Economic cracks big enough to drive a car industry into are opening up all over the globe. Trade gaps are opening up between major allies. Widening spreads between the dollar and other currencies are shredding emerging markets. As we start into summer, these cracks and several others described below have become big enough to get everyone’s attention, just as I said last year would become the situation.

I had, as readers here know, predicted the same for last summer but revised my timing to this summer after Trump was elected and the hope for tax cuts lit on fire one of the world’s greatest stock rallies. Those tax cuts are also creating another rapidly rising gap between government revenue and government spending.

That rally died, pretty much as I said it would, almost as soon as those tax cuts became law. In fact, it died sooner than I said it would because I thought the tax cuts would provide more economic levity than they have. The Dow and S&P 500, as of last Monday’s close, hit their longest correction period since 1984! That’s more than half of my lifetime since we saw a correction period last this long.

However, now that the trade war is officially engaged, FANGMAN stocks (Facebook, Apple, Netflix, Google, Microsoft, Amazon and NVIDIA) are taking the market up again. Whether they will undo my prediction that the second leg down in the stock market will occur in early summer … remains to be seen.

Even so, this past Monday, when nearly every expert fully expected Netflix would blaze the trail upward as markets refocused on “earnings”, Netflix shares got slammed (down 13% in one mammoth stomp) because it had almost 20% fewer new subscribers than it had projected in April. Other Netflix news, such as revenue, was pretty much as expected or even a little better, meaning the reaction was … well … a bit panicky perhaps? It is what happens when everyone is leaning on the same seven stocks to save them and the world and the first one to report has wobbly legs.

Netflix blamed the shortfall on its emerging markets where a strengthening dollar crippled its projected growth. Ah, well, that’s still one of those cracks, and that means all is not even well in the FANGMAN stocks. Turns out emerging markets do have contagion that can hammer the United States leading stocks.

(And, as for stocks growing because of “earnings growth,” keep in mind that 50% of that earnings growth was due entirely to fewer tax dollars being taken out of the top-line number, not to corporate revenue growth.)

Trump’s election interrupted the establishment’s failing economic journey; but, as I said back then, the reprieve would be temporary. The collapse would resume. The Trump Rally was due, as David Stockman said, to people getting high on hopium. In reality, the Fed’s fake recovery was already on a path to failure, which it would take back up as soon as delirious hope gave way to the reality that failure was already baked into the “recovery” and that tax cuts of the kind Trump was providing would do little more than stimulate the world’s greatest wave of stock buybacks so that the insider money could get out of stocks, which it has been doing.

(As an interesting side note, Team Trump “forgot” to wipe out a provision in the tax code that allows individuals to pay the corporate tax rate, instead of the personal rate if they want to. That provision was made when corporate rates were higher during the Kennedy administration so that people rarely had reason to opt for the corporate rate. Because congress forgot to remove that provision, the wealthiest individuals in America can now pay less than the middle class at 21%. Ah, but what can you expect?)

Fed pops copper’s topper

I’ve written a lot this year about the Fed’s quantitative tightening as being the ultimate guarantee that the economic is going to sink, so I won’t write more on that here. I will, however, note the coincidence now with Dr. Copper verifying my diagnosis.

As the global economy goes, so goes the price of copper. Thus, copper is called “Doctor Copper” because it is often watched as a life sign for how the global economy is doing. Copper has finally started falling, after a period of healthy growth during the Trump Rally. Here is a graph of what copper prices have done in direct correlation with the Fed’s quantitative tightening: (It is not that the Fed’s actions directly change copper prices, but that, if they hurt the global economy, any downturn there will be reflected in a short time in what happens with the price of copper as demand for copper falls.)

The price of copper flattened when the Fed began QT and then churned sideways at that level all year. Not long after the Fed’s last increase in its rate of QT, copper finally began to fall. If copper is still accurate as an economic gauge, it means global growth, which was rising “harmoniously” last year, stalled with the Fed’s start of QT and, since the start of summer, it has been falling precipitously.

