by Patrick Hill

As if waking up to an economic nightmare, investors see headlines like these and many others flashing across their Bloomberg terminals:

- Facebook says Oculus headphone production will be delayed due to virus

- Apple extends country wide store closing for another week

- Foxconn delays iPhone production

- Qualcomm cuts production forecast due to virus uncertainty

- Starbucks announces China store closures through Lunar New Year, uncertain when they may reopen

- US Steel flashes a warning of a cut in demand

- Nike shoe production halted

- Under Armour missed on sales, and their outlook is weak. They partially blamed the Corona Virus outbreak.

- IEA forecasts drop in oil demand this quarter- first time in a decade

The seemingly never ending list of delays, disruptions, and cuts rolls on from retail to high technology. Even services are impacted as flights and train trips are canceled within and to and from China. While some technology-based services are provided over the Internet service, restaurants, training, and consulting, as examples, must be performed in person. Manufacturing operations require workers to be at the factory to produce products. Thus, manufacturing is much more acutely affected by quarantines, shutdowns, transportation disruption, and other government actions.

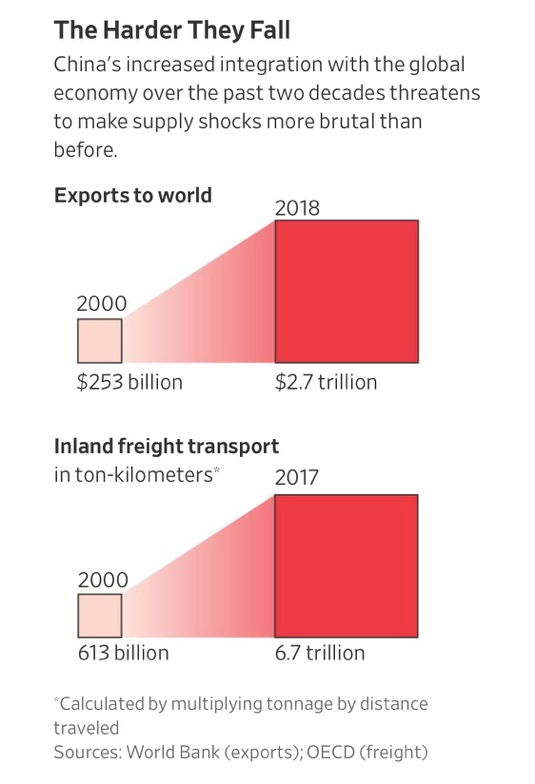

It is as if an economic tsunami is rolling over the global economy. China’s economy was 18 % of world GDP in 2019. For most S & P 100 corporations, the Asian giant is their fastest growing market at 20 – 30 % per year. Even more critical, China has become the hub of world manufacturing after entering the World Trade Organization in 2000. Over the past two decades, U.S. corporations have relocated manufacturing to China to leverage an inexpensive labor force and modern business infrastructure.

Source: The Wall Street Journal – 2/7/20

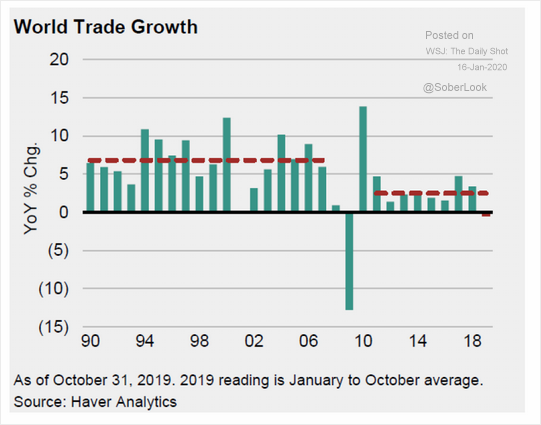

Prior to the epidemic, world trade had begun to slow as a result of the China – U.S. trade war and other tariffs. World trade for the first time since the last recession has turned negative.

