by Guest Author

Eric Hickman discusses how COVID-19 has defied hyperbole.

The economic effects from COVID-19 will be devastating. Stock and asset prices will fall dramatically and will take years to recover. U.S. Treasury yields will turn negative. Sell “risk-on” assets, increase cash, and buy Treasury bonds.

The U.S., if not the world’s economy was primed for a serious recession coming into 2020. I argued in an article published on January 13 that, based on economic indicators, a U.S. recession would begin sometime before the end of 2020 and likely by March. In this context, COVID-19 was just the catalyst (albeit, a transcendent one) that tipped the world into it. Pandemic or not, the world was oversupplied and due to flush-out bad debt, weak companies and inequality. It only needed a push. China hadn’t had a recession in 42 years (since modern records have been kept in 1978), Australia in 28 years, and the U.S. in 10 years. Creative destruction had been waiting a long time.

And what a push it was. Just 10 days later (on January 23), I wrote an e-mail to my clients with an article from The Washington Post about emerging issues in Wuhan saying, “I get the sense that this is a bigger story than we are aware of.” In the ensuing months, COVID-19 has become everything.

The health side of the story is bad enough, but the economic one is worse. The combined economic effects of the global simultaneous lock-down, nine or more months of social distancing/rolling lock-down until a potential vaccine/treatment is available (the “90% Economy” as The Economist has termed it), as well as the normal deleveraging side of the business cycle (the “knock-on” effects or mentality change that usually is the recession) make for an economic contraction that will be deep (severe), wide (pervasive), and long (time).

And yet, stock markets are pricing a quick return to normal. It won’t happen. We are still in the first (dare I say, “denial”) stage; something akin to the spring of 1930 when the stock market had rallied back to be down just 19% from the 09/03/1929 peak. I suspect there are many years and chapters of COVID-19 yet to come.

At the same time, it isn’t the end of the world. If one can appreciate how it works, there are investments that will do well; but just a few.

COVID-19 Will Be Here For A While

Many prominent people and publications are saying serious things about this virus’ severity and duration:

- Bill Gates, “It is impossible to overstate the pain that people are feeling now and will continue to feel for years to come.” 4/23/2020

- German Chancellor Angela Merkel, “We are not living in the final phase of the pandemic, but still at the beginning.” 4/23/2020

- CDC Director Robert Redfield, “There’s a possibility that the assault of the virus on our nation next winter will actually be even more difficult than the one we just went through.” 4/21/2020

- WHO Special Envoy David Nabarro, “We think it’s going to be a virus that stalks the human race for quite a long time to come until we can all have a vaccine to protect us…” 4/12/2020

- Former CDC Director, Tom Frieden, “As bad as this has been so far, we’re just at the beginning.” 5/7/2020

- New York Magazine, “The FDA has never approved a vaccine for humans that is effective against any member of the coronavirus family, which includes SARS, MERS, and several that cause the common cold.” 4/20/2020

A vaccine requires several steps past finding the right formula. Once a promising discovery is made, there is animal testing, human testing, dose finding, regulatory approval, large-scale production, distribution and the issue of who pays for it. You cannot inject all humans with something until there is relative certainty it is not going to have adverse effects. Experts seem to agree that this cannot be done faster than nine months. Under the best case scenario, the world will be forced into the “90% economy” until sometime in 2021.

COVID-19 Is Still Mysterious To Scientists.

It has several phenomena that make it problematic:

- Contagious without symptoms;

- A relatively long incubation period;

- Symptoms throughout the body (i.e., blood clotting, COVID toe, organ failure);

- Unknown immunity duration after recovery; and

- Uneven virulence across strains, the population, and within an infection.

COVID-19 hit the developed world first; presumably in places where there is greater international travel. And because of that, most developed nations are now seeing a plateau or decrease in new infections (in the first wave at least). But seemingly, many developing economies are just starting their first wave. Developing economies generate the lion’s share of global GDP (estimated to be 60-70%) and thus have a large impact on the developed world.

The Economic Picture Is Serious

The economic damage already done from the lock-down as well as the idea that the world was near to a recession will result in a secular change in spending mentality that favors saving over spending.

Beyond lock-downs, the social distancing required until a potential vaccine is available has direct ramifications to economic activity. Gatherings with less density imply less demand for goods and services. Common examples are flights with empty middle seats or stadiums half-filled. Social distancing policies will enforce less economic output until a vaccine can be found and distributed broadly.

