Leveraged-Loan Risks Are Piling Up

Rising interest rates have a peculiar effect.

US junk-bond issuance in June plunged 31% from a year ago to just $14.5 billion, the lowest of any June in five years, according to LCD of S&P Global Market Intelligence. During the first half of the year, junk bond issuance dropped 23% from a year ago to $110.6 billion.

Is investor appetite for risky debt drying up? Have investors given up chasing yield? On the contrary! They’re chasing harder than before, but they’re chasing elsewhere in the junk-rated credit spectrum: leveraged loans.

Leveraged loans are another way by which junk-rated companies can raise money. These loans are arranged by banks and sold either as loans or as Collateralized Loan Obligation (CLOs) to other investors, such as pension funds or loan funds. They’re a $1 trillion market and trade like securities. But the SEC, which regulates securities, considers them loans and doesn’t regulate them. No one regulates them.

In the first half, companies issued $274 billion of non-amortizing leveraged loans, and $97 billion in revolving and amortizing leveraged loans, according to LCD, for a total of $371 billion, on par with the record set in the first half last year.

This is well over triple the amount of junk bonds issued in same period ($110 billion).

Many of these loans have floating interest rates, typically pegged to the dollar-Libor. And in an investment environment where the Fed has been trying to push up interest rates, Libor has surged, and floating-rate loans, whose interest payments increase as Libor ratchets higher, are very appealing to investors – despite the additional risks these higher interest payments pose for the companies that are already struggling with negative cash flows. LCD:

The U.S. leveraged loan market, which is accessed by speculative grade debt issuers, has been exceedingly hot over the past two years or so as investors pour money into the asset class in anticipation of rate hikes by the Fed. Such moves usually boost interest in floating rate asset classes.

Given the “sustained investor appetite” for this type of debt, companies have been able to issue these loans with lower spreads over Libor, making it cheaper for companies to borrow – until rates rise further. That’s when this debt gets more expensive for these companies that already have a high debt load, often combined with money-losing operations – the combination that gives them a non-investment grade or “junk” credit rating (my cheat-sheet on credit rating scales).

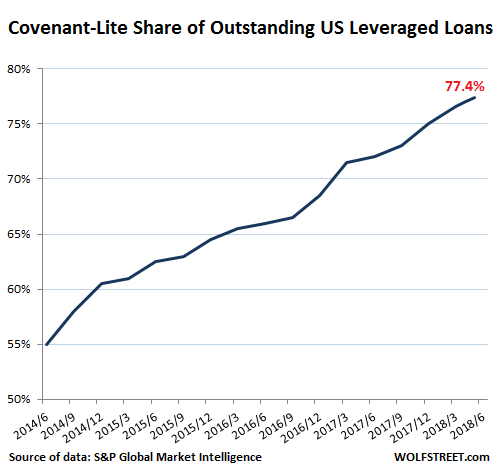

Leveraged loans come with covenants that are supposed to protect investors during the term of the loan and in case of default. With strong covenants and good collateral, leveraged loans tend to be less risky than junk bonds issued by the same company.

Alas, investors have the hots for this debt, and companies are taking advantage of it by weakening covenants, giving investors fewer protections and the company more leeway – such as paying interest with more debt rather than cash if it runs out of cash (payment-in-kind or PIK); normally, not being able to pay interest would constitute a default, but not with these “covenant lite” or “cov-lite” loans. The boom in cov-lite has started years ago and has surged to massive record proportions. When these loans default, investors are exposed to much greater losses.

As of the end of May, a record 77.4% of the $1 trillion in leveraged loans currently outstanding are cov-lite, the 13th month in a row of records, up from 55% in June 2014:

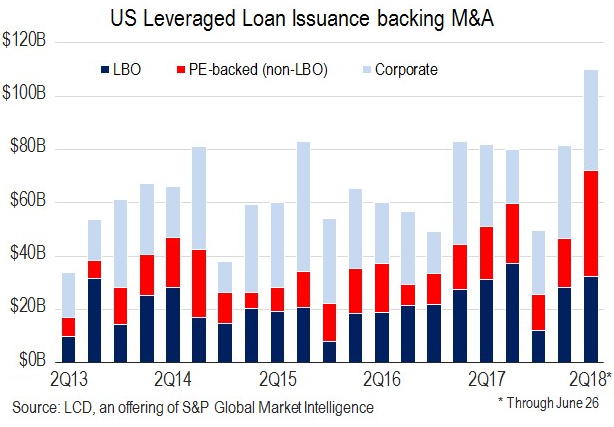

Financial Engineering Is Not MAGA—-Record Leveraged Loan Issuance In Q2 To Fund M&A