Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Market still blows off Fed, Treasury selloff, and volatility in stocks.

“Leveraged loans,” extended to junk-rated and highly leveraged companies, are too risky for banks to keep on their books. Banks sell them to loan mutual funds, or they slice-and-dice them into structured Collateralized Loan Obligations (CLOs) and sell them to institutional investors. This way, the banks get the rich fees but slough off the risk to investors, such as asset managers and pension funds.

This has turned into a booming market. Issuance has soared. And given the pandemic chase for yield, the risk premium that investors are demanding to buy the highest rated “tranches” of these CLOs has dropped to the lowest since the Financial Crisis.

Mass Mutual’s investment subsidiary, Barings, has packaged leveraged loans into a $517-million CLO that is sold in “tranches” of different risk levels. The least risky tranche is rated AAA. Barings is now selling the AAA-rated tranche to investors priced at a premium of just 99 basis points (0.99 percentage points) over Libor, according to S&P Capital, cited by the Financial Times.

Also this week, New York Life is selling the top-rated tranche of a CLO at a spread of less than 100 basis over Libor. And Palmer Square Asset Management sold a $510-million CLO at a similar premium over Libor.

In the secondary markets, where the CLOs are trading, red-hot demand has already pushed spreads below 100 basis points. These are the lowest risk premiums over Libor since the Financial Crisis.

These floating-rate CLOs are attractive to asset managers in an environment of rising interest rates. If rates rise further, Libor rises in tandem, and investors would be protected against rising rates by the Libor-plus feature of the yields.

And it’s big business: In 2017, about $117 billion in new CLOs were issued in the US, which brought the total US CLOs outstanding to nearly $1 trillion.

Libor has surged in near-parallel with the US three-month Treasury yield and on Monday reached 1.83%. So the yield of Barings CLO was 2.82%. While the Libor-plus structure compensates investors for the risk of rising yields and inflation, it does not compensate investors for credit risk!

These low risk premiums over Libor are part of what constitutes the “financial conditions” that the Fed has been trying to tighten by raising its target range for the federal funds rate and by unwinding QE. It’s supposed to make borrowing a little harder and a little more costly in order to cool off the credit party.

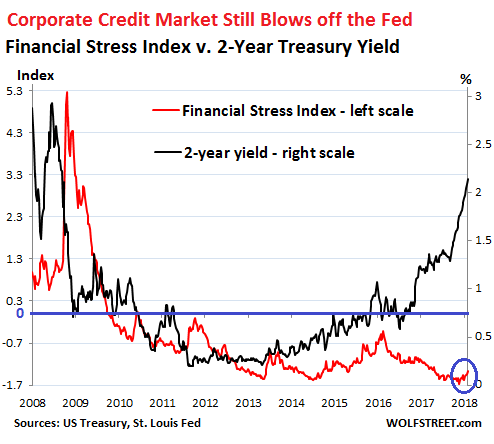

One of the measures that track whether “financial conditions” are getting “easier” or tighter is the weekly St. Louis Fed Financial Stress Index. In this index, zero represents “normal.” A negative number indicates that financial conditions are easier than “normal”; a positive number indicates that they’re tighter than “normal.”

The index, which is made up of 18 components – including six yield spreads, including one based on the 3-month Libor – had dropped to a historic low of -1.6 on November 3, 2017. Despite the Fed’s rate hikes and the accelerating QE Unwind, it has since ticked up only a smidgen and remains firmly in negative territory, at -1.35.

The Financial Stress Index and the two-year Treasury yield usually move roughly in parallel. But since July 2016, about the time the Fed stopped flip-flopping on rate hikes, the two-year yield began rising and more recently spiking, while the Financial Stress Index initially fell.

The chart below shows this disconnect between the St. Louis Fed’s Financial Stress Index (red, left scale) and the two-year Treasury yield (black, right scale). Note the tiny rise of the red line over the past few weeks (circled in blue):

The horizontal blue line marks zero of the Financial Stress Index (left scale). At or above zero is where I — after reading the tea leaves — think the Fed would like to see the index at this point. But the index is far from it. And the CLOs mentioned above are examples of just how ebullient corporate credit markets still are at every level. A similar ebullience is still visible in junk bonds as well.

The corporate credit markets are starting to take into account the risk of slightly higher inflation – hence the appetite for these floating-rate CLOs. But the risk premium over Libor and other risk premiums show that credit markets are still totally in denial about the bigger risk for junk-rated credits: the risk of default. And this risk of default surges when rates rise and financial conditions tighten as these companies have trouble refinancing their debts when they come due. But for now, investors are blithely ignoring that they’re in for a big reset.

The chorus for more rate hikes is getting louder. But no one will be ready for those mortgage rates. Read… Four Rate Hikes in 2018 as US National Debt Will Spike