Economic data releases have been “off the charts” bad but dismissed by investors as aberrations. And as yet economists are increasingly clear that even if the economy has already bottomed (I doubt it), it will be a years-long recovery back. But the stock market is priced for a V-shaped recovery (more on this below). Investors are imagining that the new infections curve (of a given country) to be inversely correlated to its economic curve. As the new infections rate falls, the economy will come back in the same proportion. But the economic indicators are “off the charts” in the same proportion to how severe this incident is. In other words, they are real numbers and they are commensurately scary.

In any past recession, there were geographical areas or industries that were somewhat unaffected and could mitigate the heavily affected areas. In this case, whole aspects of the global economy were turned off simultaneously in a very specialized and optimized (“just-in-time”) global economy. Also, unlike older historical pandemics when it took days or weeks for news to travel, humanity knew about it at the same time, changing our economic behavior (a little or a lot) all at once. This is unprecedented in human history.

With reduced tax revenue, U.S. state, local, and municipal governments are struggling and will likely need a stimulus package of their own. If this is happening in the United States, imagine the fiscal crises that will strike less wealthy economies.

Countries that have not locked down (Sweden) or countries well on the other side of the infections curve (South Korea, China) are showing depressed economies even without the lock-down.

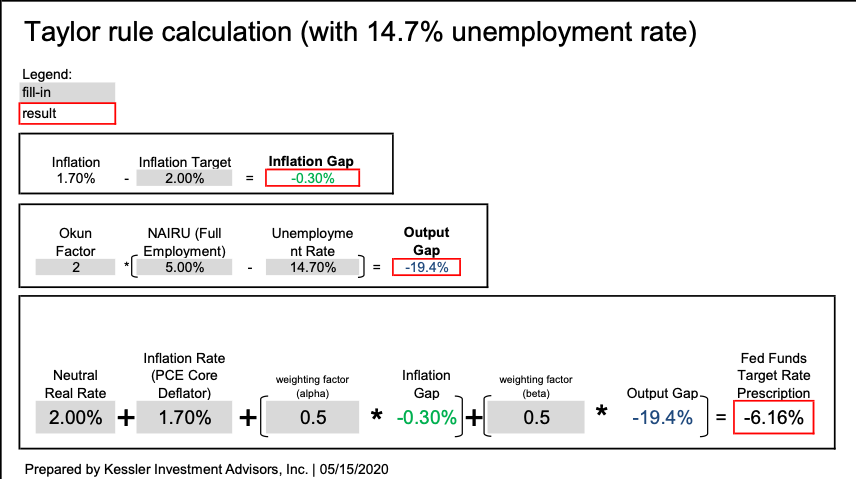

With the U.S. unemployment rate at 14.7%, the Taylor Rule implies the Fed funds rate should be less than minus -6% to be stimulating the economy. If the unemployment rate were to rise to 25% in May (per Treasury Secretary Steven Mnuchin on 05/10/2020), the Taylor Rule would suggest the Fed funds rate should be below minus -16% to be stimulative. I’m not suggesting the Fed will get to these levels, but it illustrates the scale of the crisis.

Several others have stern warnings about the economic severity of COVID-19:

- Chairman and CEO of BlackRock Larry Fink, surreptitiously, “Mass bankruptcies, empty planes, cautious consumers and an increase in the corporate tax rate to as high as 29% were part of a vision Fink sketched out on a call this week.” 05/06/2020

- Minneapolis Federal Reserve Bank President Neel Kashkari, “Large banks are eager to be part of the solution to the coronavirus crisis. The most patriotic thing they could do today would be to stop paying dividends and raise equity capital, to ensure they can endure a deep economic downturn.” 4/16/2020

- Sam Zell, “Sam Zell, the billionaire known for buying up troubled real estate, said the coronavirus pandemic will leave the same kind of impact on the economy and society as the Great Depression 80 years ago, with long-lasting changes in human behavior that imperil many business models.” 05/05/2020

- Nouriel Roubini, “The Coming Greater Depression of the 2020s,” 04/28/2020

- Warren Buffett “I don’t know that three, four years from now people will fly as many passenger miles as they did last year.” 05/02/2020

- Scott Minerd, CIO of Guggenheim Investments, “To think that the economy is going to reaccelerate in the third quarter in a V-shaped recovery to the level where gross domestic product (GDP) was prior to the pandemic is unrealistic. Four years from now the economy will most likely recover to the same level of activity that it was in January.” 4/26/2020

- Historian Niall Ferguson, “It will take much longer than people assume for the economy to recover.” 05/06/2020

Global Stock Markets Will Fall To New Lows

Prominent publications have come out with specific warnings about the stock market:

- The Economist, “A one-month bear market scarcely seems enough time to absorb all the possible bad news from the pandemic and the huge uncertainty it has created. This stock market drama has a few more acts yet.”

