Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

Oops, they’re already rising.

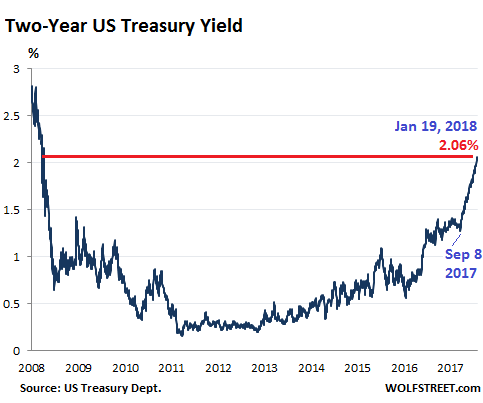

The US government bond market has further soured this week, with Treasuries selling off across the spectrum. When bond prices fall, yields rise. For example, the two-year Treasury yield rose to 2.06% on Friday, the highest since September 2008.

In the chart, note the determined spike of 79 basis points since September 8, 2017. That was the month when the Fed announced the highly telegraphed details of its QE Unwind.

September as month of the QE-Unwind announcement keeps cropping up. All kinds of things began to happen, at first quietly, without drawing much attention. But then the trajectory just kept going.

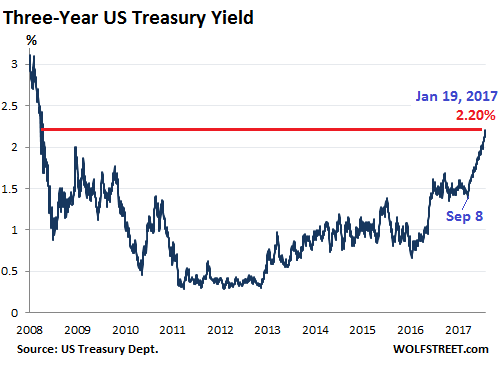

The three-year yield, which had gone nowhere for the first eight months of 2017, rose to 2.20% on Friday, the highest since October 1, 2008. It has spiked 82 basis points since September 8:

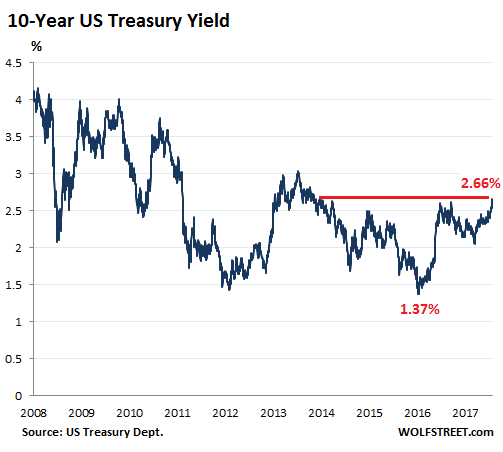

The ten-year yield – the benchmark for financial markets that most influences US mortgage rates – jumped to 2.66% late Friday.

This is particularly interesting because the 10-year yield had declined from March 2017 into August despite the Fed’s three rate hikes last year, and rising short-term yields.

At 2.66%, the 10-year yield has reached its highest level since April 2014, when the “Taper Tantrum” was winding down. That Taper Tantrum was the bond market’s way of saying “we’re shocked and appalled,” when Chairman Bernanke dropped hints the Fed might eventually begin tapering what the market had called “QE Infinity.”

The 10-year yield has now doubled since the historic intraday low on July 7, 2016 of 1.32% (it closed that day at 1.37%, a historic closing low):

Friday capped four weeks of pain in the Treasury market. But it has not impacted yet the corporate bond market, and the spread in yields between Treasuries and corporate bonds, and particularly junk bonds, has further narrowed. And it has not yet impacted the stock market, and there has been no adjustment in the market’s risk pricing yet.

But it has impacted the mortgage market. On Friday, the average 30-year fixed-rate mortgage with conforming loan balances ($417,000 or less) for top-tier borrowers, according to Mortgage News Daily, ended at 4.23%, the highest in nine months.

But historically, 4.25% is still very low. And likely just the beginning of a long, uneven climb higher.

And the impact on mortgage payments can be sizable. When rates rise for example from 3.5% to 4.5%, the payment for a $250,000 mortgage jumps by $144 to $1,267 a month. This can move the payment out of reach for households that have trouble making ends meet.

A one-percentage-point increase takes on larger proportions in a place like San Francisco, where it might take a mortgage of $1.25 million to buy a median home. At 3.5%, the monthly payment is $5,613. At 4.5%, it jumps to 6,334, an increase of $721 a month and an increase of $8,652 a year.

A mortgage rate of 4.5% is still very low! And it is likely headed higher.

Since the Financial Crisis, the ultra-low mortgage rates were among the factors that have caused home prices to soar. But as rates are heading higher, the housing market is in for a big rethink. These higher rates are going to be applied to the now prevailing sky-high home prices.

This will come in addition to the rethink triggered by what the new tax law will do to the housing market.

There’s another aspect to this equation: Homebuyers who are willing and able to stretch to cough up those higher mortgage payments can’t spend this money on other things. Falling mortgage rates gave a huge boost to home prices and to the entire economy in numerous ways. But that process will go into reverse.

So where will it go from here? The 10-year yield is still historically low and has a lot of catching up to do with regards to the trajectory of shorter-term yields. In addition, the Fed will continue to push its buttons – gradually hiking its target range for the federal funds rate and proceeding with its “balance sheet normalization.” And as the 10-year yield rises, mortgage rates will respond, and Housing Bubble 2 will get a lot more costly to deal with.

Even the bond market’s inflation expectations now exceed the Fed’s target. Read… Bond Market Smells Inflation, Begins to React