Source: Haver Analytics, The Wall Street Journal, The Daily Shot – 1/19/20

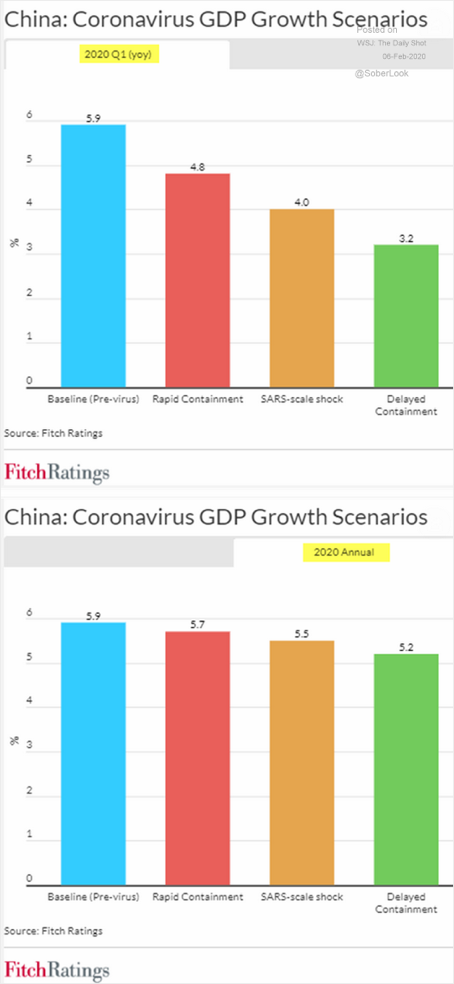

Based on severity estimates, analysts have forecasted the impact on first-quarter China GDP growth. In the chart below from Fitch Ratings, growth for first quarter drops almost in half and for year growth drops to 5.2 % if containment is delayed:

Sources: The Wall Street Journal, The Daily Shot – 2/6/20

When news of the virus first was announced, the market sustained a quick modest decline. The next day, investors were reassured by official news from China and the World Health Organization that the virus could be contained. Market valuations bounced on optimism that the world economy would see little to no damage in the first quarter of 2020. Yet, there is growing skepticism that the official tolls of the virus are short of reality. Doctors report that at the epicenter of Wuhan that officials are grossly underestimating the number of people infected and dead. The London School of Hygiene and Tropical Medicine has an epidemic model indicating there will be at least 500,000 infections at the peak in a few weeks far greater than the present 45,000 officially reported.

The reaction, and not statements, of major governments to the epidemic hint that the insider information they have received is far worse and uncertain. U.S. global airlines have canceled flights to China until mid-March and 30 other carriers have suspended flights indefinitely – severely reducing business and tourist activities. The U.S. government has urged U.S. citizens to leave the country, flown embassy staff and families back to the U.S., and elevated the alert status of China to ‘Do Not Travel’ on par with Syria and North Korea. All of these actions have angered the Chinese government. While protecting U.S. citizens from the illness it adds stress to an already tense trade relationship. To reduce trade tension, China announced a relaxation of import tariffs on $75 billion of U.S. goods, reducing tariffs by 5 to 10 %. President Xi on a telephone call with President Trump committed to complete all purchases of U.S. goods on target by the end of the year while delaying shipments temporarily. It remains to be seen if uncontrolled events will drive a deeper trade wage between the U.S. and China.

Inside China, chaos in the supply chain operations is creating great uncertainty. Workers are being told to work from home and stay away from factories for at least for another week beyond the Lunar New Year and now well into late-February. Foxconn and Tesla announced plant openings on February 10th, yet ramping up output is still an issue. It will be a challenge to staff factories as many workers are in quarantined cities and train schedules have been curtailed or canceled. Many factories are dependent on parts from other cities around the country that may have more severe restrictions on transportation and/or workers reporting to work. Thus, even when a plant is open, it is likely to be operating at limited capacity.

On February 7th, the Federal Reserve announced that while the trade war pause has improved the global economy, it cautioned that the coronavirus posed a ‘new threat to the world economy.’ The Fed is monitoring the situation. The central bank of China infused CNY 2 trillion in the last four weeks to provide fresh liquidity. The liquidity will help financially stretched Chinese companies survive for a while, but they are unlikely to be able to continue operations unless production and sales return to pre epidemic levels quickly.

Will the Federal Reserve really be able to buffer the supply chain disruption and sales declines in the first quarter of 2020? The Fed already seems overwhelmed, keeping a $1+ trillion yearly federal deficit under control and providing billions in repo financing to banks and hedge funds causing soaring prices in risk assets. While the Fed may be able to assist U.S. corporations with liquidity through a tough stretch of declining sales and supply chain disruptions, it cannot create sales or build products.

