assumed ability to benefit from companies passing on higher costs to customers through price increases.

There aren’t easy ways for investors to combat inflation, if it should arise. Gold and commodities helped in the 1970s. Real estate can help too, as inflation can cause property price appreciation and push rents higher. Some foreign stock markets might help. Arends points out that Japanese and Singaporean stocks took off in the 1970s. Corporate bank loans and floating rate corporate debt might also help, though, Arends notes Ben Inker of Grantham, Mayo, van Otterloo (GMO) in Boston says credit protections aren’t what they once were. Finally, Inker notes that cash is a reasonable choice in times of inflation. And cash, as Arends says, doesn’t have to be in U.S. dollars. It can be in Swiss Francs, for example.

The 1970 also saw observers like Harry Browne advocate a different kind of portfolio mix – 25% each in cash, long-term bonds, stocks, and commodities. The cash and commodities would help in inflation, while the long-term bonds would help in times of deflation.

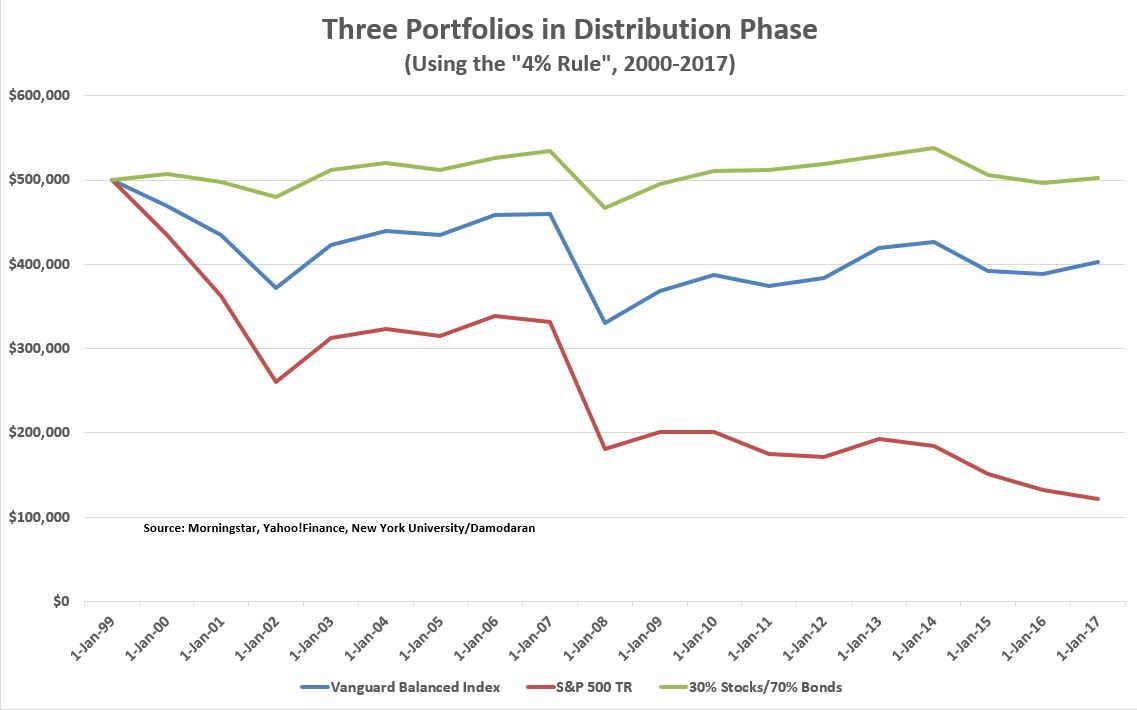

That leads me to the argument that, if you’re going to maintain a static portfolio allocation, something like 30% stock exposure, with the rest in short-term bonds and cash might be reasonable for someone about to retire soon. My reasons are that stocks are too volatile for a portfolio in distribution, and they’re likely too expensive to deliver good future returns in any case.

First, although I cherry-picked the start date so that two severe bear markets are baked into this hypothetical study, this portfolio in distribution phase shows that 30% stock exposure is better for a retiree in a bear market than a more aggressive portfolio. A balanced portfolio worked reasonably well, but only dropping down to 30% stocks allowed the portfolio to remain intact in a nominal sense (though not in an inflation-adjusted sense). Taking money from a portfolio during a volatile stock market is a tricky business. Too much stock exposure – even when using the famous “4% rule” (4% withdrawal the first year and 4% more than the first withdrawal annually thereafter) can destroy someone’s retirement.

Second, it’s not clear that stocks will outperform bonds over the next decade in any case. Even if you’re not in distribution phase, making volatility less of a concern, you may not add return to your portfolio by adding stock exposure. That’s because the Shiller PE (current price of stocks relative to past 10-year inflation-adjusted earnings) is over 30, meaning stocks have to remain more expensive than they have in history barring one other time for the next decade to deliver more than a 4% or 5% return.

And if you do add U.S. stocks to your portfolio, you’ll likely be adding the same old volatility stocks have delivered in the past. Modern academic finance like to use something called the Sharpe Ratio, which is a volatility-adjusted return or indicates how much return an investment achieved per unit of volatility. This view of the world has its problems, because risk might not be volatility, but it can be useful in helping you decide whether you want to add a certain asset to a portfolio or not. Getting, say, 4% or 5% annualized from stocks and assuming their historical volatility is a lot worse than getting the customary 10% from stocks and assuming their customary volatility. Adding U.S. stocks to a portfolio at current prices makes for what modern academic finance would call an inefficient portfolio.

Foreign stocks are cheaper than their U.S. counterparts, but they’re not screamingly cheap. If a balanced portfolio seems reasonable to you, it may not be under today’s circumstances. Consider trimming at least some of that stock exposure and adding a few other asset classes. Those new additions may not shoot the lights out, but, chances are, neither will U.S. stocks for the next decade. Above all, don’t think there’s some rule that says you need half your money in stocks. The idea of the balanced portfolio has become so popular that it feels like heresy to some people to deviate from it. But investing isn’t about faith; it’s about assessing the circumstances and likely returns in as rational a way as possible. Remember also to get some help from an adviser in constructing a portfolio and completing a financial plan. Many asset classes that weren’t available in the past to retail investors are available now. An experienced adviser can help you use them well and manage the risks they contain.