Just How Transitory Is Inflation?

Would you buy a five year CD paying 5%?

We would be shocked if anyone answers “no.” On a relative basis, versus other fixed-income options, a 5% FDIC guaranteed CD is a no-brainer. However, to properly evaluate the CD or any investment, we need to factor in inflation expectations. If inflation for the next five years is 10%, the no-brainer CD will be a bust.

The pandemic is easing, and the winds of recovery are roaring at the economy’s back. Pent-up demand and the remnants of stimulus are driving robust economic growth. At the same time, the ability to produce and deliver goods remains greatly hampered. The result is inflation, the likes of which have not been seen in over a decade.

Making inflation forecasting even harder is considering how past and future monetary and fiscal stimulus might affect prices.

Assumptions based on prior periods may prove right but may also be a recipe to lose 5% on a 5% CD. Given such a unique environment, we must be suspicious of confident media and Wall Street inflation narratives.

This is a time where we must think for ourselves. To help you, we break down the 336 components and subcomponents of CPI to better appreciate what is driving the current inflation rate. In turn, this will prove helpful in thinking about future inflation rates.

CPI Summary

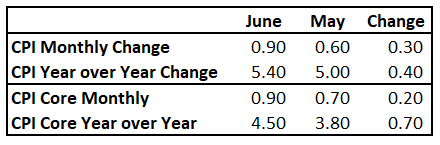

On July 13, 2021, the BLS released the June CPI report. The following table shows the headline results for the report.

June’s prices climbed well above May’s levels, as well as almost all economists’ expectations. The monthly CPI change of +0.9 equates to an approximate 11% annualized rate. For those old enough to remember, the report brought back nightmares from the 1970s.

Since 1990, there are only three other months in which the monthly rate rose by 0.9% or more. The 5.4% year-over-year rate of inflation is the largest in over a decade.

Digging Into Cupcake and Biscuit Prices

The information below is from the most granular details within the CPI Index. For example, the Food category comprises 13.9% of CPI. Over half of it is Food at Home. One component of Food at Home is Cereals. Within Cereals are flour, breakfast cereal, rice/pasta/cornmeal, bread, biscuits/rolls/muffins, cakes/cupcakes/cookies, and a catch-all other category.

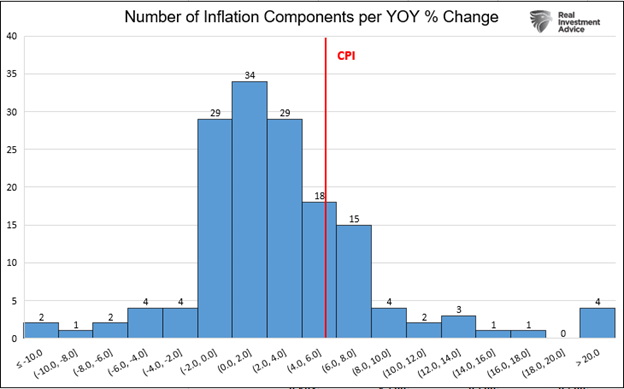

The following analysis dives into cupcakes, biscuits, and the other 153 products and product groupings compromising CPI.

The distribution graph below shows the 153 products sorted by their respective year-over-year change in 2% increments. As shown, over 75% of the constituents are below the +5.4% year-over-year change in CPI (red line). 28% of the year-over-year changes were negative. On a monthly basis, not shown, 69% are below the monthly CPI change (+0.9%).

The right-most column shows four subcomponents whose prices have risen by at least 20% in the last year. They are as follows:

- Used Cars 45.2%

- Gasoline +45.1%

- Fuel Oil +44.5%

- Other Motor Fuels +32.1%

The left-most column shows two subcomponents whose prices have fallen by 10% or more. They are as follows:

