“We gathered on porches; the moon rose; we were poor.

And time went by, drawn by slow horses.

Somewhere beyond our windows shone the world.

The Great Depression had entered our souls like fog.” – Pantoum of the Great Depression – Donald Justice.

Wall Street insiders relish market troughs.

They bask sanguine in their confidence of history. Tenured pros are comforted in the belief that monetary and fiscal stimulus triggers are cocked and at the ready, reinforced in the knowledge that taxpayers without choice in the matter, will again, be the bail-out solution.

In a last irony to turn the blade in the back slowly, this group confidently takes credit for saving a system they helped to bust in the first place.

They are the strong hands who patiently await to scoop up shares when markets falter. As the smart money, these players unload inflated shares to the ‘dumb’ money or retail investors at “FOMO” or fear-of-missing-out emotional peaks.

The masses are advised to blind buy and hold. Retail investors are cajoled as “brave” if they “ride it out.” And whatever “it” is can be counted in years, even decades. Time is precious to us mere mortals. Our lives are finite; Wall Street lives on forever. The precious time it takes to break-even is ignored. Not relevant.

One of my favorite Nashville-based songwriters Drew Holcomb begins a song with a seminal line:

“Time steals every paradise I’ve been looking for.”

When Wall Street prospers, Main Street doesn’t necessarily follow a similar, prosperous path.

For example, Pew Research Center outlines that overall, American Household wealth has not fully recovered from the Great Recession. As early as 2016, median wealth of all U.S. households was $97,300; well below median wealth of $139,700 before the recession began in 2007.

Haven’t most Americans benefited from the triple-digit returns of the stock market since March 2009?

Not really.

According to the Federal Reserve’s Changes in U.S. Family Finances survey published in September 2017, median values of retirement accounts were little changed, remaining at about $60,000 in 2016. For the top income group, the rate of stock ownership, directly or indirectly, increased, continuing the trend from the 2010 survey. Stock ownership for this group was 93.6 percent in 2016.

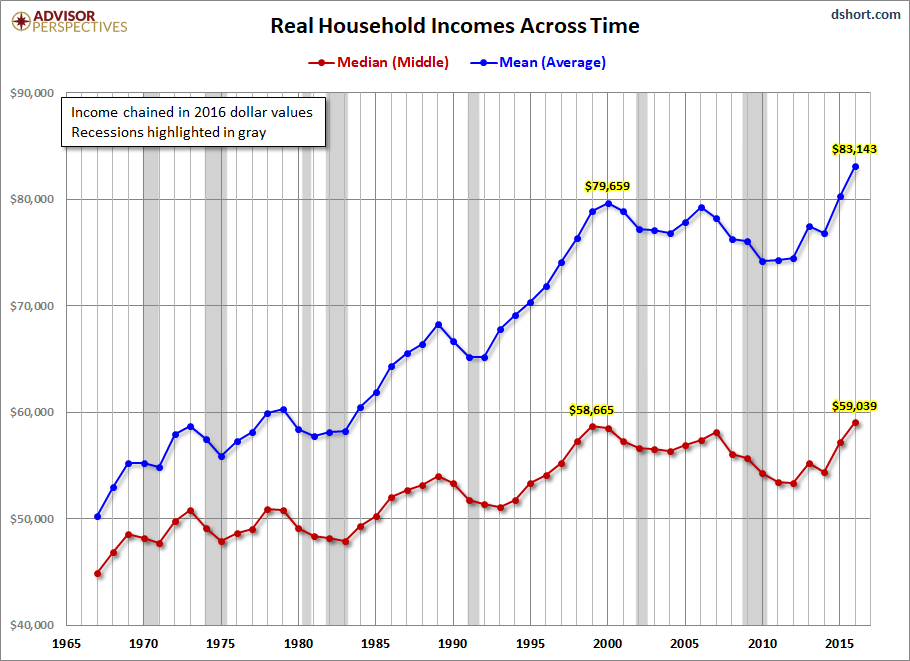

Main Street or the middle-class’ primary motivation is wages and wage growth. Appreciation of primary residences is a strong second. Finally, signs of life exist with inflation-adjusted wages (red line), exceeding 1999 levels. Notice the average (blue line), skewed by higher wage earners.

The stock market is finally paying heed to the bond market; rising rates are having a material impact on housing as 30-year mortgage rates reach an eight-year high. Increased corporate leverage is threatening to put profit margins at risk.

A spike in ten-year Treasury rates from 3.05-3.25% (3.15% at the time of this writing), was enough to get the stock market’s attention especially at a time where there was dearth of earnings news to distract it.