- Financial Times, “Equities generally are still priced for a near-perfect bounce-back from the coronavirus crisis. Lockdowns may last longer than planned. Exits may prove bumpier. Hopes that the virus can be eradicated quickly, and a second wave of infections avoided, may be proven wrong. A quick rebound to the status quo ante looks increasingly implausible. Amid so many unknowns, a further market correction looks more than likely.”

Despite it seeming as though the Federal Reserve and Treasury have spent infinite amounts of money to prop things up, it is still less than the money lost. In a general sense, if the stimulus funds were as big as the problem, economic indicators wouldn’t be weakening. Politicians never accidentally make people more than whole (in the aggregate). No matter how much liquidity there is, stocks are still ultimately beholden to corporate earnings.

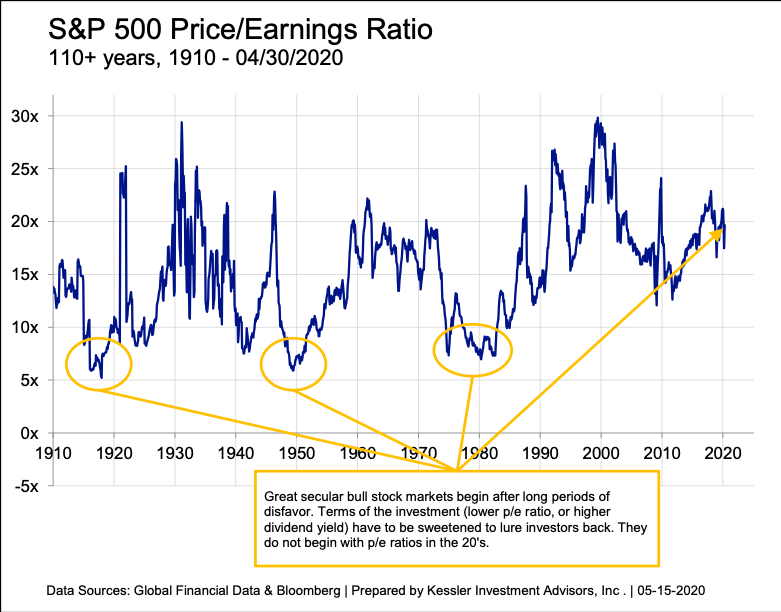

The stock market is fundamentally expensive. The price earnings ratio (trailing) of the S&P 500 is near 20. Prices will need to come down a great deal before stocks look secularly attractive. They will have to come down even further if earnings weaken materially. Multi-decade secular bull markets have begun when these ratios are below 10 (see chart below).

This is a big enough demand shock (an economic “earthquake”) that virtually any company (U.S. or international) will struggle for years. Even after the virus and economy improve, paying the huge public debt bills that economies have amassed will become the focus. Higher taxes will ultimately weigh on profitability for decades. There will be exceptions (say Clorox or Netflix, so far), but the majority will struggle.

Because COVID-19 has only been known for four months (really just three, as the markets are concerned), investors can still imagine a V-shaped recovery.

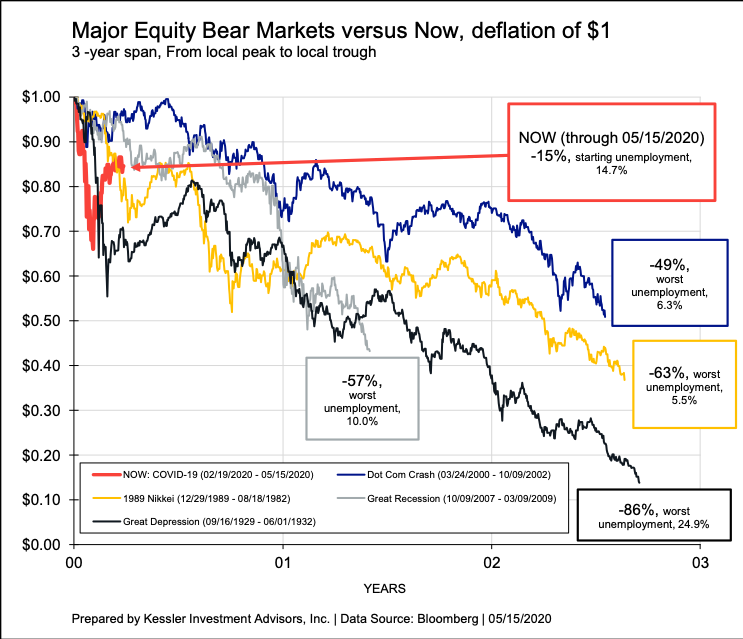

The chart below puts the U.S. stock market’s (S&P 500) performance from its recent peak in the context of past major bear markets.In this view, things have only begun. For instance, in the Great Depression, it took nearly three years from the peak to the trough. We are just four months into this.

