Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

Is the euro dead yet? And how is the Chinese Renminbi doing?

Total global foreign exchange reserves, in all currencies, rose to $11.4 trillion in the fourth quarter 2018, according to the IMF’s just released COFER data. These foreign exchange reserves do not

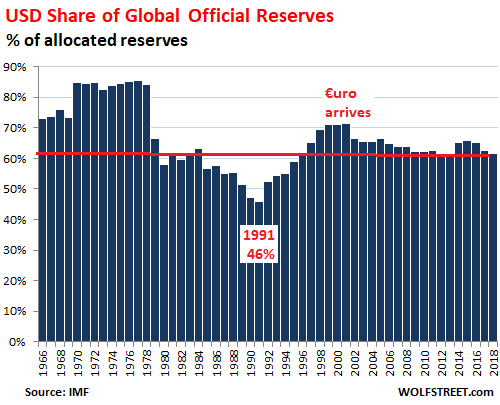

In 1999, the euro became an accounting currency in the financial markets, replacing the European Currency Unit. On January 1, 2002, Euro banknotes were released into circulation and gradually replaced the national banknotes of the original member states of the Eurozone. Note the drop of the dollar’s share, from 71.5% in 2001 to 66.5% in 2002. Today, the euro has replaced 19 national currencies. And the dollar’s share is down to 61.7%:

In Q4, the euro’s share of foreign exchange reserves rose to 20.7%, the highest since Q4 2014. The creation of the euro – the idea of eventually consolidating all European currencies in one big currency – was an effort to knock the dollar off its hegemonic pedestal. The goal was for the euro to eventually reach “parity” with the dollar. Then the euro debt crisis happened.

The degree of dominance of the US dollar as global reserve currency is determined by the amounts of US-dollar-denominated financial assets – US Treasury securities, corporate bonds, etc. – that central banks other than the Fed are holding in their foreign exchange reserves. The dollar’s role as a global reserve currency diminishes when central banks shed their dollar holdings and take on assets denominated in other currencies.

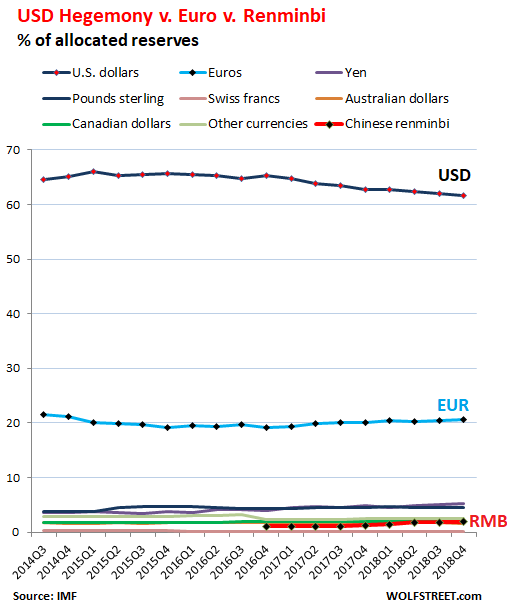

The combined share of the dollar and the euro edged down to 82.4% in Q4 2018. The remaining currencies make up 17.6% of allocated global reserve currencies. On October 1, 2016, the IMF added the Chinese renminbi to its currency basket, the Special Drawing Rights (SDR), elevating it to an official global reserve currency. Hopes by some folks that it would dethrone the dollar as hegemon have been disappointed. But little by little, the renminbi is gaining. In Q4 2018, with a share of 1.89%, it beat the Canadian dollar for the first time and moved up to fifth place on the list:

- Dollar: 61.7%

- Euro: 20.7%

- Japanese yen: 5.2%

- UK pound sterling, at 4.4%.

- Chinese renminbi: 1.9% (record)

- Canadian Dollar: 1.8%

- Australian dollar: 1.6%

- Swiss franc: 0.15%

- Other: 2.48%

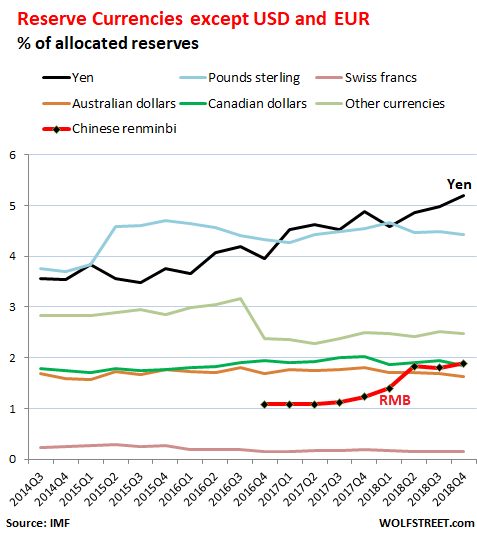

This chart shows the battle among the lesser reserve currencies (without the dollar and the euro). Note the surge of the yen’s share from 3.6% in 2014 to 5.2% at the end of 2018. The renminbi is the red line that starts in 2016. The share of “other currencies” dropped that year as the renminbi became an entry. The IMF doesn’t disclose details, but we can assume that the renminbi had been listed under “other currencies” until 2016, when it was separated out.

But with the USD and the EUR added to the chart, the other currencies are reduced to their place at the bottom, with the Chinese renminbi (bright red line at the bottom) still near irrelevance:

As the IMF points out, this data is based on the currencies’ share of “allocated” reserves. Not all central banks disclose to the IMF how their total foreign exchange reserves are “allocated” among specific currencies. But disclosure has increased and the data is becoming more complete. In Q4 2014, “allocated” reserves accounted for only 59% of total reserves; now they account for 94%.

And a special word about the theory that the US, as the country with “the” global reserve currency, “must have” a large trade deficit with the rest of the world. This “must have” is clearly not the case because the Eurozone – with the second largest reserve currency – has a large trade surplus

But there is another way of looking at this: The fact that the dollar is the largest reserve currency and largest international funding currency allows the US to easily fund those massive trade deficits, which has made the trade deficits possible over the past two decades. This may not always be the case in the future, but so far so good, as they say.

The US trade deficit goes out-of-whack as Corporate America searches for cheap labor and tax benefits. Read... Good Lordy, What a Banner Year 2018 was for China, Other Countries, and Corporate America