Also, an observation – the uncustomary silence and respectively, bearish tones from a Fed Chair and the scattered Governor minions during the recent stock market routing didn’t help. We’re not used to silent treatment from the Fed when stocks pull back or volatility picks up. Investors have gotten accustomed to the Fed jawboning the markets quiet or higher.

Fed head-honcho Powell believes the economy is running hot and he’s just the fireman to tame the flames.

Believe him.

I write this because interest rates matter; accommodative monetary, and or fiscal, policies that increase liquidity can be significant stock market catalysts, even while a majority of Main Street’s populace suffers.

As a leading indicator, markets are characterized by a counterintuitive nature that leaves investors – novice or experienced along with the general population, dumbfounded.

I thought the Great Depression, a tragic slice of American history could prove my point.

Six weeks into his new administration, FDR wasn’t fooling around. He came out of the gate as a strong, determined hand at the nation’s helm. He held strong convictions that weren’t going to be deterred. Lack of ethics in business, the excesses of the 1920s were his targets, and he had the courage to expose and correct them.

The Roosevelt Program wasn’t popular. Businesses from meat packers to investment bankers believed the Roosevelt Program spelled hardship for their businesses. It was difficult (even more so today), to separate special individual or trade business interests from their interests as citizens or units in the overall poor state of the nation.

A big disagreement at the time was what to do with current wages. A majority of business leaders were advocates for a reduction in wages as prices for goods were quickly deflating. The consumer price index fell by close to 27% from 1929 to 1933. Less wages would translate to more bodies employed. Employees would be putting in less hours in a day however, the strategy would allow additional workers to be hired. Although a good idea, the resistance was too strong.

One of the most aggressive FDR initiatives was to aggressively deflate debt for those who held farm and home mortgages. In 1933, the economic life of your everyday Americans simply couldn’t pay mortgage interest at 1929 levels. The plan was to lower interest rates dramatically from 1929 to 1933 levels. At the time, the action was deemed ‘heroic,’ by advocates.

Uncle Sam was to gather mortgages that concern the mortgagee and crush the mortgagor. The lenders to receive Federal Land Bank bonds at 4.5% as against 7-10% on present mortgages with the Federal government to guarantee the interest. Business could not revive within an environment choked by debt. The overall deflation of debt was inevitable.

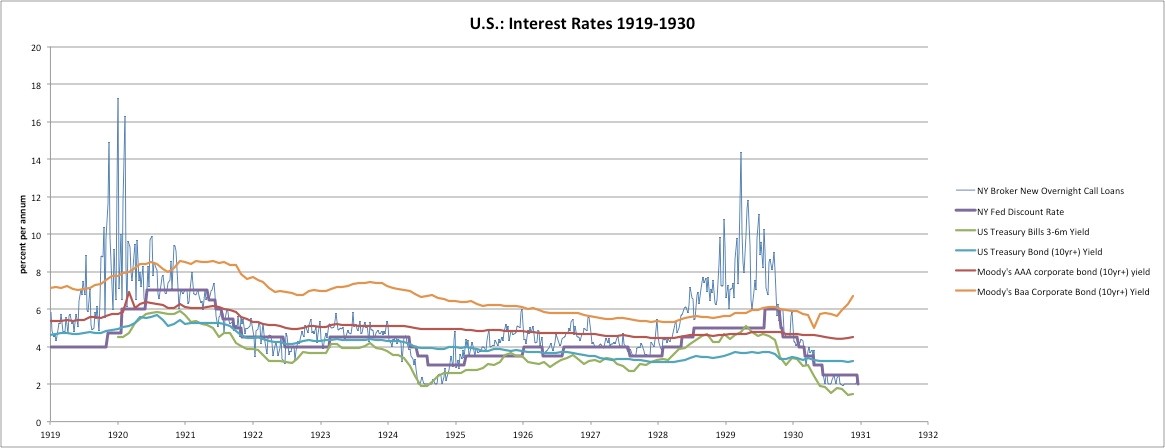

Interest rates as represented by call loan and discount, began their ascension in 1928 to cool off speculation in securities markets. By 1930, the discount rate fell from 6% to 2.5% as the Fed realized they may have overdone it to tighten the money supply.

One theory is that the Fed kept rates too low in the 1920s which was a catalyst for errant lending that lead to the great bust. Another is the money supply was too tight during the early 30s as the monetary base suffered a great decline. Deflation was a culprit, not inflation.

Consequently, the discount rate should have been close to 1% or less! In other words, The Federal Reserve’s monetary policy and interest rates were catalysts to boom and bust in the economy and markets.

Stocks had a dazzling run from 1933-1936 due to accommodative monetary and fiscal policies. The Roosevelt Program along with the money supply – M2 (M2 is cash and deposits (M1) + time deposits), bottoming and beginning to improve, sparked a hunger by Wall Street players for speculative assets like stocks. Main Street was disinterested. Unemployment was a shade lower than a tragic 25% in 1933. It fell to 16.9% in 1936.