The stock markets went down through alternating waves of hopes (prices higher) and fears (prices lower). There will be many chapters to COVID-19. We are in the first one.

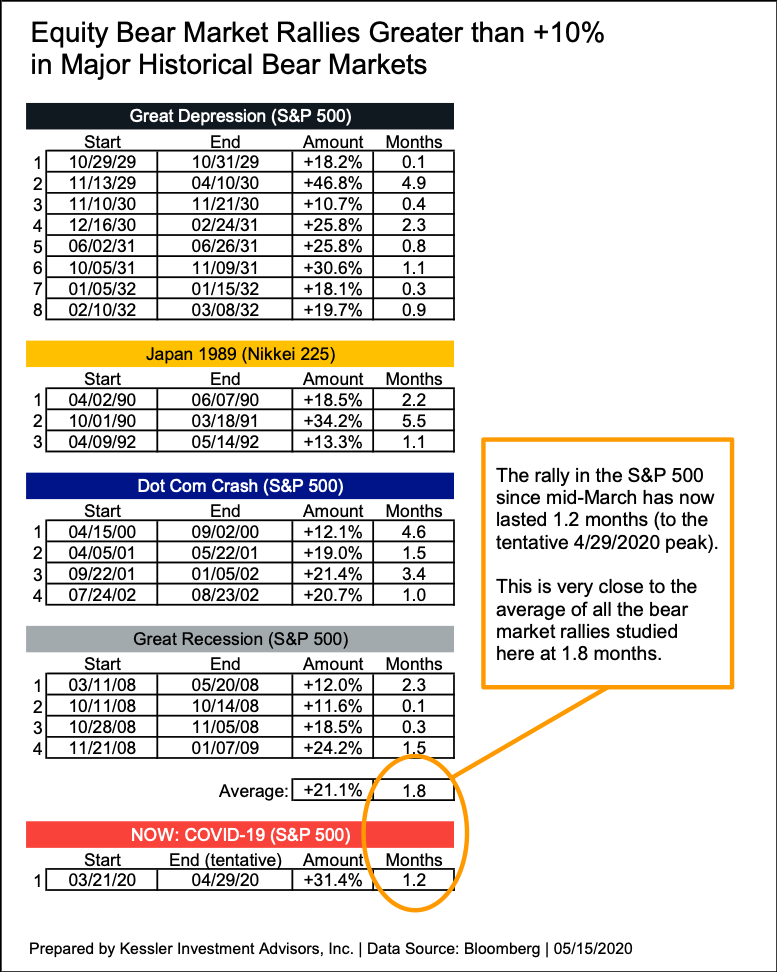

The table below shows all of the bear-market rallies greater than 10% in the cycles identified above. There were several strong rallies. The average length of those rallies was about two months (1.8). The current rally has lasted a very similar 1.2 months (assuming 04/29/2020 was the peak).

What To Invest In?

There is nothing wrong with cash.

Today, we call money not being invested “cash,” but at one time, it was just called “savings.” The importance of savings is that the money is there more than it is growing. Japan has rediscovered this dynamic in the last 30 years. Despite cash earning nothing (and it won’t again for years), if you are in cash and the stock market falls, you get to buy it back cheaper. Having cash gives an investor the freedom to invest in opportunities as they arise and be the “buyer” in a buyer’s market. Don’t think you have to invest all your money to be productive.

U.S. Treasury bonds will appreciate. They appreciate in price when yields fall and depreciate when yields rise. The more that yields move lower, the more that prices move higher. As an example, if the current 30-year Treasury’s yield were to drop from where it currently yields 1.33% (5/15/2020), to 0.75%, this bond would appreciate by 15%. If it dropped to a zero yield, it would appreciate 40%. These aren’t small returns. But bond prices decrease in the same proportion if rates were to rise.

As has already happened in Japan and Germany, U.S. Treasury interest rates will fall well below zero as this crisis intensifies. This is why:

Deflation will be the theme of the “90% economy” because it implies a 90% price. Meaning that if the economy is expected to operate 10% lower than before, supply and demand would suggest that prices (inflation) would be 10% lower too. I am not suggesting a one-time drop of 10%, but rather that there will be tremendous pressure towards lower prices (in aggregate that-is; individual sectors may have higher prices). But, it isn’t just the initial shock, there will continue to be deflationary pressure as long as the output gap is negative. That is going to take years and years to close. Deflation implies lower Treasury yields, because if prices are deflating at say 5% per year, a minus 4% yield on a Treasury would be valuable (as saving 1% over the alternative). Because of this, there is no limit to how negative Treasury rates can go, they are a function of inflation/deflation.

