Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

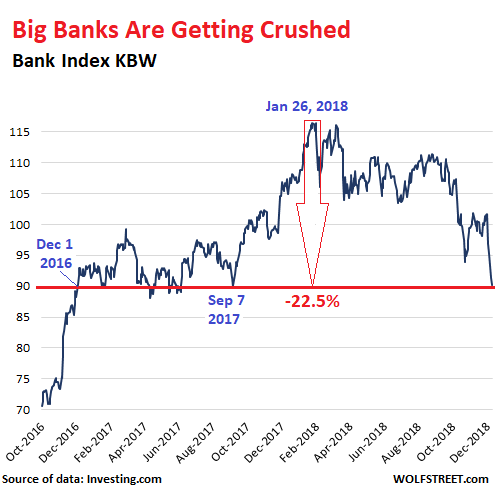

On Tuesday, the US KBW Bank index, which tracks the largest 24 US banks and serves as a benchmark for the banking sector, dropped 1.2%, the fifth day in a row of declines, to the lowest close since September 7, 2017.The index is now back where it had been on December 1, 2016. Two years of big gains gone up in smoke. The past five trading days looked like this:

- Dec 11: -1.2%

- Dec-10: -2.1%

- Dec 07: -2.0%

- Dec 06: -1.6%

- Dec 05: -4.9%

But no, the index doesn’t include Goldman Sachs – which is big in other ways but not as a bank, and which has skidded 35% from its all-time peak in February. The index has now dropped 22.5% since the post-financial crisis peak on January 26:

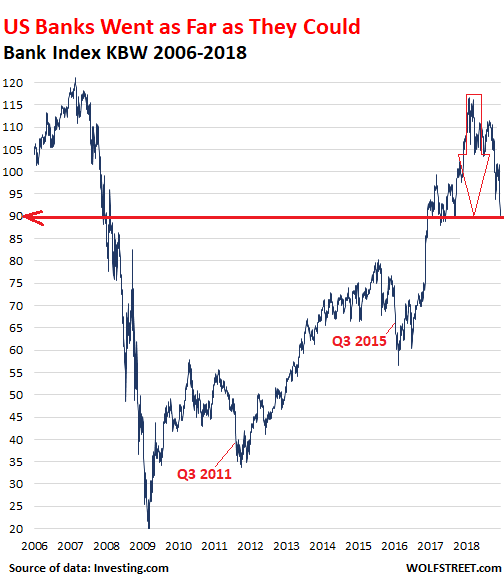

So far in Q4, the index has dropped 14%. Unless a miraculous banking-Santa-Claus rally pulls banks out of their dive by the end of the quarter, a 14% decline would make it the worst quarterly decline since Q3 2011. If tax selling kicks in, given the losses bank-stock investors have taken so far this year, it could get worse in the coming days.

Not even in Q3 2015, during the oil bust, when investors were fearing that banks would take steep losses on their loans to the oil industry, did shares drop this much.

The index is now back where it had first been a couple of years before its crazy peak in February 2007. Said peak occurred about a year before Bear Stearns toppled. During the subsequent collapse of banks stocks, it looked like the index would hit zero.

After the bottom in March 2009, the Fed’s strategies to benefit the banks and those that owned them took hold, at the expense of depositors and other classes of US stake holders, such as renters or future home buyers. And it worked. But that era is now over. And the tax cut too has been baked in, and banks are left to fend for themselves:

Big banks are heavily exposed to business debt, and business debt, which includes commercial real estate debt, has ballooned to record levels, while credit quality has deteriorated. The Fed, in its recent Financial Stability Report, pointed out this issue as a major risk to financial stability.

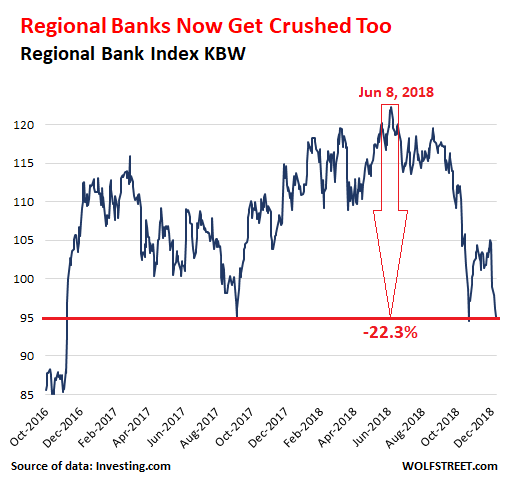

But those are the biggest 24 banks in the US. What bout the regional banks?

Since the big-bank sell-off started in January, the regionalbanks actually performed quite well, and the KBW US Regional Bank Index climbedto new post-Financial Crisis highs the summer.

The story on Wall Street was that regional banks would be immune to the downdraft, and that investors needed to rotate from big banks into regional banks, etc. With immaculate timing, the KBW Regional Bank Index [KRX] peaked on June 8, wavered for a month, and in September started to spiral down. It too has plunged 22.3% by now, but in a much shorter time period than the large bank index:

This is a new era for banks – the era the Fed arm-twisted them into preparing for: Building their loss-absorption capacity by building their capital buffer to have it nice and fat and ready to be eaten up by business loan losses over the next few years. But these are still the good times, loan losses are still low, and money is still flowing relatively cheaply and plentifully. The actual pain won’t start for a while.

Instead of “bubble” or “collapse,” the Fed uses “valuation pressures” and “broad adjustment in prices.” Business debt, not consumer debt, is the bogeyman this time. Read... The Fed Explains the Rate Hikes: To Prevent Financial Crisis 2