Prior to the virus crisis, CEO Confidence was at a ten year low. Then, CEO confidence levels improved a little with the Phase One trade deal driving brighter business prospects for the coming year. Now, a possible black swan epidemic has entered the world economic stage creating extreme levels of sales and operational uncertainty. Marc Benioff, CEO of Salesforce, expresses the anxiety many CEOs feel about trade:

“Because that issue (trade) is on the table, then everybody has a question mark around in some part of their business,” he said. “I mean, we’re in this strange economic time, we all know that.”

Adding to the uncertainty is a deteriorating political environment in China. During the first few weeks of December, local Wuhan officials denounced a doctor that was calling for recognition of the new virus. He later died of the disease, triggering a social media uproar over the circumstances of his treatment. Many Chinese people have posted on social media strident criticisms of the delayed government response. Academics have posted petitions for freedom of speech, laying the blame on government censors for making the virus outbreak worse. The wave of freedom calls is rising as Hong Kong protester’s messages seem to be spreading to the mainland. The calls for freedom of speech and democracy are posing a major challenge to President Xi. Food prices skyrocketed by 20 % in January with pork prices rising 116 % adding to consumer concerns. Political observers see this challenge to government policies on par with the Tiananmen Square protests in 1989. The ensuing massacre of protestors is still in the minds of many mainland people. As seems to be true of many of these events that it is not the crisis itself, but the reaction and ensuing waves of social disorder which drive a major economic impact.

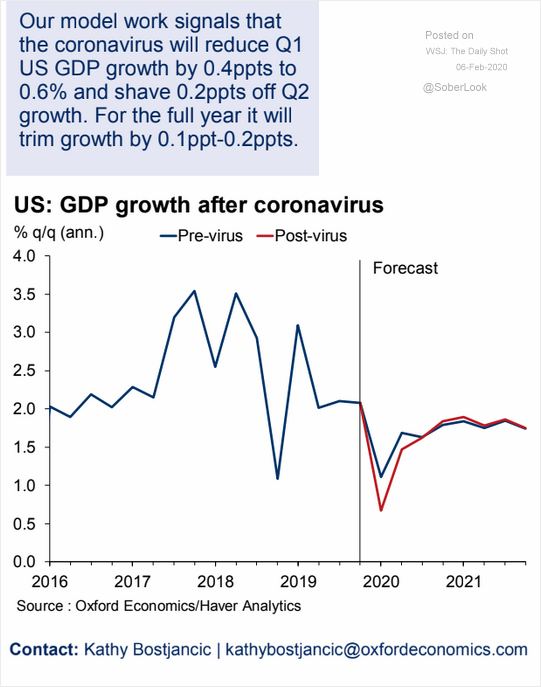

Oxford Economics has forecast a slowdown in US GDP growth in the first quarter of 2020 to just .6 %

Sources: Oxford Economics, The Wall Street Journal, The Daily Shot – 2/6/20

Will U.S. GDP growth really be shaved by just .4 %? If we consider the compounding effect of the epidemic to disrupt both demand and supply, the social chaos in China challenging government authority (i.e., Hong Kong), and a lingering trade war – these factors all make a decline into a recession a real and growing possibility. We hope the epidemic can be contained quickly and lives saved with a return to a more certain world economy. Yet, 1930s historical records show rising world nationalism, trade wars, and the fracturing of the world order does not bode well for a positive outcome. Mohammed A. El-Arian. Chief Economic Advisor at Allianz in a recent Bloomberg opinion warns of a U shaped recession or worse an L :

“I worry that many analysts do not fully appreciate the notable differences between financial and economic sudden stops. Rather than confidently declare a V, economic modelers need more time and evidence to assess the impact on the Chinese economy and the related spillovers – a consideration that is made even more important by two observations. First, the Chinese economy was already in an unusually fragile situation because of the impact of trade tensions with the U.S. Second, it has been navigating a tricky economic development transition that has snared many countries before China in the “middle income trap. All this suggests it is too early to treat the economic effects of the coronavirus on China and the global economy as easily containable, temporary and quickly reversible. Instead, analysts and modelers should respect the degree of uncertainty in play, including the inconvenient realization that the possibility of a U or, worse, an L for 2020 is still too high for comfort.”

Patrick Hill is the Editor of The Progressive Ensign, theprogressiveensign.com/ writes from the heart of Silicon Valley, leveraging 20 years of experience as an executive at firms like HP, Genentech, Verigy, Informatica, and Okta to provide investment and economic insights. Twitter: @PatrickHill1677.