Given the scale of COVID-19, the Fed (and other developed economy central banks) will need to cut short-term rates deeply negative. This will pull all Treasury yields lower. I can already hear the chorus of arguments (“it hasn’t worked!”, “it creates a liquidity trap!”, “it creates hyperinflation!”) Yes, there will be tremendous resistance, but a threshold exists where the importance of protecting an industry (money market managers, banking) will pale in comparison to the economic needs of the whole country. In other words, there is a point where the Fed will alienate creditors at-large for the bigger picture. There are two prominent voices calling for negative rates so far (below), but I suspect these voices will grow in number:

- Professor of Economics and Public Policy at Harvard University Ken Rogoff, “…the Fed could push most short-term interest rates across the economy to near or below zero. Europe and Japan already have tiptoed into negative rate territory. Suppose central banks pushed back against today’s flight into government debt by going further, cutting short-term policy rates to, say, -3% or lower.” 5/4/2020

- Former President of the Minneapolis Federal Reserve Bank, Naranya Kocherlakota, “Unprecedented situations require unprecedented actions. That’s why the U.S. Federal Reserve should fight a rapidly deepening recession by taking interest rates below zero for the first time ever.” 4/24/2020

But “yield curve control” is the Fed’s next-biggest tool and I suspect it will be used before negative rates because it is more palatable to the banking and money-market industries. “Yield curve control” is a fancy way of saying that the Fed could control longer-term interest rates like they do with short-term rates. Japan is currently doing it and the U.S. did it in the 1950s. The idea is to force term rates down to, or below, a certain threshold to encourage lending. For instance, the Fed could target the 10-year Treasury yield to be 0.25% and ensure it by committing to buy enough 10-year Treasury bonds to take it there. “Committing” is the key word because if the central bank is credible enough, it doesn’t always have prove it with real capital; the threat is enough for the market to take it there. Assuming the mortgage market was functioning normally, it could help get mortgage rates down to 1%. Anyone with a mortgage can imagine how helpful that would be.

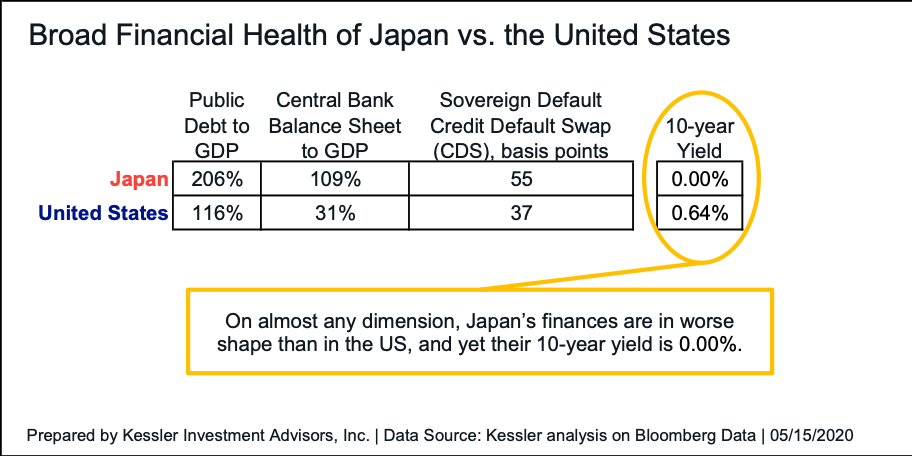

Some worry that the amount of stimulus the U.S. is spending will lead to hyper-inflation or equivalently, a weakened currency. The fiscal/monetary picture of the U.S. isn’t as extreme as it is made to be. Japan’s finances are a useful example of how far a super-power’s credit stretches. On almost any dimension, Japan’s finances are in worse shape than in the US, and yet their 10-year yield is 0.00% (see table below). Credit risk should show up first in Japan before we would see it in the U.S. They are the canary in the coal mine on this issue.

All of these things combined portend a continuing U.S. Treasury bull market (lower yields) for a few more years. Then, once everyone has given up on the stock market and P/E ratios are in the single digits, it will be time to buy stocks.

COVID-19 is the equivalent of a 300-year flood. It will be the theme of financial markets for an enduring horizon.