This past weekend in the NYTimes, Nobel-laureate economist Robert Shiller sounded the alarm on housing again. For those who don’t know, Shiller called the stock market bubble of the late 1990s and the housing bubble of the following decade. He is famous for his house price index and for his method of stock market appraisal called the “Shiller PE,” which judges price relative to past 10-year average real earnings, even if this latter metric comes from the great market analyst Benjamin Graham.

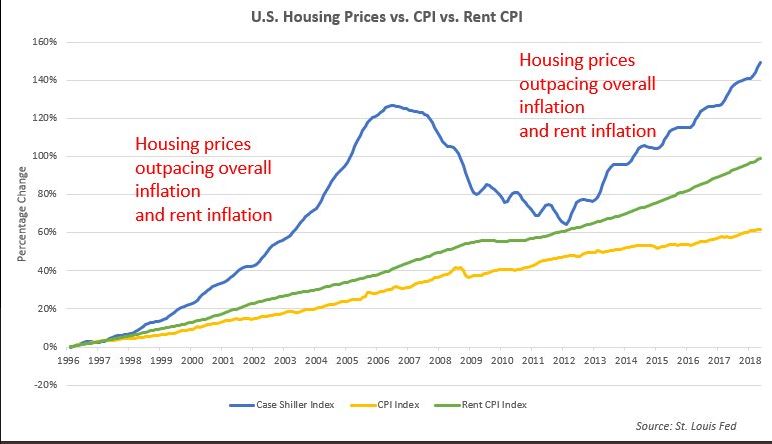

Shiller doesn’t use the word “bubble” in his article, but he argues that since around 2012 we have been experiencing one of the great housing booms in history. And this one is on the heels of the previous great boom and bust. (The third and more benign boom coincided with the great post-war Baby Boom).House prices are now 53% higher than they were in early 2012, meaning they have appreciated at least 7% annualized. Inflation, measured by CPI, since 2012? Less than 2%. That’s a big gain on CPI-adjusted grounds. The excellent graphic below from my colleague, Jesse Colombo, in a Forbes article, tells the price-CPI discrepancy story.

How is it that house prices can surge higher than inflation when median household income is mostly stagnant? Shiller places great importance on the psychological aspects of large price movements. He doesn’t think single economic factors typically tell the story — or the whole story. Therefore, he is skeptical that low interest rates are the primary cause of home price increases. There is some merit to blaming low rates, according to Shiller, and they have been present at the last two bubbles, but rates have actually been going up since 2012, while prices have continued to surge. As Shiller puts it, “The housing market does not react as directly as you might expect to interest rate movements. Over the nearly seven years of the current boom, from February 2012 to the present, all major domestic interest rates have increased, not decreased. So, while interest rates have been low, they have moved the wrong way, yet the boom has continued.”

Another possible explanation is economic growth. But house prices didn’t surge from 1950 through 2000 despite GDP roaring ahead sixfold during that time. And it’s not quite correct either to say prices are normalizing, because they are higher now than at the bubble peak.

Perhaps the home price increases are now a self-fulfilling prophesy, says Shiller. In other words, prices have been going up so people expect them to keep going up. Shiller quotes Keyenes saying, “people seem to have a “simple faith in the conventional basis of valuation.” If the conventional basis is now that home prices are going up 5 percent a year, then sellers, who would otherwise have no idea what to ask for their houses, will just put a price based on this convention. And likewise buyers will not feel they are paying too much if they accept the convention. In the United States, we may believe that the process is all part of the “American dream.”

The price surge can’t go on forever, but Shiller explains that nobody knows when it will stop. All we know now is that prices have surged as they have only two other times in recorded history. Let buyers and sellers beware. And if you have questions on our views of stock and bond markets, please contact us here.