Last week, I discussed the Fed’s recent comments suggesting they might be closer to cutting rates and restarting “QE” than not.

“In short, the proximity of interest rates to the ELB (Effective Lower Bound) has become the preeminent monetary policy challenge of our time, tainting all manner of issues with ELB risk and imbuing many old challenges with greater significance.

“Perhaps it is time to retire the term ‘unconventional’ when referring to tools that were used in the crisis. We know that tools like these are likely to be needed in some form in future ELB spells, which we hope will be rare.”

After a decade of zero interest rates and floods of liquidity by the Fed into the financial markets, it is not surprising the initial “Pavlovian” response to those comments was to push asset prices higher.

However, as I covered in my previous article in more detail, such an assumption may be a mistake as there is a rising probability the effectiveness of QE will be much less than during the last recessionary cycle. I also suggested that such actions will drive the 10-year interest rate to ZERO.

Not surprisingly, those comments elicited reactions from many suggesting that rates will rise sharply as inflationary pressures become problematic.

I disagree.

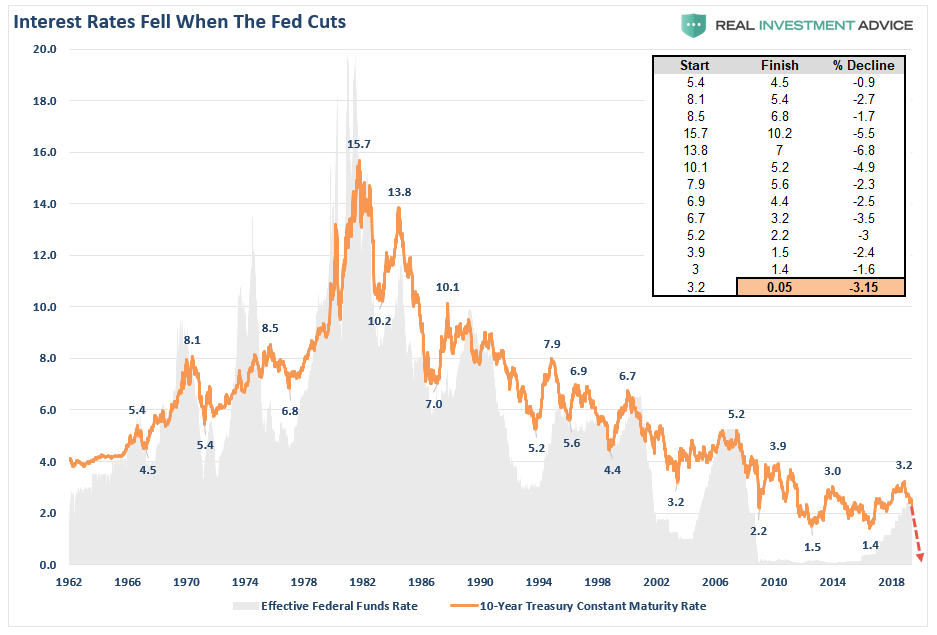

First, there is no historical evidence that is the case. The chart below shows that each time the Fed embarks upon a rate reduction campaign, interest rates have fallen by 3.15% on average.

