As the US Treasury 10-year yield approaches 2% … again, we begin to worry about issues such as extension risk and convexity risk (collectively known as “The Wings”) given their propensity to drive hedging.

Extension Risk

Historically, the risk of sudden yield curve movements has greatly affected the market for MBS, which represent claims on a pool of underlying residential mortgages. The interest rate risk of MBS differs from the interest rate risk of Treasury securities because of the embedded prepayment option in conventional residential mortgages that allows homeowners to refinance their mortgages when it is economical to do so: When interest rates fall, homeowners tend to refinance their existing loans into new lower-rate mortgages, thereby increasing prepayments and depriving MBS investors of the higher coupon income. However, when rates rise, refinancing activity tends to decline and prepayments fall, thereby extending the period of time MBS investors receive below-market rate returns on their investment. This is commonly known as “extension risk” in MBS markets.

Duration and Convexity

The effect of the prepayment option can be seen in the chart below, which displays the relationship between yield changes (x-axis) and changes in the value of an MBS (black) and a non-prepayable ten-year Treasury note (red). The sensitivity of each instrument to small changes in yields (essentially the slope of each yield-price relationship at the point at which the MBS was last hedged, indicated by the dashed line) is known as the effective duration, while the rate at which duration changes as yields change (the curvature of the price-yield relationship) is known as its convexity. In the example shown below, the MBS and Treasury security are duration matched in the sense that they will tend to move one-to-one for small changes in yields.

When interest rates increase, the price of an MBS tends to fall at an increasing rate and much faster than a comparable Treasury security due to duration extension, a feature known as the negative convexity of MBS.Managing the interest rate risk exposure of MBS relative to Treasury securities requires dynamic hedging to maintain a desired exposure of the position to movements in yields, as the duration of the MBS changes with changes in the yield curve. This practice is known as duration hedging. The amount and required frequency of hedging depends on the degree of convexity of the MBS, the volatility of rates, and investors’ objectives and risk tolerances.

Duration hedging of MBS can be done with interest rate swaps or Treasury bonds and notes. When rates decline, hedgers will seek to increase the duration of their positions. This can be achieved by buying Treasury notes or bonds, or by receiving fixed payments in an interest rate swap. Conversely, MBS holders will find the duration of their MBS extending when rates increase, which they may choose to offset by selling Treasury notes or bonds, or by paying fixed in swaps. If sufficiently strong, this hedging activity can itself cause interest rates to rise further, and further increase duration for MBS holders, inducing another round of selling of Treasuries.

A Convexity Event Averted

A sudden initial rise in medium- to long-term rates can therefore trigger a self-reinforcing sell-off in Treasury yields and related fixed income markets, fueled by MBS hedging—a phenomenon known as a convexity event. During a convexity event, MBS hedgers collectively attempt to decrease duration risk by selling Treasury securities or paying fixed in swaps. The two most important factors that determine the likelihood of a convexity event are the size of the MBS portfolio held by duration hedgers and the convexity of that portfolio. The large-scale purchases of MBS initiated by the Federal Reserve in November 2008 as part of the post-crisis LSAPs have had a profound impact on both these determinants.

MBS investors, broadly speaking, fall into two categories: those holding MBS on an unhedged or infrequently hedged basis and those that actively hedge the interest rate risk exposure. Unhedged or infrequently hedged investors include the Federal Reserve, foreign sovereign wealth funds, banks, and mutual funds benchmarked against an MBS index. MBS holders who actively hedge include real estate investment trusts (REITs), mortgage servicers, and the government-sponsored enterprises (GSEs).

Mortgage bonds are often held by large investors such as money managers and banks. They tend to prefer stable returns and constant duration as a means to reduce risk in their portfolios. So when interest rates drop, and mortgage bond duration starts to shorten, the investors will scramble to compensate by adding duration to their holdings, in a phenomenon known as convexity hedging. A hedge is basically investing in something that tends to go up when the first thing goes down (or vice versa). To add duration, so as to extend payments into a longer period, investors could buy U.S. Treasuries, which would further push down yields in the market. Or they could use interest-rate swaps, which are a contract between two parties to exchange one stream of interest payments for another.

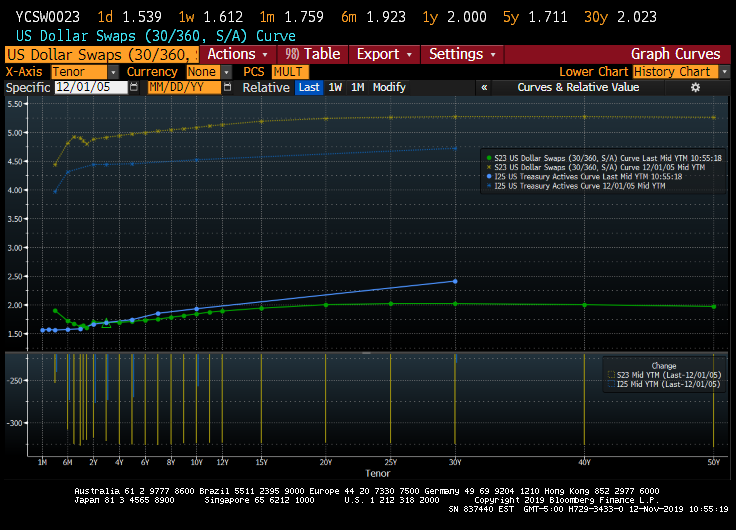

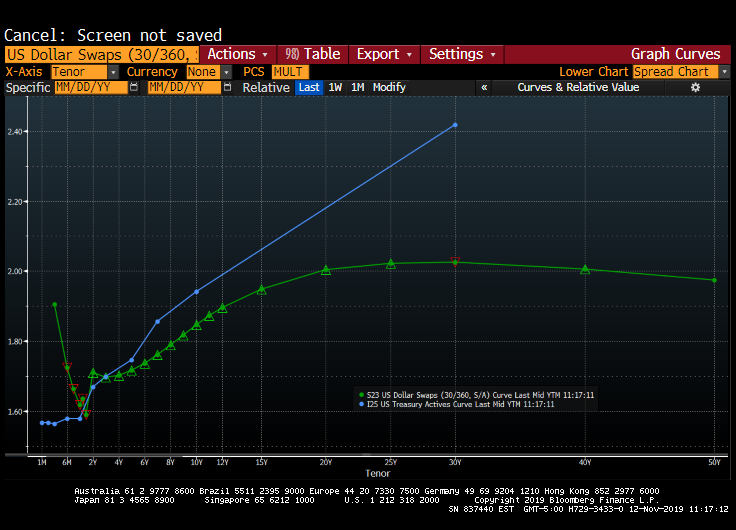

Here are the dollar swaps and US Treasury actives curves today and from December 2005 to illustrate the decline in both curves of around 300 basis points at the ten year tenor.

Today’s US Treasury curve upward sloping … again having retreated from the inverted curve.

Here is a snap shot of MBS hedge ratios by coupon.

Of course, interest rates are influenced by the Voodoo Children themselves, the Central Banks like The Federal Reserve.