Having become a master of financial engineering instead of aircraft engineering.

By Wolf Richter for WOLF STREET.

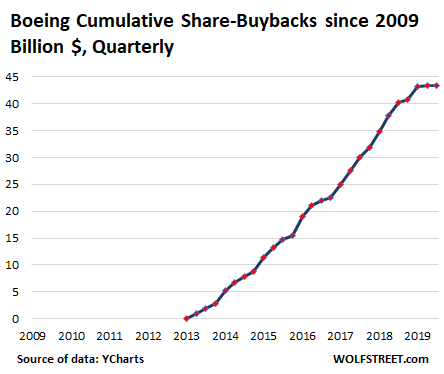

The first thing to know about Boeing’s mad scramble to line up “$10 billion or more” in new funding via a loan from a consortium of banks, on top of the $9.5 billion credit-line it obtained in October last year – efforts to somehow get through its cash-flow nightmare caused by the 737 MAX fiasco – is that the company blew, wasted, and incinerated $43.4 billion to buy back its own shares since June 2013, having become a master of financial engineering instead of aircraft engineering.

If Boeing had focused on its business – such as designing a new plane instead of doctoring an ancient design to save money and time – and if it hadn’t blown $43 billion on share-buybacks but had invested this money in a new design, those two crashes wouldn’t have occurred, and it wouldn’t have to beg for cash now. The chart below shows the cumulative share-buybacks in billions of dollars since Q1 2009. In Q2 2019, it belatedly halted the share buybacks (share buyback data from YCharts):

As is always the case with share buybacks, the idea is to buy high in order to drive shares even higher. This is what you learn on the first day of Financial Engineering 101. So Boeing stopped buying back its shares in Q1 2009 when its shares had plunged into the $35-range, at which point they were a good deal, and then recommenced share-buybacks in Q2 2013 when its shares had already risen to the $100-range.

The second thing to know about Boeing’s mad scramble to borrow another $10 billion is that it already has a huge amount of debt and other liabilities, and that its total liabilities ($136 billion) exceed its total assets ($132 billion) by about $4 billion as of September 2019, meaning that it has negative net equity, that the share buybacks have destroyed its equity, which is what share buybacks do to the balance sheet.

It also means that every dime in “cash” and “cash equivalent” listed on the balance sheet is borrowed. And this is about to get a whole lot worse. In October 2019, Boeing had already obtained a new credit line of $9.5 billion, which about doubled the size of its existing credit line. Credit lines serve as liquidity backup.

And now Boeing is scrambling to pile “$10 billion or more” in new loans on top of it.

This huge amount of cash is needed to fund the cash drain resulting from the fallout of two 737 MAX crashes, the global grounding of the planes now in its 11th month, the inability to deliver the 400 or so already built planes, the current halt in production, the squealing suppliers that have now started layoffs, the settlements with its airline customers over the grounded planes, the settlements and litigation with the families of the victims of the two crashes, the costs of dealing global regulatory issues, the collapsing sales of that plane, the scandal of Boeing’s culture revealed by corporate emails oozing to the surface, and the costs of re-engineering the software of the plane to make the plane safe to fly, amid doubts that this can even be done.

Putting a priority on financial engineering over actual engineering can get very expensive.

Now Boeing is getting closer to a deal with a group of banks, led by Citibank, for new loans of “$10 billion or more,” CNBC reported this morning, citing “people familiar with the matter.” The banks have already agreed to $6 billion of the funding so far, and Boeing is talking to other lenders to obtain more. Commitments are due by the end of this week.

The loans will have a maturity of two years and will have a delayed-draw structure that would allow Boeing to access the funds at a later time, Bloomberg reported this morning.

On January 13, Moody’s finally started stirring in bed, after sleeping through the first 10 months of all this, and announced that it would put Boeing’s debt ratings “on review for downgrade,” fearing “a more costly and protracted recovery for Boeing to restore confidence with its various market constituents, and an ensuing period of heightened operational and financial risk.”

And the upheaval among Boeing’s largest customers is growing.

Speaking today at the Airline Economics aviation finance conference in Dublin, Steven Udvar-Hazy, executive chairman of aircraft leasing company Air Lease, which has 150 of these cursed planes on order, said, according to Reuters, that his company “asked Boeing to get rid of that word MAX. I think that word MAX should go down in the history books as a bad name for an aircraft.”

“The MAX brand is damaged,” he said.

At the same conference, Aengus Kelly, CEO of aircraft leasing company AerCap, which has 100 Boeing 737 MAX planes on order, exhorted owners of these planes to not panic-dump them by leasing them at low rates or sell them cheaply, according to Reuters:

“Discipline and keeping a cool head is vital because if people panic and lease the airplane or sell the airplane at knock-down rates for an extended period of time, it will be harder for the residual value of that asset to recover.” A plunging residual value could be deadly for aircraft lessors. And he exhorted his colleagues to “be absolutely disciplined when it comes to placing the aircraft.”