Submitted by Danielle DiMartino-Booth

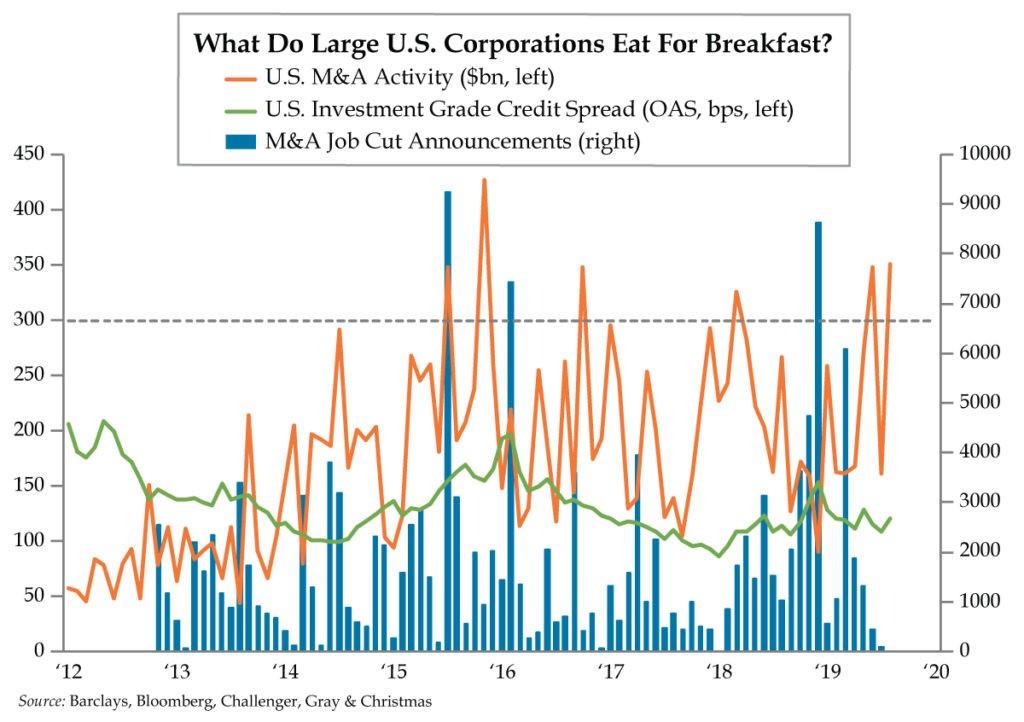

- Over the last three months, Investment Grade companies have capitalized on falling rates setting the new issuance market ablaze and inciting large-scale M&A; June and August M&A crested $300B taking the three-month total to $860B, the bulk of which is unfunded

- With large-scale M&A comes the potential to generate a bigger bump in corporate layoff announcements; while July’s job cuts tied to M&A were a scant 87, expect that number to increase substantially as acquisitions close in the coming months

- Increased IG bond supply should widen spreads into year-end; while high yield-to-IG spreads have expanded, narrowing the gap implies increased fundamental risk pushing investors to move to relative safety and dislocating the $3T ‘BBB’ bucket in the process

You probably have never heard of Kate Murtagh. She was a native of Los Angeles and an actress by training whose career spanned the second half of the 20thcentury. She lived to the age of 96, an accomplishment in its own right. But her true claim to fame might come as a surprise to avid vinyl record album collectors who could probably pick Murtagh out of a lineup. The British rock band Supertramp’s 1979 album, Breakfast in America, was RIAA-certified quadruple platinum. It sold more than four million copies in the U.S. alone and featured Murtagh depicted as the iconic waitress named “Libby” on its cover. She strikes a similar pose to that of the Statue of Liberty with New York City in the background but holds a tall glass of orange juice and a menu, rather than a torch and tabula ansata.

What got us thinking about Breakfast in America was our sixth sense kicking in. We detected something we can only describe as ravenous in our latest read of U.S. merger and acquisition (M&A) activity. “What do big U.S. corporations eat for breakfast in America?” The answer: Smaller ones.

Exxon Mobil CEO Darren Woods can attest to the growing appetite among C-Suite occupants. In a Tuesday Bloomberg story titled “Exxon Eyes Oil M&A as Clean Energy Shift Seen Taking Decades,” Woods noted that “If there is the opportunity to acquire something that bring unique value to Exxon Mobil, we’ll be in a position to transact on that.” Exxon is keeping a “watchful eye” for deals, especially in the Permian Basin where Woods is looking to scoop up someone on the cheap. We hate to break it to our bruised and battered energy investors but he’s waiting for even lower share prices of players in the space.

It’s clear that the Investment Grade (IG) credit market is open for business to fund acquisitions (or just for U.S. corporates to take advantage of cheap money). About $27 billion priced yesterday from 21 issuers, led by a $7 billion deal from Disney. Later in the day, cash-rich Apple dipped its toes in the water, announcing a similarly sized $7 billion bond sale, its first since 2017.

No surprise, part of Apple’s proceeds will go to fund acquisitions. And Tim Cook is not alone. Managed-care giant Anthem and worldwide information technology solutions company Hewlett Packard Enterprise also have funds earmarked for such purposes.

Put the micro news aside for just a second and contrast the capital raising with the surge in large-scale M&A over the last three months. Both June and August each eclipsed the $300 billion mark, a feat without comparison over ANY three-month period. What’s more, of the $860 billion in announced M&A from June to August, $758 billion, or 88%, are designated “proposed” or “pending.”

In other words, a large swath of the surge in M&A has yet to be funded. Odds are a sizable chunk makes its way through the credit market generating an increase in IG supply at a time of seasonal weakness in issuance. It’s typical for syndicate desks to rev back up in September, which is the second-half’s largest month for IG supply. After that, things tend to tail off through December in typical “close-the-books” fashion.

A separate knock-on effect of large-scale M&A is the potential to generate a bigger bump in corporate layoff announcements in the coming months. We’ve touched on the link between M&A and layoffs in past Feathers, and look to today’s Challenger, Gray & Christmas report for the latest on job cut announcements specifically caused by M&A. In July, a mere 87 were reported, the lowest number since January 2018’s record low of zero. A snapback with a vengeance is in the offing.

The upshot: technical supply factors should widen IG credit spreads through year end alongside the latest surge in M&A activity lifting jobless claims.

Ask your friendly neighborhood equity strategist how their outlook changes if credit supply and labor market risk rise in sync. Aside from first making sure their personal portfolio is hedged, they might suggest a certain disconnect is poised to be rectified.The up-in-quality trade in high yield has widened the spread to IG (adjusted for duration) to record wides. To close this gap, increased fundamental risk must force a march up the credit stack to safety, dislocating the $3 trillion ‘BBB’ bucket in the process.

You likely appreciate that fundamentals beat technicals to pressure stocks in Tuesday’s session. But that was just one day’s trading on a disappointing ISM report that embedded technicals swiftly swept aside. The turning point in sell-side sentiment we describe is rare because it’s grounded in fundamentals. You might consider a light breakfast at your desk in lieu of Libby’s sit-down service.