(Bloomberg) While U.S. homeowners may be celebrating their good fortune as home prices surge higher at a blistering 17% year-over-year clip, history suggests the end of quantitative easing will cool things off.

A healthy housing market wouldn’t exhibit the out-sized price increases seen of late. No mature market behaves this way unless an unusual exogenous factor is at work. In the case of housing, there are two of them.

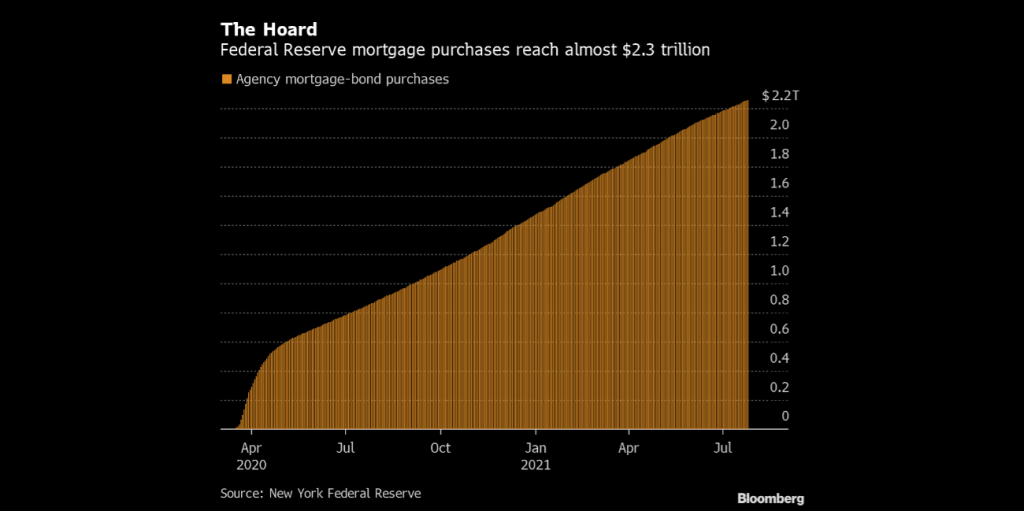

First is the Federal Reserve’s massive QE4 program, which in size and pace is a behemoth compared to the mortgage bond purchase programs seen during QE1 and QE3. This current QE alone now accounts for almost $2.3 trillion in mortgage bond purchases since March 2020, while the previous two QEs combined took down $2.75 trillion. The Fed now holds about 31% of the entire agency mortgage market on its balance sheet.

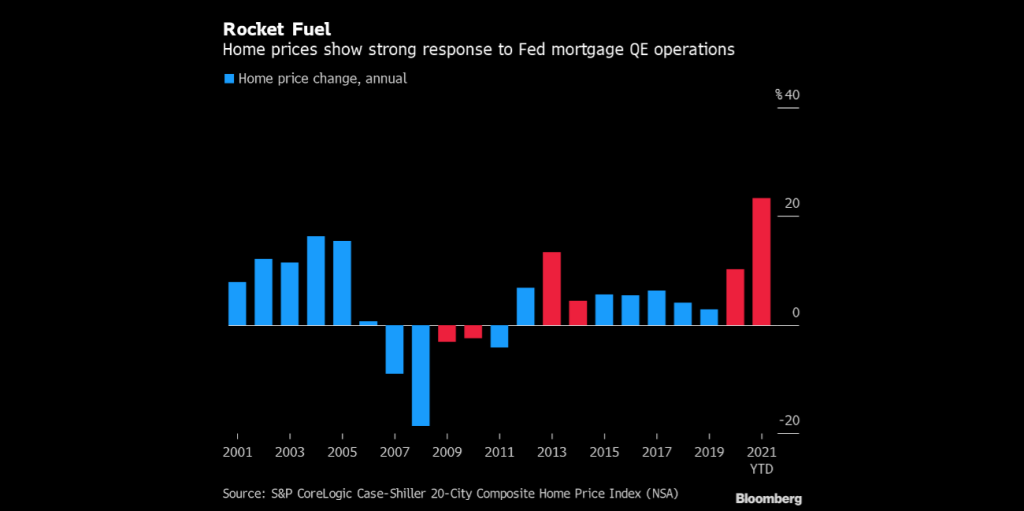

The situation is reminiscent of QE3, which ran from Sept. 2012 through Oct. 2014 and saw the central bank purchase $1.4 trillion in mortgages. Home prices, as measured by the S&P home price index, rose 6.9% in 2012, then exploded 13.4% higher in 2013 and jumped a further 4.4% in 2014. They had dropped 5.8% in 2011, before the Fed buying.