Imminent inversion of the prophetic yield curve

The moves of greatest interest are all happening in interest. Another sign of how well the Fed’s program is working — one that nearly every analyst is concerned about — is the spread between interest rates on short-term bonds and long-term bonds. It has been getting precariously close to its inversion point, an event that has preceded almost every recession known to modern man. Inversion happens when investors become willing to receive a smaller yield from long-term bonds than from short-term bonds, meaning they think something will go seriously wrong in the short-term.

Normally investors in long-term bonds demand higher interest because they anticipate more erosive inflation during a strong economy. When they perceive recession is imminent, on the other hand, they park their money longterm and anticipate less inflation due to recessionary (typically deflationary) forces.

If nothing else, inversion of the yield curve, since it is closely monitored as a key indicator by most investors, can be a self-fulfilling prophecy wherein markets fall because investors suddenly expect them to fall and act accordingly.

At less than one quarter of one percent difference between the long end of bond interest (10-year Treasury note) and the short end (2-year note), the yield curve is now the lowest it has been since the start of the Great Recession (2007).

Rising bond yields and the end of repatriation of foreign profits at lowered tax levels at the end of this year will curtail the stock buybacks that hit record levels this year, which have been the primary thrust behind the stock market throughout the Fed’s so-called “recovery.” Rising bond yields also compete for interest in stocks.

One other sign of impending recession — the spread between the interest rates of risky corporate bonds versus safe treasury bonds — has increased to the critical level (as a gauge) that it hit just before or during six of the last seven recessions.

The China Syndrome … again

Many financial experts are still arguing blindly that we are not yet in a trade war, and the stock market seems to be flitting back and forth on the idea. Yet, China has already promised retaliation against the tariffs Trump has already imposed, and Trump has already promised counter-retaliation to China’s retaliation (if it happens) in the form of another $200 billion worth of Chinese goods that will receive tariffs of 10%. And this week Trump upped his bet more and threatened the possibility of tariffs on all Chinese goods — about $500 billion worth.

You can say, “All the market evidence is turning out bad for China, so Trump will win,” but we already know that what is bad for trade in China is bad for the world. We’ve seen that play out before in 2015.

Confirmation that China’s economy is slowing amid an escalating trade war is a worrying omen for global growth. Data released since Friday has affirmed what’s been expected for some time: That an ongoing campaign to curtail credit is putting the brakes on the world’s second-largest economy. Given that China generates as much as a third of global growth, that means headwinds not just for China’s economy, but for the world’s too. (Newsmax)

The broader US stock market seems to be just counting down the days of advance into this trade war in sidewinding fashion until all of this actually happens. Investors appear to be hoping it is mostly negotiating rhetoric, but David Stockman (President Reagan’s Director of Office of Management and Budget) says Trump doesn’t have a clue about what he’s doing because Chinese tariffs in recent years are nothing (about 3.5% on average agains 1.7% average by the US):

[Stockman] was famously “taken to the woodshed” by President Reagan for his statements in a 1981 Atlantic Monthly article, that “supply-side economics — the backbone of the Reagan economic revolution – was a ‘Trojan horse’ that would ultimately benefit the rich….” [Now he says,] “The fact is, we are heading into a massive trade war in the world…. Trump doesn’t know what he’s doing at all. He is making it up. He is a hopeless protectionist with a 17th-century view of the world…. We have an absurd policy — dangerous, stupid. The worst that I’ve seen since my whole career started in 1970 under [President Richard] Nixon, and he did some crazy things.” (Global Macro Monitor)

China’s stock market has already fallen badly, and Chinese credit markets are tightening up rapidly. Chinese GDP growth is the weakest since 2009. If you have any doubt as to how the crashing Chinese economy can break destructively against US shores, remember the Chinese-induced summer flash crash of 2015 when S&P futures plunged 12% in one week.