- Food at employee sites and schools (cafeteria food) -29.9%

- Telephone hardware, calculators, and other information items -17.8%

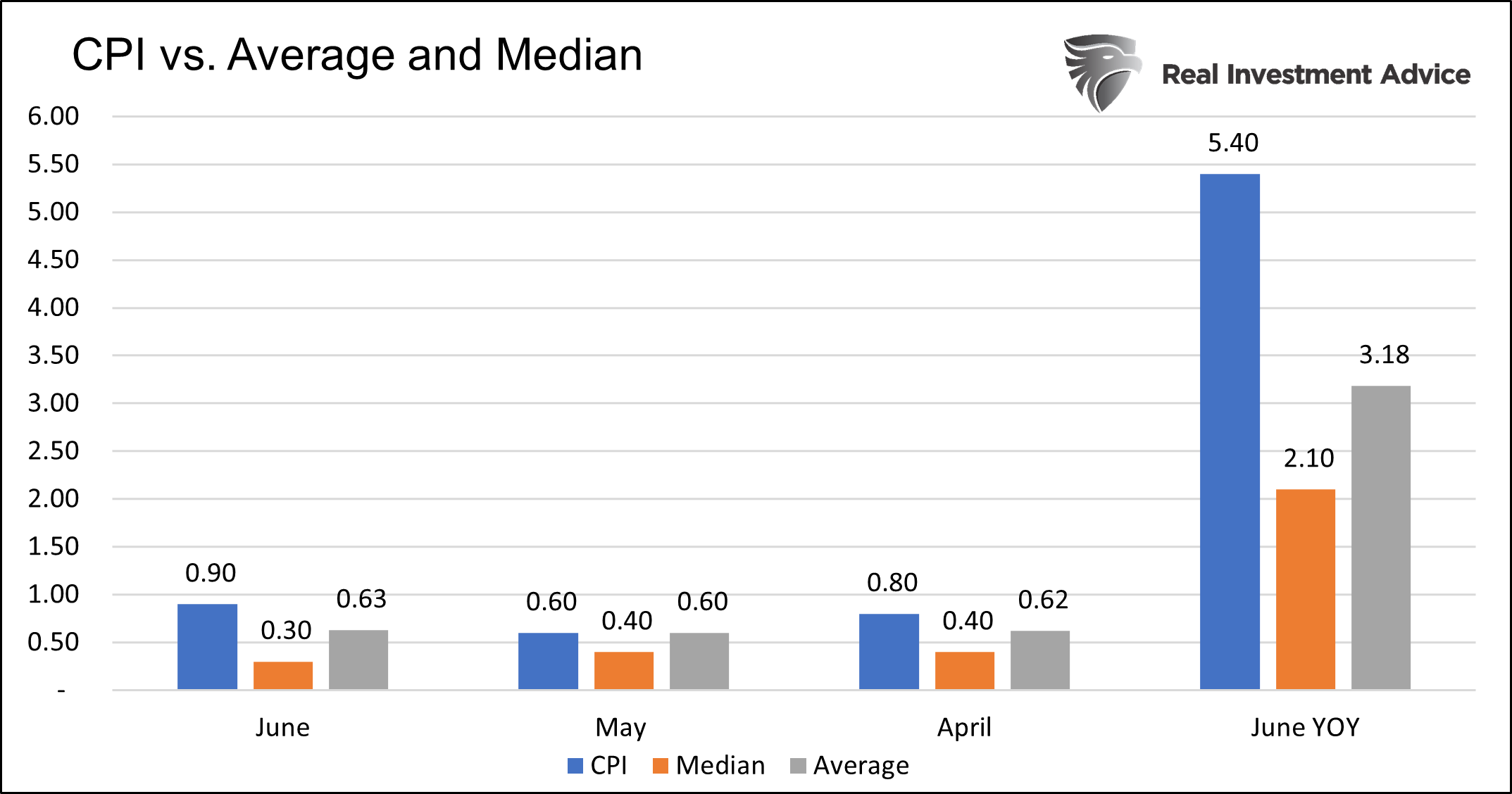

The following bar chart breaks down the last three monthly data points and most recent year-over-year data to show how the CPI index stacks up against the average and median of the underlying data.

Price increases for most subcomponents are not overly concerning. The median inflation rate based on 153 goods is +3.6% annualized or 1.8% less than the CPI Index.

Contribution Analysis

While the data above helps us appreciate inflation, at least not yet, is not a widespread problem, it does not account for how we spend money. The BLS assigns a weighting for each good when calculating CPI.

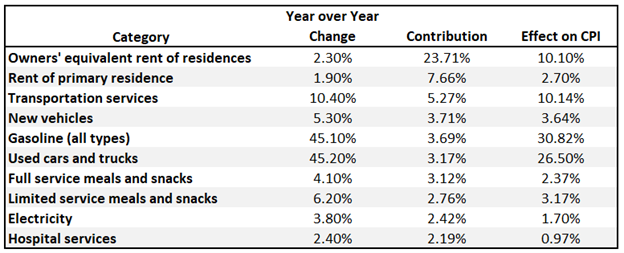

The table below shows the categories accounting for more than 2% of the CPI Index. While only constituting about 5% of the number of categories, these ten components account for over 50% of the CPI Index and almost 90% of June’s increase in CPI.

Gasoline and used cars alone are responsible for half of the year-over-year change in CPI. Transportation services, such as auto insurance, vehicle maintenance, and airline fares rose over 10%. While smaller price increases than gasoline and used cars, transportation has nearly twice the two products’ weighting.