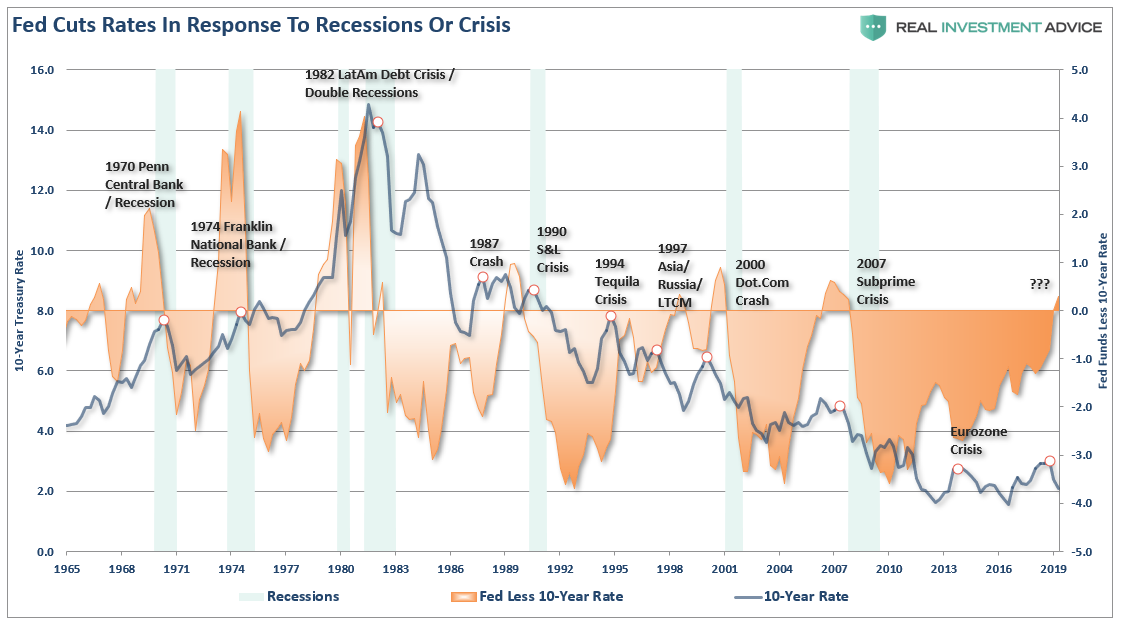

Of course, we need to add some context to the chart above. Historically, the reason the Fed cuts rates, and interest are falling, is because the Fed has acted in response to a crisis, recession, or both. The chart below shows when there is an inversion between the Fed Funds rate and 10-year Treasury it has been associated with recessionary onset.

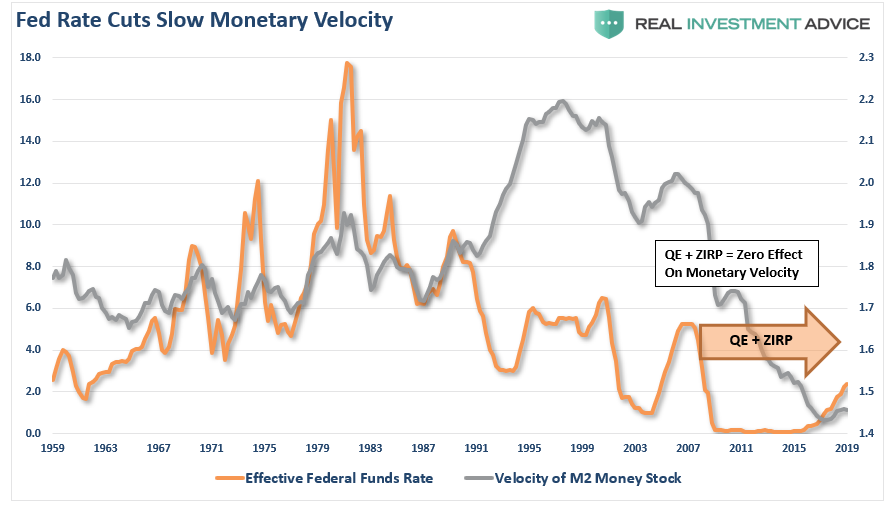

Secondly, after a decade of QE and zero interest rates inflation, outside of asset prices, (as measured by CPI), remains muted at best. The reason that QE does not cause “inflationary” pressures is that it is an “asset swap” and doesn’t affect the money supply or the velocity of money. QE remains confined to the financial markets which lifts asset prices, but it does not impact the broader economy.