It’s the spillover effect that most worries economists, given China’s central role in a regional and global supply chain that feeds America’s economy with goods and services. “We have not seen the worst yet,” said Iris Pang, Greater China economist at ING Bank NV in Hong Kong. “For the rest of the world it begins with a bilateral trade war between the U.S. and China but it would not end with a bilateral impact. Global supply chains, shipping companies, foreign investment hurdles from the U.S. government … will change global business flows.” (Newsmax)

If nothing else, because tariffs get built into the cost of goods sold, tariffs will assure inflation for US consumers, and inflation will pressure the Fed to maintain its quantitative-tightening schedule, even if the economy starts to go down so fast that the Fed’s infamously blind eyes can see it is failing. If inflation rises, the Fed will be caught in a corner, forced to continue tightening into a receding economy. (For the Fed, that is their nightmare stagflation scenario in which we will all be facing rapid inflation and tightening liquidity at the same time.)

Trump tax cuts and ultra-high government spending fail to deliver

While the insanely rich are directly pocketing all corporate tax savings via stock buybacks (as they were designed to), consider how poorly the stock market is doing anyway. All the negative economic facts listed in this article are happening during the largest tax cuts in history. Ineffective!

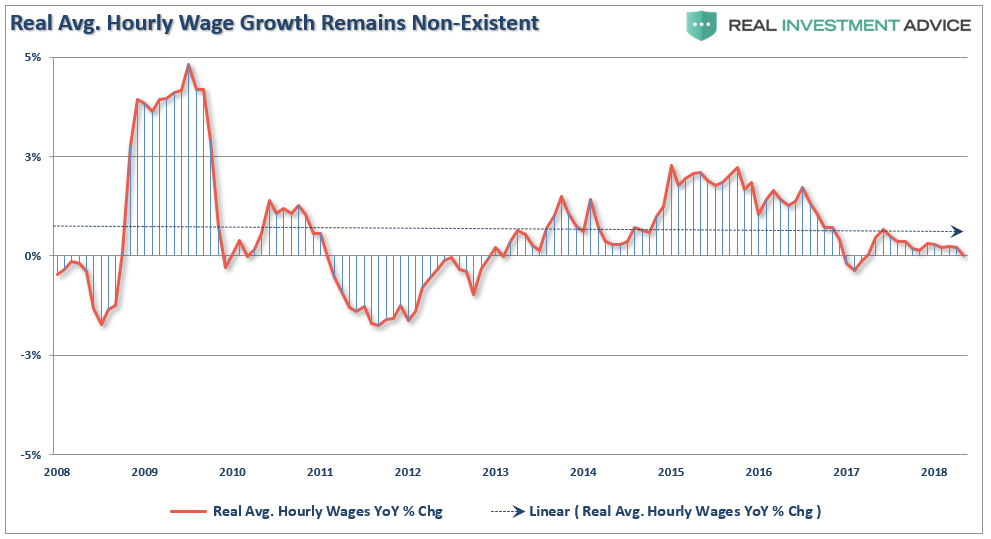

Wages haven’t even changed enough this year to keep up with rapidly rising inflation. That means wealth creation, even after the Trump Tax Cuts, is still failing to trickle down in order to improve consumer spending capabilities:

The Organisation for Economic Co-operation and Development (OECD) warns that positive employment trends are at risk of being derailed by “unprecedented wage stagnation” affecting low-paid workers. This is as much true in the US as other parts of the world: (Compare wage growth in 2007 to ten years later.)

In spite of tax cuts, wage growth in the US falls short of the growth rate in 2007 by more than half. And consider …

Explosion of personal debt will lead to personal explosions

One thing that has gone up, even though the stock market is mostly churning sideways and wages are losing to inflation is personal debt. People here in the 99% where I live make up for the lack of wage growth by taking out more debt to try to maintain a standard of living that our constantly lagging wages will cover. (The operative word being maintain, not improve.)

Financial inequality (meaning here inequality of wealth-creating opportunities between the 1% and all the rest) eventually leads to a peasant revolt. (I’m not saying we should all have equal wealth, but we are suffering from lack of equal opportunity to create wealth, and the new opportunities are all being hand-delivered to the already wealth.) The peasantry doesn’t want to revolt by nature, so it takes a lot of oppression to overcome their inertia; but unrestrained greed at the top is getting us there as the stakeholders maintain the tightest stranglehold on wages that they can while many of the 99% indenture themselves with debt owed to the banksters just to maintain their lifestyle position. Personal indebtedness has climbed from a reasonable move downward during the Great Recession back to an all-time high.