Shelter constitutes about a third of CPI. Shelter is comprised of owners’ equivalent rent (OER), which attempts to value housing and rental prices. Both measures were tame at 2.3% and 1.9%, respectively.

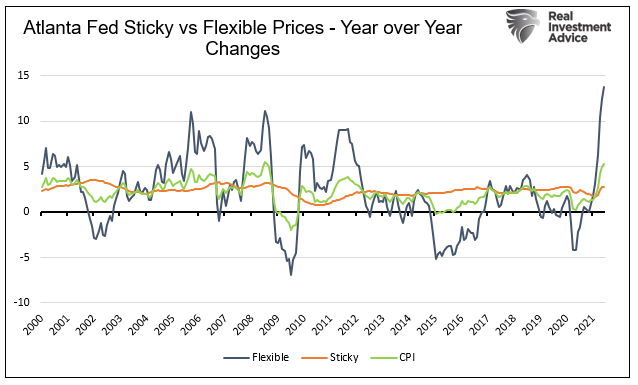

Sticky versus Flexible Prices

To forecast future inflation, it’s beneficial to understand which prices are sticky and which are flexible.

Sticky prices change infrequently. However, when they increase, they tend to stick, so to speak. Examples include education, communication services, and motor vehicle insurance. Flexible prices oscillate over time. Examples include gasoline, fruits and vegetables, and car rentals.

The Atlanta Fed distributes a sticky and flexible price index. The index constituents and explanation of each index is found HERE.

The graph below charts the Fed’s sticky and flexible price indexes. Not surprisingly, the sticky index is stable, and the flexible index is volatile. Changes in CPI tend to be heavily correlated with the flexible index and not so much with the sticky index. Since 2012 the correlation between the flexible index and CPI is 96%. The sticky index and CPI only have a 30% correlation.

Given the flexible index drives CPI, we look at the four largest contributors to the June surge in CPI. We want to understand if they are flexible or sticky prices and assess their likelihood of reverting to pre-pandemic levels.

If prices are unchanged in the future for these goods, the rate of inflation will gravitate toward zero. If they fall in price, they will exert negative pressure on CPI.

The following four components, detailed below, account for 76% of the recent increase in CPI. Let’s review whether they are sticky or flexible, as well as expectations for future price changes.

Shelter (OER and rent)

Shelter is by far the most important factor in the CPI Index. OER, accounting for most of shelter prices, are only up 2.3% versus last year. The smaller subcomponent, rent, is up even less at 1.9%.

Shelter prices tend to be sticky. Other than the 2008 financial crisis and the Great Depression, the U.S. never really experienced a meaningful decline in national housing values. While the BLS’s OER price measure is tame, house prices are not. The well followed Case-Shiller home price index is up 17% year over year. Rental prices are also picking up.

Per Apartment List “So far in 2021, rental prices have grown a staggering 9.2 percent. To put that in context, in previous years growth from January to June is usually just 2 to 3 percent.”

Our concern is CPI Shelter Index catches up to reality, providing a significant boost to inflation in the months ahead. Further, given shelter tends to be sticky, a reversal in prices is less likely.

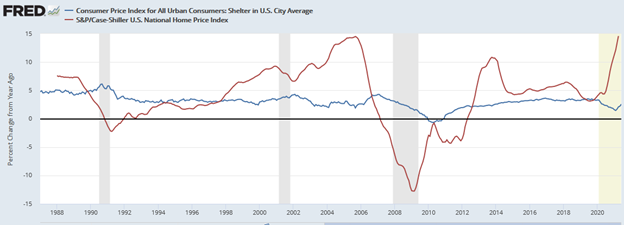

All that said, the correlation between the reality of house and rent prices and the CPI shelter levels is weak.

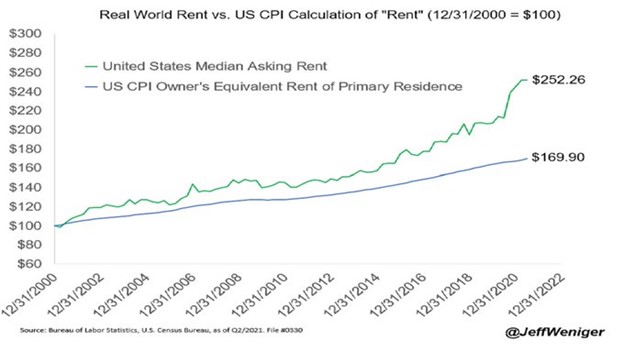

The graph below shows little correlation between CPI Shelter prices and the Case-Shiller Index. The CPI index trends from the housing boom of 2000-2007 are not much different than periods before and after. The second graph shows the disconnect between actual rent and the CPI’s calculation of owners’ equivalent rent.