“Hoovervilles” or tent cities remained prominent. Before 1935, there were very few relief systems in place outside of local churches and whatever services cities could provide.

But that stock market whew, what a run!

We ponder the question –

“How can the stock market do so well when the economy appears broken?”

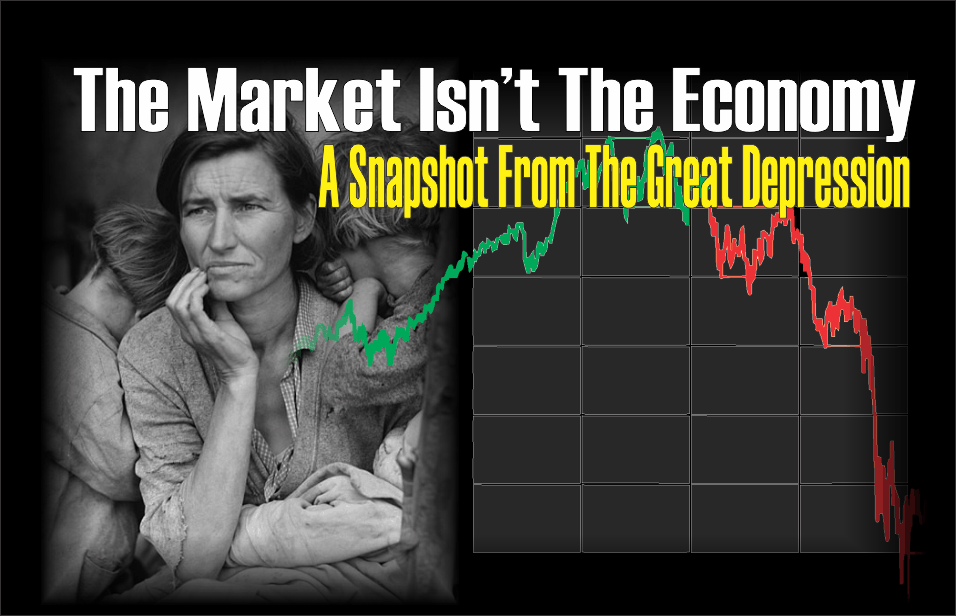

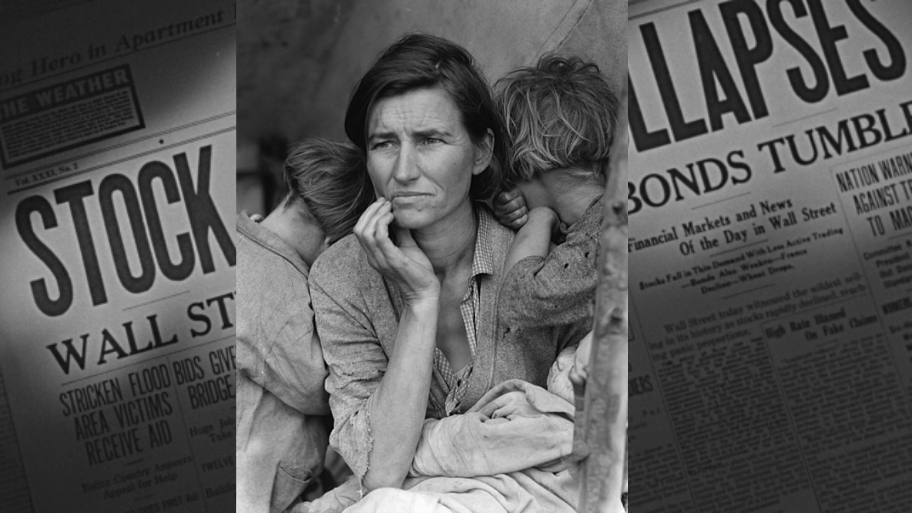

A picture does more to showcase the reality of the time than any words I share:

Here is Florence Owens Thompson. She was an iconic image of the Great Depression.

She’s 32 years old in this photo (what age does she look to you?)

Florence was a migrant worker in California in 1936. Here she is with her two children. She had seven. From 1931-1936, the stock market as represented by the Dow Jones was up 136 percent.

Now matter how you cut it, things were just fine on Wall Street.

Not so for Florence and many others at the intersection of Main Street and the Great Depression.

One lesson to never forget: Markets can and do indeed prosper during tough economic cycles due to fiscal and monetary stimulus. Markets falter when rates increase.

As the Fed continues to drain liquidity from the system, target a neutral rate, normalize (whatever that is), all of us as investors may finally understand how painful it can be for stocks, again.