The greed gap between the 1% and all the rest grew exponentially wider under Trump

Greed has reached its highest level in modern history. Consider that dividends for corporate owners have rarely if ever been higher or more abounding, stock buybacks have certainly never been higher, which have also filled the pockets of corporate owners, and dividends have never been higher, while taxes on corporate earnings are at or near historic lows as are personal taxes on the wealthy.

All of that means corporate owners have never been richer! Yet, none of those benefits have trickled down to those who make their money by working in those companies. I warned about all of this before the Trump Tax Cuts became law, and now the data are in:

Not surprisingly, our guess that corporations would utilize the benefits of ‘tax cuts’ to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. [Article was written back in February.] This is ‘financial engineering gone mad’ and something RIA analyst, Jesse Colombo, noted recently:

‘… corporations have largely focused on juicing their stock prices via share buybacks, dividends, and mergers & acquisitions. While this pleases shareholders and boosts executive compensation, this short-term approach is detrimental to the long-term success of American corporations…. Even more alarming is the fact that share buybacks are expected to exceed $1 trillion this year, which would blow all prior records out of the water. The passing of President Donald Trump’s tax reform plan was the primary catalyst that encouraged corporations to dramatically ramp up their share buyback plans. (“The Data Is In: Tax Cuts And The Failure To Trickle Down“)

While I suspect the $1 trillion estimate for 2018 buybacks is exaggerated, there is no question at all that buybacks have lifted to unprecedented heights. (If it is not an exaggerated estimate, then there is zero chance of the stock market crashing this year because buybacks all by themselves will drive it higher no matter what the economy does. My prediction will lose solely due to the fact that corporate greed went even beyond the upper ravages of greed that I anticipated.) We’ve never seen anything remotely like this.

Now consider that, even as corporate owners and overseers are personally pocketing all of this Titanic tax benefit, corporations are complaining that they cannot get well qualified help … even as they refuse to lift wages in order to get that help! Corporate owners have become so intensely greedy that they will not loosen the grip of their tiny, green-stained hands the least bit to let the thinnest thread of a dollar bill escape their grasp in order to get the qualified help they CLAIM their companies need in order to grow.

They are now milking every cent out of their companies with almost no investment for longterm growth or improved labor situations, even in a labor market that they claim is one of the tightest ever. The tiny trickle of wealth that once slipped through their hands has been firmly squeezed off. Now THAT is greed! This generation of principle shareholders will go down as the greediest in American history.

Corporate tax cuts not paying for themselves, resulting in massive US deficit

According to the latest monthly Treasury statement, the amount collected for individual income taxes throughout the first nine months of the fiscal year hit a record of $1.3 trillion, but the amount for corporate income taxes — even with record repatriation of accumulated foreign profits — was way down ($68 billion lower than the first eight months of the last fiscal year). Combining those tow facts, the government has in the past nine months collected less than it has during the same period for any of the previous five fiscal years! That tax deficiency along with Trump’s profligate increase in government spending along with the balance of other tax differentials, has left the federal government with a gaping $607 billion break in the budget for the first nine months of the year.

As the trend stands now, June ran an overall $75 billion budgetary gap compared to May’s $147 billion deficit. That was, nevertheless, still the second-largest June deficit since the pit of the Great Recession. (June tax collection under the new Trump Tax Cuts was down 6.6% year on year.) Total government debt passed $21 trillion in June. At the start of the Trump administration, it had just passed the eye-popping $20 trillion milestone. (Tax amounts are in constant June 2018 dollars.)

Big gaps are opening up everywhere.

US debt problem compounded by rising interest

That problem is compounded with interest. With interest rates rising (the 2-year treasury note is now the highest it has been since the start of the Great Recession), total interest paid on the US debt has never been higher:

At over $550,000,000,000 a year, half of our massive annual deficit is due to interest on all the previous deficits. I’ve been warning on my blog that we can expect a blow-out in the federal debt to become evident this year under the Trump Tax Cuts and all of the increased military and stimulus spending because the ballooning of debt is now finally concurrent with a rapid rise in interest rates. High deficits under Obama were partially papered over with practically non-existent interest. You can see the blowout that has just happened on total interest payments in the graph above.