Transportation Services

Transportation services have a 5.27% weighting in CPI but account for about 10% of the recent increase in CPI. Of note in this category is car and truck rental prices rising 87% versus last year. Motor vehicle insurance is up 11.3%, and public transportation, including airfare, is up 17%.

Most of the line items in this broad category are flexible. Airfares, accounting for .74% of CPI, are much higher today than last year because air travel was dead last year. The same story holds for auto rentals. Further, due to a lack of supply, auto rental chains sharply increased prices versus those before the pandemic. As the shortage of cars abate, rental prices should follow.

Also, pandemic related, many insurance customers received discounts last year since they did not drive as much as usual. Those discounts are expiring, resulting in what amounts to temporary price increases.

This sector was heavily affected by the pandemic and unease with travel. As the economy normalizes, we expect most prices in this category to revert to historical norms. This sector will likely provide a deflationary pull on CPI in the future.

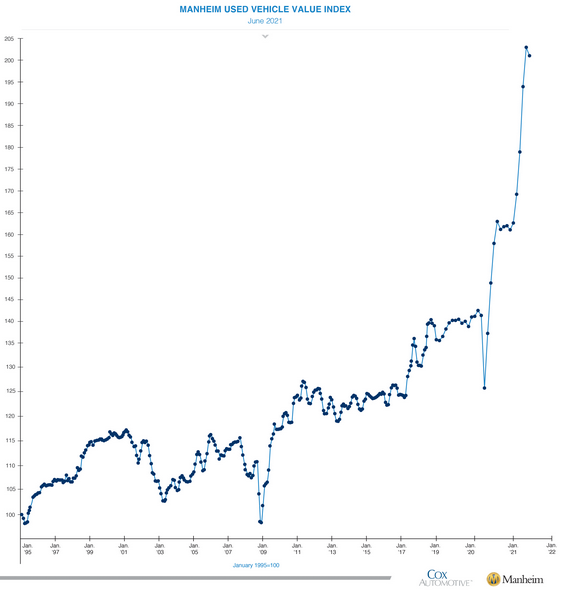

Used Cars

There is a severe shortage of used cars related to the pandemic. The graph below shows the resulting surge in the Manheim Used Car price index.

Once the chip shortage and other problems reducing the production of new cars abate, used cars will become more plentiful. At such time, likely in the next six to nine months, used car prices will plummet. While car prices tend to be sticky, we believe the recent aberration in used car prices will not hold. As we have seen, despite a small contribution, used car prices can have a significant effect. The same math will hold when prices correct as well.

Gasoline

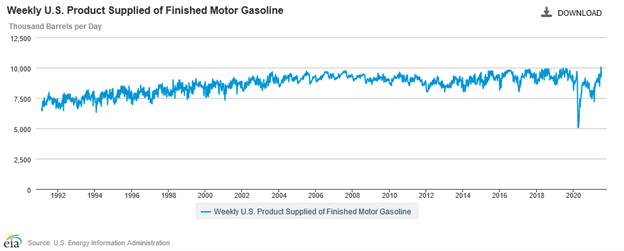

Gasoline and energy, in general, are the wildcard in any inflation forecast. Energy accounts for 7.1% of CPI, and gasoline is over half of that. Gas prices are highly flexible. They typically oscillate with economic growth and oil production. OPEC production is still limited although increasing, and U.S. Shale production remains slow to come back online. At the same time, demand, as measured by the amount of product supplied, fully recovered.

If energy prices sustain current levels, the incentive to produce will increase and result in downward price pressures. A natural slowing of economic activity will potentially reduce demand.

We think gasoline and oil prices generally are likely to stay near current levels but risk price reductions. As such, the contribution from higher gasoline prices will decline significantly.

Future Inflation

We think the current inflationary surge is temporary. When flexible prices, especially some of those mentioned, normalize, inflation is likely to follow suit. This is an uneasy forecast. The following are key factors that can prove us wrong:

- Shelter, accounting for a third of CPI, starts rising in line with house and rent prices.

- Wages continue to gain momentum, further increasing demand for goods while the supply and production lines are not fully operational.

- Round after round of fiscal stimulus continues, further driving demand.

- An inflationary mindset infiltrates consumer behavior. If people think prices will rise in the future, they are more likely to spend at today’s “cheaper” prices, again driving demand.

Summary

We remind ourselves daily to be humble as we are in unchartered territory. Trying to predict the future in normal times is hard enough. Trying to predict it today with so many unparalleled factors is fraught with risk.

All we can do is follow the data, watch for emerging trends, and track consumer behavioral trends closely. While we believe that recent price increases are temporary, we are not wed to that forecast. Importantly, neither are our investment decisions.

Review inflation one day at a time and take everyone’s inflation forecast with a grain of salt.