Home prices displayed much the same pattern during 2009 and 2010 after the Fed instituted QE1 from Nov. 2008 to Aug. 2010, purchasing $1.35 trillion during that time. While the cost of a home in 2007 and 2008 fell 9% and 18.6%, respectively, during 2009 and 2010 they dropped just 3.1% and 2.4%.

In this millennium, including the housing boom years of the early oughts, the average annual home price growth has been 5.2%. During the years with active Fed mortgage purchases, it has averaged 7.6%, compared to 4.2% during the years without.

The second outside force is the collapse in home building since around 2010, which has left the U.S. housing market desperately short of supply.

During the decade of 2010 to 2019, just 683,000 of new single-family homes were built on an annualized basis, the lowest level of any decade since the 1950s. Considering that the U.S. population of about 330 million is far larger than it was in the 1950s, this has had consequences.

The supply of existing homes for sale hit a record low of just over 1 million units in January, helping fuel the rise in prices. It has since moved higher to 1.25 million as of last month, yet this is still about half the trailing average of 2.4 million seen since 2000.

But developers can’t build new homes as quickly or as painlessly as the Fed can create credit. Once the Fed brings QE4 to a close, a home price downturn, let alone a price collapse, amid such a scarcity of supply seems to be out of the question.

The agency mortgage sector on Tuesday saw higher-coupon UMBS 30-year coupons outperform their lower-coupon counterparts despite a five-basis-point bull-flattening of the U.S. Treasury curve. This was all done on light volume, as most investors seem content to hold onto their cards prior to today’s FOMC rate announcement.

Trade desks were said to have remained relatively quiet for a second day, though the market saw more of an up-in-coupon move than on Monday, with the 3.5% through 4.5% coupons all displaying robust flows compared to their trailing five-Tuesday averages.

This week’s economic data releases include the FOMC rate decision today and pending home sales on Thursday.

Jerome, please call the white courtesy phone. The housing market is on fire!

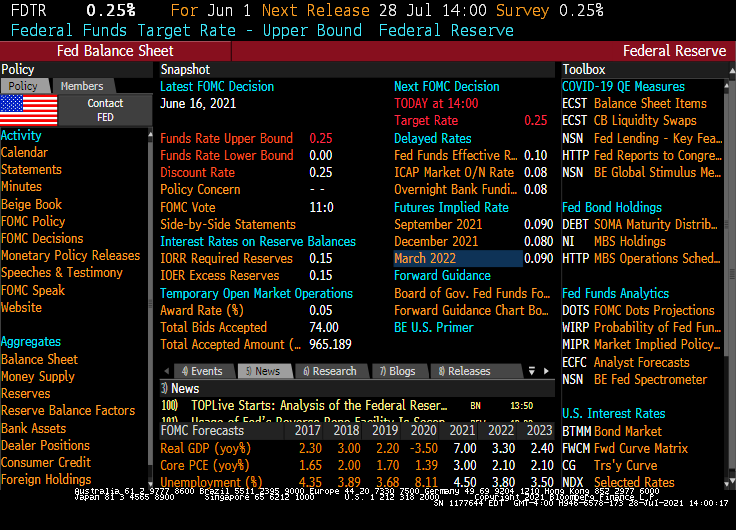

Update: No change in rates.

“Effective July 29, 2021, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 0 to 1/4 percent.

- Increase the System Open Market Account holdings of Treasury securities by $80 billion per month and of agency mortgage-backed securities (MBS) by $40 billion per month.

- Increase holdings of Treasury securities and agency MBS by additional amounts and purchase agency commercial mortgage-backed securities (CMBS) as needed to sustain smooth functioning of markets for these securities.

- Conduct overnight repurchase agreement operations with a minimum bid rate of 0.25 percent and with an aggregate operation limit of $500 billion; the aggregate operation limit can be temporarily increased at the discretion of the Chair.

- Conduct overnight reverse repurchase agreement operations at an offering rate of 0.05 percent and with a per-counterparty limit of $80 billion per day; the per-counterparty limit can be temporarily increased at the discretion of the Chair.

- Roll over at auction all principal payments from the Federal Reserve’s holdings of Treasury securities and reinvest all principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in agency MBS.

- Allow modest deviations from stated amounts for purchases and reinvestments, if needed for operational reasons.

- Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve’s agency MBS transactions.”