The US government is starting, at last (as I’ve said it would), to find it more difficult to sell debt. Last month, it saw one of its worst treasury auctions in years. The debt financing struggle right now surges and then relaxes, but the surges of energy required to sell the debt are increasing.

US debt problem compounded by fleeing financiers

Another gulf is growing between the US and its fleeing financiers. For about three years I’ve been saying that Russia would divest completely from US treasuries in order to end the hegemony of the US dollar. This is the year in which they have done that. They started back in April and have already divested four-fifths of all their US treasury holdings. Who can blame them, given all the sanctions the US has placed on them? Why would they want to have their sovereign treasure tied up in wealth the US can freeze or seize? And with trade down, what do they need those dollars for?

A U.S. Treasury report this week appears to show Russia liquidating dollar assets at a record pace, selling four-fifths of its cache of U.S. government debt, $81 billion worth, over a two-month period. It started in April, when the U.S. imposed the most onerous sanctions yet on allies of Putin. The release caused a stir in the markets because neither the Treasury nor the Bank of Russia will comment on the transactions…. For Sergey Dubinin, Russia’s central bank chief from 1995 to 1998, there’s no mystery at all — the sales were simply a prudent “hedge” against confiscation, a possibility that looks more likely every day. Russia, he said, has learned from Iran’s experience and is converting its dollar assets into other currencies to safeguard its reserves against any attempts at seizure…. Putin has long railed against “the dollar monopoly,” even referring to the U.S. as a “parasite” for “living beyond its means.” In May, after he was sworn in for a fourth term, Putin went further and called for a “break” from the dollar to bolster the country’s “economic sovereignty.” (Newsmax)

Russia was once the United States’ second-largest financier. With Russia divesting from US dollars almost entirely now and China setting up the yuan to compete as a global trade currency and with Iran now selling all of its oil outside the petrodollar market due to US sanctions, the move against the US dollar as a global trade currency is strengthening rapidly. These nations once bought a lot of US treasuries because they did a lot of trade in US dollars. Because it is often easier to exchange US bonds as a way of exchanging dollars between countries than to exchange actual currency, nations have less and less reason to buy US bonds as tariffs slow trade and the yuan starts to compete for trade status even in the petroleum market.

As the dollar becomes increasingly unpopular, the US will have a harder time finding financiers so it won’t benefit as easily from the low-interest comfort zone in which it has thrived. This could ramp up fairly quickly with the trade war leading to currency wars. With trade diminishing due to tariffs and more nations upset with the US, it is quite possible the US dollar will find fewer buyers. Dollar days are numbered.

Rising interest on all debt already creating crises for emerging markets

With total global debt (households, businesses and governments) now at $247 trillion, rising interest rates are a serious problem for everyone (maybe even their bankers if defaults continue to accelerate). The time bomb we have created has even more risk of blowing up soon if Trump’s trade wars decrease global GDP, making it harder for businesses and governments to service their debts. While the US will continue to service its debts for the time being, marginal nations may default, and that can cascade through the banking system throughout the global economy.

We are seeing this already in emerging markets (EMs) where the rising value of the dollar compared to local currencies is creating serious financial stress fractures for nation’s and businesses whose debt obligations are denominated in US dollars. Even the US in not immune to the spread of those cracks coming all the way back to many US investors and some US banks (just as we saw this past week with Netflix).

In a new report, the Institute of International Finance, an industry research and advocacy group, says that the debts of some “emerging market” countries (Turkey, South Africa, Brazil, Argentina) seem vulnerable to roll-over risk: the inability to replace expiring loans. In 2018 and 2019, about $1 trillion of dollar-denominated emerging-market debt is maturing, says the IIF…. “″(We had) a goldilocks economy, with decent economic growth. Inflation was nowhere to be seen, allowing central banks (the Federal Reserve, the European Central Bank) to be more accommodative (i.e., keeping interest rates low). You could always roll over your debt. However, the probability of this continuing is much less now.” (The Columbus Dispatch)

These experiences give other nations reason to hate the dollar and to avoid it in the future IF they can so as not to become trapped by moves the US makes in its own self-interest.

