Just recently, I was accused of “quietly abandoning” my belief that rates are ultimately headed toward zero. Nothing could be further from the case particularly as the recent rise in rates is accelerating my base case.

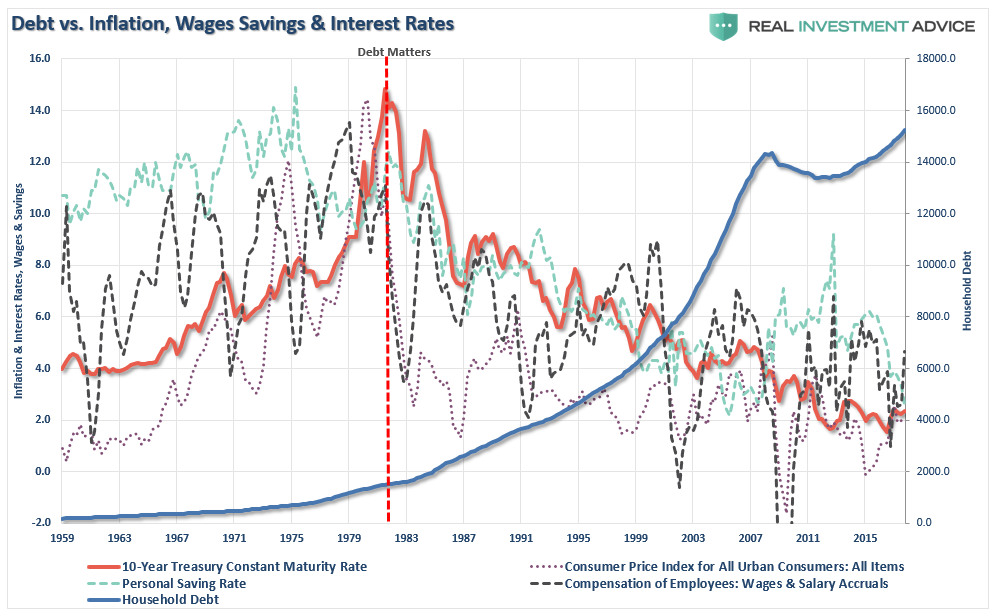

The chart below, which tracks rates back to the late-1800’s shows, that rates can, and do, remain low for extremely long periods of time.

Rates are ultimately directly impacted by the strength of economic growth and the demand for credit. While short-term dynamics may move rates, ultimately the fundamentals combined with the demand for safety and liquidity will be the ultimate arbiter.

What is clear is that the rise in rates in the 60-70’s was combined with rising inflationary pressures driven by rising wages and ultimately economic growth. It was also a time where very low indebtedness allowed rates to rise without a severely negative consequences.

With households, corporations, the government and investors more levered today than ever before in history, the rise in rates is the “fuse” that will eventually ignite the next major reversion. As I discussed yesterday, that epicenter of that reversion will be pension funds.

When the $4-5 Trillion in required bailouts for pension funds begin, not to mention potential bailouts of mortgages, auto loans, and student loan debt, the demand for Treasuries will surge sharply driving rates lower once again. The next rounds of Quantitative Easing will dwarf what we have witnessed over the last decade.

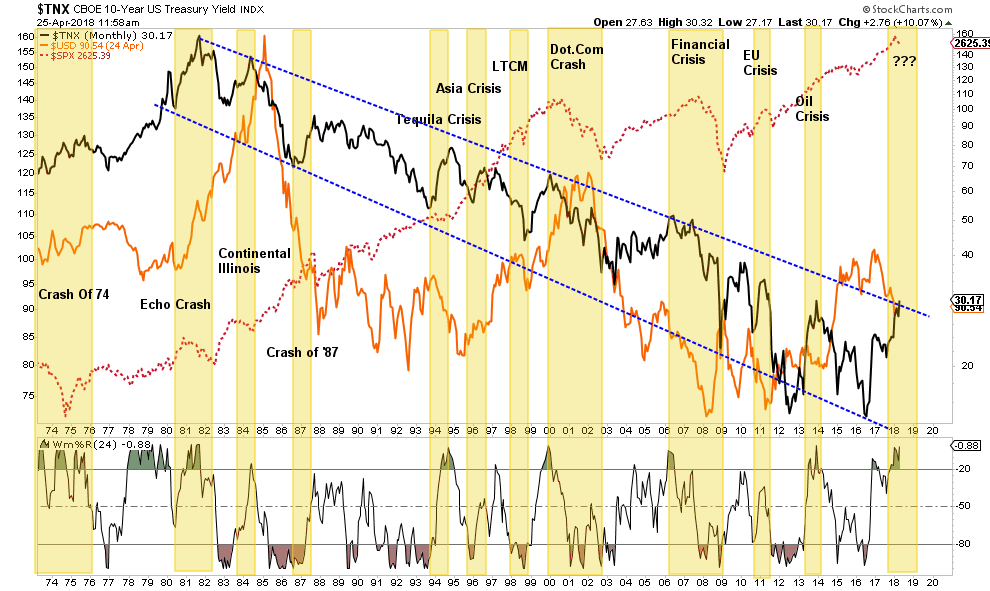

What is clear is that sharp increase in interest rates, particularly on a heavily levered economy, has repeatedly led to negative outcomes. With rates now at extensions only seen in 7-periods previously, there is little room left for rate acceleration before such an outcome spawns.

