My former University of Chicago MBA students Ken Riggs penned this nice analysis of the current state of the commercial real estate market. Ken is Vice Chairman of RERC (Real Estate Research Corporation) in Des Moines, Iowa.

August 27, 2020

By: Ken Riggs, Vice Chair

Lucas Kane, Analyst

RERC

Best Property Type Over the Next Four Quarters: Industrial

Subtypes to Watch: Warehouse and Data Center

The investment in warehouse over the years has shifted dramatically from the smaller traditional warehouses located in clusters in major metropolitan areas to logistic last-mile delivery behemoths. As we all know, technology has changed consumer shopping behavior by enabling consumers to purchase items online. The pandemic has only intensified this trend. The advanced retail estimates for July indicated a 24.7% increase in online shopping YoY, and this has propelled the logistics industry into hyperdrive. The positive performance of these large distribution centers makes them the darlings of the market, as all major investor groups have vastly increased their capital spending in the subtype. RERC survey respondents overwhelmingly chose industrial as the best property type over the next four quarters.

But consumers’ connections to their Amazon accounts is not just downstream logistics. The link between Amazon and consumers is through data centers, another supercharged property subtype. The move to cloud computing was fueling demand for data centers way before we heard of COVID-19. According to Forbes, global internet usage has increased by as much as 70% since the pandemic broke out. As people continue to work from home, engage in online learning, and use videoconferencing and video and music streaming services, the demand for data centers will continue to grow.

Worst Property Type Over the Next Four Quarters: Hotel

Not Far Behind: Retail

Talking about being knocked to your knees! The hotel sector was beginning to face strong headwinds before the start of 2020 as supply was chugging along too fast for the demand. This imbalance or risk was reflected in RERC institutional cap rates for the sector, which started rising in 3Q 2019. COVID-19 exacerbated these problems – air travel plummeted in March before finally increasing in June and appearing to have plateaued around 50% of pre-pandemic levels. With many companies banning nonessential travel, however, the there will continue to be much less business travel than pre-COVID-19.

For retail, the hits keep coming. The already bruised sector is being walloped by the pandemic; institutional investors identified retail as one of the sectors to watch closely beyond the next four quarters. Since the outbreak of the virus, at least 25 major retailers have filed for bankruptcy. As many as 25,000 stores are expected to close in the U.S. in 2020, according to Bloomberg. In the short term, it will be difficult to backfill the vacancies. Many Class B and Class C malls will never recoup the losses.

Sector to Watch over the Next Year: Office

COVID-19’s new realities are starting to take shape. We did not initially think about potential structural changes to the office sector, but COVID-19 is redefining where and how people want to work and play. Analysts disagree about the outlook for office space demand, particularly in the dense CBD areas. Most investors, however, agree that office sector disruptions will continue until a vaccine is developed and people feel safe returning to the workplace. A PwC survey conducted in early June found that only 47% of employees believe that improved safety measures, such as wearing masks or reconfiguring layouts to allow for social distancing, would make them feel comfortable returning to work. However, it’s not easy to social distance while getting to work, especially if your only option is public transportation.

The big question is whether structural changes in the office-using sector, specifically the ability to communicate through technology and work from home, will pose dangers for long-term demand in the sector. A significant portion of the U.S.’ largest corporations, including Facebook and Google, plan to continue working entirely from remote locations until at least the middle of 2021. Though the requirement to return to the office may be at the whim of the CEO, there seems to be incentive for employers to allow remote working in the long term, even if on a partial basis. An international study of 3.1 million workers found that the workday has increased 48.5 minutes since the pandemic broke out. Even if demand for office space returns in the long term, there will likely be stark differences based on geography (e.g., urban vs. suburban) and tenant makeup, which means that cash flow analysis becomes much more important in valuations.

RERC’s Take on Investment Market Dynamics

It is all about the forecasted cash flow and a buyer’s or seller’s confidence about forecasting revenues and expenses. The trick is figuring out the revenue side, especially for hotels and retail. However, estimating operating expenses and capital costs are not far behind in being able to confidently forecast net operating income or net cash flow.

This is why we are seeing the huge bid-ask spread. Strong property types with solid cash flows are in strong demand or hold positions, and unless you offer a large premium, why sell? Conversely, for retail and hotel there is no confidence about the future cash flows. Unless you offer up a very distressed price, why should I buy?

We have yet to see the stress in selling, but we will because the extend and pretend can only last so long. Let’s see if Sam Zell reaffirms his legacy as the Grave Dancer once the market has to face realities and stand on its own without being propped up by the government.

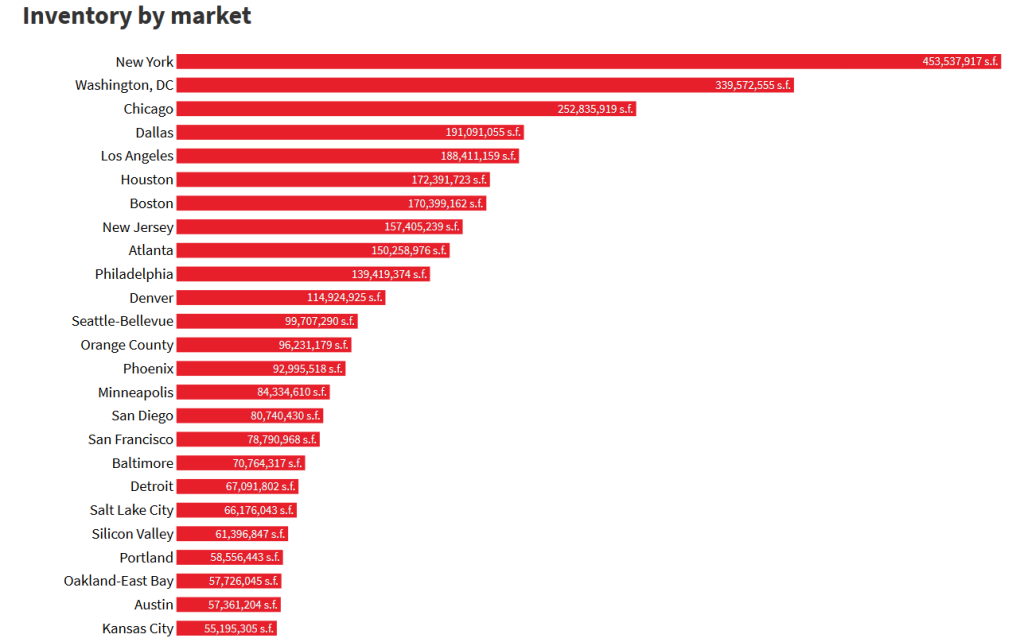

Note: Office inventory in Washington DC is second only to “Escape From …” New York. Chicago is third.