Since 2013, I have laid out the case, repeatedly, as to why interest rates will not rise. Here are a few of the most recent links for your review:

- March 28, 2019 – The Bond Bull Market

- December 24, 2018 – Why Gundlach Is Still Wrong About Higher Rates

- October 11, 2018 – The Upcoming Bond Bull Market

- April 20, 2017 – Why Bonds Aren’t Overvalued

- March 23, 2017 – The Long View – Rates, GDP & Challenges

- October 24, 2016 – End Of The Bond Bull, Better Hope Not

- August 30, 2016 – Why Interest Rates Are Going To Zero

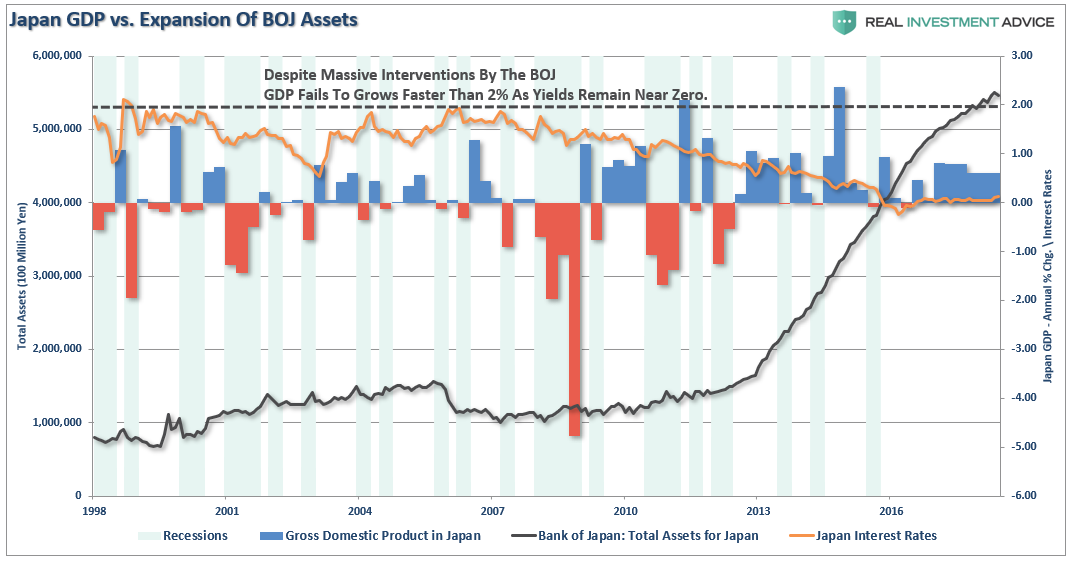

As I said, I have been fighting this battle for a while as “everyone else” has remained focused on the wrong reasons for higher interest rates. As I stated in “Let’s Be Like Japan:”

“This is the same liquidity trap that Japan has wrestled with for the last 20 years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

- A decline in savings rates to extremely low levels which depletes productive investments

- An aging demographic that is top heavy and drawing on social benefits at an advancing rate.

- A heavily indebted economy with debt/GDP ratios above 100%.

- A decline in exports due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

The lynchpin to Japan, and the U.S., remains interest rates. If interest rates rise sharply it is effectively “game over” as borrowing costs surge, deficits balloon, housing falls, revenues weaken, and consumer demand wanes. It is the worst thing that can happen to an economy that is currently remaining on life support.”

This last bolded sentence is the most important and something that Michael Lebowitz discussed in “Pulling Forward:”

“Debt allows a consumer (household, business, or government) to pull consumption forward or acquire something today for which they otherwise would have to wait. When the primary objective of fiscal and monetary policy becomes myopically focused on incentivizing consumers to borrow, spend, and pull consumption forward, there will eventually be a painful resolution of the imbalances that such policy creates. The front-loaded benefits of these tactics are radically outweighed by the long-term damage they ultimately cause.”

Unfortunately, the Fed is still misdiagnosing what ails the economy, and monetary policy is unlikely to change the outcome in the U.S., just as it failed in Japan. The reason is simple. You can’t cure a debt problem with more debt. Therefore, monetary interventions, and government spending, don’t create organic, sustainable, economic growth. Simply pulling forward future consumption through monetary policy continues to leave an ever growing void in the future that must be filled. Eventually, the void will be too great to fill.