Given that such negative outcomes have always led to lower future rates, this time is unlikely to be any different. The only question is the timing, and as they say, “timing is everything.”

But don’t dismiss my recent quietness on rates as a change of attitude, actually we remain heavy buyers of bonds every time rates hit overbought levels.

However, while I am fairly certain the “facts” will play out as they have historically, rest assured that if the “facts” do indeed change, I will gladly change my view.

Currently, there is NO evidence that a change of facts has occurred.

Just something to think about as you catch up on your weekend reading list.

Economy & Fed

- Oil Prices Release Gusher Of Nonsense by Caroline Baum via MarketWatch

- Markets Must Prepare For Stagflation by Danielle DiMartino-Booth via Bloomberg

- Reform Entitlements by National Review

- CBO’s Budget Analysis Paints A Grim Picture by Committee For A Responsible Federal Budget

- Building More Highways Won’t Reduce Traffic by Scott Sumner via The Money Illusion

- Looking Past Slowing Global Growth by Edward Harrison via Credit Writedowns

- Ignoring Wealth Gap Isn’t Economically Sound by Patrick Iber via The New Republic

- Spending Never Gets Blamed For Deficit by J.T. Young via Washington Times

- Dems’ Get A New Plan – Socialism by IBD

- A 1990 Playboy Interview Explains Trumponomics by Jibran Khan via National Review

- Don’t Worry About Recession, Worry About The Fed by Matt O’Brien via Wonkblog

- Do Tax Payers Know They Are Handing Out Billions To Businesses? by Nathan Jensen via NYT

Markets

- ECB Launches A Stealth Taper by Tyler Durden via ZeroHedge

- The Most Important Chart Of The Century by Shawn Langlois & Jessica Shaw via MarketWatch

- Fed Is Behind, Still Screwing Up by Tom McClellan

- Trump’s Stock Market Looks Like Reagan’s by Keris Lahiff via CNBC

- Why Are Investors So Afraid Of Bonds? by Mark DeCambre via MarketWatch

- Have Investors Given Up On Bull Market by Luke Kawa via Bloomberg

- Yes, It’s A Bubble. So, What? by Rob Arnott via Research Affiliates

- Is Diversification A Free Lunch? by Gary Mishuris via Enterprising Investor

- Amazon Baffles Investors With BS by Shira Ovide via Bloomberg

- The Real Message Of The Yield Curve by Conor Sen via Bloomberg

- Reminiscing On Reminiscences Of A Stock Operator by Seth Levine via The Integrating Investor

- Where Did All The Dip Buyers Go by Brian Maher via The Daily Reckoning

- Key Trendlines Are Being Tested by Dana Lyons

Most Read On RIA

- Analyst Estimates Go Parabolic, Are Markets Next by Lance Roberts

- 5-Indicators To Watch by Lance Roberts

- Nowhere To Hide by Michael Lebowitz

- Investors Must Be Their Own Fiduciary by Richard Rosso

- Smart Money Is Bullish On The Dollar by Jesse Colombo

- Pension Crisis Is Worse Than You Think by Lance Roberts

- See A Bubble, Get Out Of The Way by John Coumarianos

- The Return Of The Bond Vigilantes by Doug Kass

Research / Interesting Reads

- An Orderly Unwind Of Market Leverage by Wolf Richter via Wolf Street

- More Couples Keeping Separate Bank Accounts by Caroline Kitchener via The Atlantic

- The Great Exodus From Blue Cities Accelerates by Kristin Tate via The Hill

- Debt-Enabled Bubble Crashing Into Demographics by Danielle Park via JugglingDynamite.com

- More Than 50% Of Americans At Risk Of Retiring Broke by Katie Brockman via Motley Fool

- New Homes Have Never Been Less Affordable by Ironman via Political Calculations

- 18-Failed Predictions Since 1st Earth Day by Mark Perry via AEI

- The Greatest Two-Year Cooling Event Just Happened by Aaron Brown via RCM

- How Not To Run Out Of Money In Retirement by Liz Weston via LA Times

- Where Alpha Really Comes From by Michael Harris via Price Action Lab

- Gender Pay Gap? Not In The Corner Office by Andrew Ross Sorkin via NYT

“The individual investor should act consistently as an investor and not as a speculator.” – Benjamin Graham

Questions, comments, suggestions – please email me.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In