Inflation lift off at last

Just in the nick of time, then, to augment the growing EM problem, US inflation (CPI) is rising per the Fed’s long effort to make it do so. Inflation hit 2.9% last week (year on year), its highest in six years. When you consider that the CPI measure of inflation intentionally factors out some of the worst inflation (the volatile stuff that consumers actually have to pay), that official inflation number is scorchingly hot! If measured as it was back in the high-inflation Nixon and Carter years, it would be something near 10%! That is a major crack opening up in the future buying power of the money you have saved now.

It also means the Fed won’t be able to back out of its quantitative tightening even if it wants to because it has inflation that it already created finally pushing it to tighten faster. It is becoming caught in an inflation trap. Wholesale inflation (PPI) also jumped to a six-year high this week. The Producer Price Index is on more of a tear than CPI, hitting 3.4%. (Core wholesale inflation, which strips out energy and food, was 2.9%.)

That means that consumer inflation is going to continue to increase as inflation happening among producers gets passed along. Some of that PPI increase is bound to press forward into retail pricing for more CPI inflation down the road. How much PPI inflation affects consumer price inflation depends on how much producers can absorb in order to hold inelastic retail prices down.

Remember, if inflation rises, bond interest rises. If bond interest rises, bond prices fall. If bond prices fall, the bond bubble breaks, and down falls baby, bonds and all. That means the Fed, backed into a corner, will be pressed to fight inflation with more quantitative tightening over propping up stocks with a return to quantitive easing or even just by backing off of QT because bond bombs hit closer to banks.

As things stand now, the Fed has no intention of backing away from QT for a long time. Fed Chairman Powell said on Tuesday,

“With appropriate monetary policy, the job market will remain strong and inflation will stay near 2 percent over the next several years,” Powell said in one of the strongest affirmations yet that the Fed is within reach of its dual policy targets more than a decade after the United States endured a deep financial crisis and recession. The Fed “believes that – for now – the best way forward is to keep gradually raising the federal funds rate….” Overall the risks to the economy were “roughly balanced,” with the “most likely path for the economy” one of continued job gains, moderate inflation, and steady growth. (Newsmax)

The stock market, oblivious as always, seemed to love all the QT-assuring news about rising CPI, as was demonstrated when the Nasdaq hit an all-time record on the same day the inflation reports came out.

The problems above are real now, but we also have the following ongoing problems in development:

- National shutting down of retail stores and their domino effect.

- Bank failures looking imminent in Germany and Italy.

- A renewed Grexit/Italeave problem.

Contrary forces to my own predictions

On the other hand, the Retail Apocalypse and Carmageddon, which had been going exactly as I had laid out, took a slight curve against me in the past week’s reports. Retail sales surged 0.5% in June (pretty good bump for one month), and the biggest factor in the surge was car sales! May sales were also revised upward to a 1.3% leap, which was the best performance since last September. Year-on-year, retail was up 6.6%. Reports did not clarify how much of that was online sales, versus brick and mortar, which is where the Retail Apocalypse is becoming a sea of troubles.

However, the other biggest parts of these two bumps were building materials (which I said would surge right now as rebuilding out of the rubble and ashes of extreme demolition wrought by three massive hurricanes and numerous wildfires last year takes time) and gasoline prices (an economic negative when prices get this high). So, the retail bump was not as positive as it seemed to many.

Consumer spending in the first quarter was its lowest in five years. The second quarter was up some; so, we may have gotten a bit of a Trump bump. However, sales in this case are measured in dollars (not units sold). With inflation rapidly making things more expensive in the second quarter, much of Q2’s boost was nothing more than the long-anticipated start-up of inflation, now well above the Fed’s target rate, which came about abruptly.