Doug Kass made a salient point as well about the potential futility of Fed actions at the wrong end of an economic cycle.

“Pushing on a string is a metaphor for the limits of monetary policy and the impotence of central banks.

Monetary policy sometimes only works in one direction because businesses and household cannot be forced to spend if they do not want to. Increasing the monetary base and banks’ reserves will not stimulate an economy if banks think it is too risky to lend and the private sector wants to save more because of economic uncertainty.

This cycle is much different than previous cycles as there are a host of anomalous conditions that will work against the likely rate cuts that lie ahead.

What has occurred in the last decade?

- $4 trillion of QE

- $4 trillion of corporate debt piled up

- $4 trillion of corporate buybacks

- A Potemkin-like expansion in earnings per share as the share count drops to a two decade low. (h/t Rosie)

- Meanwhile, capital spending has failed to revive (leading to negative productivity growth).

While this is not a short term call for an imminent drop in the equity market, if my concerns are prescient and fully realized we will likely see more than the process of a market making a broad and important top.

The Fed is pushing on a string.”

Monetary policy is a blunt weapon best used coming out of recession, not going into one.

Unfortunately, as Caroline Baum penned for MarketWatch recently, the Fed has little to work with at this juncture.

“No one is disputing the idea that the Fed needs additional tools at a time when the benchmark rate (2.25%-2.5%) is already low and offers little room for traditional stimulus. Historically, the fed funds rate has been reduced by 5 percentage points, on average, to combat recessions, according to Harvard University economist Lawrence Summers.

As Eberly, Stock and Wright note in their paper, when the policy rate is close to zero, it ‘imposes significant restraints on the efficacy of Fed policy, and our estimates suggest that those constraints are only partially offset by the new slope policies.’”

I am not disputing that dropping rates and restarting QE won’t work at temporarily sustaining asset prices, but the reality is that such measures take time to filter through the economy. The impact of hiking rates 240 basis points over the last couple of years are still working their way through the economic system combined with the impact of tariffs on exports and consumption.

The real concern for investors, and individuals, is the real economy. We are likely experiencing more than just a “soft patch” currently despite the mainstream analysts’ rhetoric to the contrary. There is clearly something amiss within the economic landscape and the ongoing decline of inflationary pressures longer term is likely telling us just that. The big question for the Fed is how to get out of the “liquidity trap” they have gotten themselves into without cratering the economy, and the financial markets, in the process.

Should we have an expectation that the same monetary policies employed by Japan will have a different outcome in the U.S? This isn’t our first attempt at manipulating cycles. (H/T Doug)

“Governor Eccles: ‘Under present circumstances, there is very little, if anything, that can be done.’

Congressman T. Alan Goldsborough: ‘You mean you cannot push a string.’

Governor Eccles: ‘That is a good way to put it, one cannot push a string. We are in the depths of a depression and…, beyond creating an easy money situation through reduction of discount rates and through the creation of excess reserves, there is very little, if anything that the reserve organization can do toward bringing about recovery.’– House Committee on Banking and Currency (in 1935)

More importantly, this is no longer a domestic question – but rather a global one since every major central bank is now engaged in a coordinated infusion of liquidity. The problem is that despite the inflation of asset prices, and suppression of interest rates, on a global scale there is scant evidence that the massive infusions are doing anything other that fueling asset bubbles in corporate debt and financial markets. The Federal Reserve is currently betting on a “one trick pony” which is that by increasing the “wealth effect” it will ultimately lead to a return of consumer confidence and a fostering of economic growth?

Currently, there is little real evidence of success.

Nonetheless, we can certainly have some fun at the Fed’s expense. My colleague Mike “Mish” Shedlock did a nice summation of the “Powell’s Pivot.”

Bubbles B. Goode from Mike “Mish” Shedlock on Vimeo.