Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

What many in 2016 thought would never happen again is now reality.

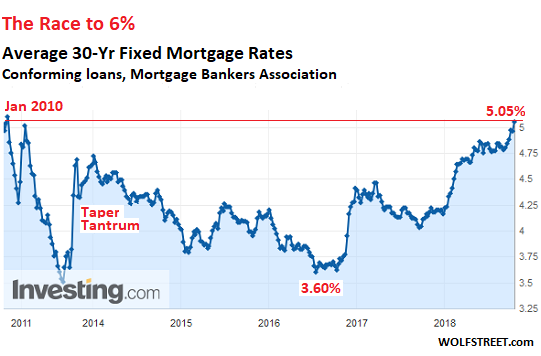

It finally happened – a line in the sand has been breached. The average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment did what people had thought in 2016 we’d never see again: It breached 5%.

It hit 5.05%, to be precise, for the week ending October 5, according to the Mortgage Bankers Association (MBA) this morning. This is the highest average rate since January 5, 2010 (chart via Investing.com):

This is likely not the pain-threshold for the housing market, though it is already putting pressure on it at the margin, with some potential buyers being scared off and other potential buyers finding the inflated home prices of today with the current mortgage rates outside their range of affordability. As interest rates have risen, some potential buyers have fallen by the wayside – though not a huge number just yet.

But 6% will likely be the pain threshold, in my estimates. It will block a considerable number of potential buyers from buying at current prices. Home prices would have to fall first.

If the maximum a household can afford is a mortgage payment of $1,720 a month, they can finance $320,000 over 30 years with a 5% fixed rate mortgage. But if the mortgage rate rises to 6%, they’re maxed out at $287,000. In other words, the price they can afford would drop by about 10% if the rate rises by 1 percentage point.

This principle goes for all budget-constrained buyers.

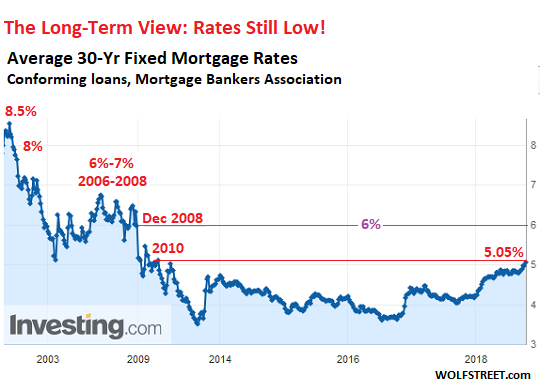

And 6% has moved into view. This is still historically low. It would take rates back to December 2008, when the Fed was kicking off its first round of QE to repress long-term rates and inflate asset prices. Beyond that are the now unimaginably high rates of 7% and 8%:

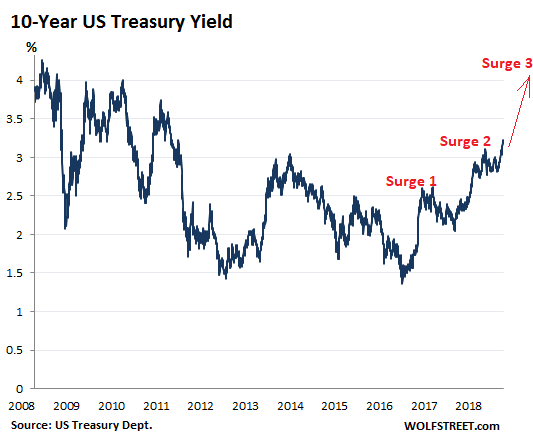

Mortgage rates move more or less in tandem with the 10-year Treasury yield, but are higher. The spread between the MBA’s average 30-year fixed mortgage rate and the 10-year yield runs around 1.5 to 2.0 percentage points over time. With today’s 10-year yield at 3.22%, the spread is 1.83 percentage points.

The 10-year yield has moved in two surges so far in this rate-hike cycle, each of them over 1 percentage point, with some back-tracking in between. It appears to have launched “Surge 3.” If it plays out, this surge would push the 10-year yield beyond 4%. And this would bring the 30-year fixed rate into the neighborhood of 6%.

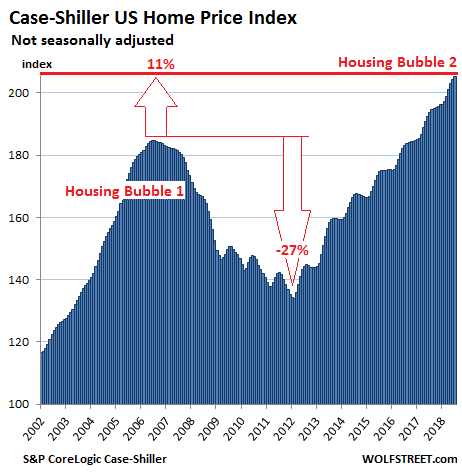

This new mortgage rate environment is meeting home prices across the US that have surged over the past years. Affordability issues, already tough to deal with at 4% and 4.5% and even tougher to deal with at 5%, are going to be much tougher at 6%.

But the Case-Shiller National Home Price Index averages out the booming housing markets with the lagging ones. Housing markets are local. And in many metros, home prices have surged far more than the national average. For example, according to my Most Splendid Housing Bubbles in America, these metros have seen the Case-Shiller index surge from the peak of Housing Bubble 1 in 2006/2007:

- Seattle, by 35%

- Denver, by 55%

- Dallas-Fort Worth, by 48%

- Portland, by 26%

- San Francisco Bay Area, by 41%

These price increases came on top of the crazy peaks of Housing Bubble 1. So a 6% average 30-year fixed mortgage rate in these inflated markets will likely change the equation a lot more than in some of the less inflated markets.