Moreover, while Carmageddon looked like it got a month of reprieve in the US, it turned much worse in China. It was the worst first half of a year ever for Ford where vehicle sales in China tumbled 38% in June. (Ford sales were down 25% year on year.) Ford’s situation, with some of its vehicles coming out of the US, could become worse with China now slapping tariffs on US vehicles. Ford has said it will absorb those tariffs, rather than raise prices. For almost twenty years, Ford has seen China as a prospect for major expansion. (GM sales in China, on the other hand, were up 4%.)

Is an economic collapse becoming obvious in the early summer as I promised?

Well, for the first time in four years Barclay’s Bank published its quarterly Global Macro Survey, which polls over 400+ institutional investors, and the majority of institutional investors around the world said they expect the global economy to surprise to the down side. Respondents said the most likely downside surprises would emanate from China, followed by the Eurozone, followed by Emerging Markets (all areas where the global economy is breaking up as noted above).

The trends above are pretty serious cracks, and I reported earlier this week about the first signs of the return of decline in housing, which I also I said would happen by the end of this summer. Whether all of that builds in time to prove the timing of my own predictions is right and to save my blog from my bet that global economic collapse (including for the US) and a US stock market crash will become clear by early summer (first half of the summer), it is certainly a strong and growing body of evidence that the Epocalypse is coming!

My detractors will be cracking up if I miss my mark, but that is a risk I’m willing to take in order to put out the strongest warning I can. Even more than wanting to warn people, I want to continually point out how wrong the path of recovery has been in hopes that some people in the right places will see that truth when the breakup happens. Otherwise, we will wind up repeating it all over again is some even more grotesque manner, including bailing out banksters all over again.

Most of all, I hope to end the insidious religiously held belief in trickle-down economics by pointing out how they never have trickled down and pointing out repeatedly in advance that the current trickle-down attempts will not trickle down either and why they will not trickle down. By saying it in advance, maybe people can realize this knowledge was not just a convenient claim after the fact. It was foreseeable.

I hope to do my part to end any excuse for continuing to blunder endlessly back down the path that says “the best way to make sure of justice for the poor and the middle class is to take care of the rich, for they are the wealth creators and the job creators.” That is obscene nonsense. Shame on any who continue to believe it after so many proofs that it does not work.

I am not for wealth redistribution, but neither do I believe for a second that the 1% have ever paid a greater share of their income in taxes than the middle class (due to their loopholes and the fact that they make most of their money speculating in stocks at lower capital-gains rates). Nor do I believe in giving the lion’s share of tax breaks in a manner that applies 99% of the benefits toward helping the wealthy 1% get richer. Anyone should have been able to see the breaks were DESIGNED to go to stock buybacks. That path will never create a wealth effect for any of the rest of us. It will help your retirement fund (if you don’t hold the money in stocks long enough to lose it again), but it does nothing to help you and your family until then.

When the social fabric is torn with the masses revolting against the next bankster bailouts, I want the greedy bastards to know they could have and should have seen that their own greed was leading us inexorably down this path! Greed contains the seeds of its own destruction, but it takes a fire to make those seeds germinate. And, unfortunately, we are on a path that could easily lead to a great conflagration all over the world because greed has been repeatedly honored with bailouts and tax breaks and the most rewarding positions in government to where I believe greed has grown worse than it has ever been in modern history.

So, I’d rather go down in flames by betting all my last five year’s writing on what I am saying now than just slip silently and chronically into an everlasting hell of whining about the economy … mostly unheard. If I do go down in flames, maybe what I’ve said will be a little more memorable when the collapse comes.

That said, the growing number of major economic cracks all over this planet indicate that the next leg down in the stock market could still happen in time to save me from my bet. These gaps in the global economy are finally no longer going unnoticed. People are starting to look around and wonder if things are going to fall apart. Even the largest financial institutions in the world have finally started revising their economic outlooks for the economy (US and global) downward.

The Epocalypse is coming! I haven’t climbed up on my housetop to shout it, but I am shouting it from here. (No one listens to people on my housetop anyway.) You may wind up cracking up at me as a heckler if I fail, but I’m OK with that because you also may just wind up cracked up because you didn’t listen. I’d rather risk the former, as I can happily live my life without this blog. It is the least sacrifice to make. I can think of many other fun ways to spend my time; and, if I’m wrong, I will.