The Federal Reserve of New York developed the secured overnight financing rate, or SOFR, to overcome the shortcomings of LIBOR.

(Bloomberg) — It’s being called the “big bang,” and it has derivatives traders on high alert.

In a critical development in the global shift away from old benchmarks that was triggered by Libor’s shortcomings, interest-rate swaps on more than $80 trillion in notional debt will transition this weekend to a new rate for determining their value.

While the switch to the secured overnight financing rate, or SOFR, is expected to boost longer-term liquidity in the new benchmark, it also is fueling concerns about unruly price action because it is expected to trigger the sale of swaps on tens of billions of dollars of debt.

“The big bang is one of the most important steps in the Libor transition,” said Marcus Burnett, director of SOFR Academy, an education technology firm whose clients include banks and asset managers. “We expect rates desks from the largest banks in New York to be participating.”

The reset, which will see SOFR replace the effective federal funds rate in calculations that value swaps, is part of a push to make SOFR a standard U.S. reference rate in debt and derivatives markets. SOFR is intended to replace dollar Libor, which still underpins hundreds of trillions of dollars of assets such as mortgages in the U.S. and syndicated loans in Asia. The big bang follows a smaller-scale pivot in Europe this July, a less-complicated switch that occurred without much impact on the imarket.

Interest rate swaps allow two parties to trade one stream of payments for another, over a set period of time. The most common variety, known as a vanilla swap, involves exchanging payments from a fixed rate for payments from an adjustable rate that is based on Libor or some other reference rate. Another kind, known as a basis swap, involves two adjustable rates.

While SOFR has struggled to gain traction since its introduction in 2018, analysts say the upcoming big bang has already triggered a shift toward more trading in SOFR-linked swaps.

This could help pave the way for a curve that reflects expectations for where the rate will be in the future, addressing one of the new benchmark’s key weaknesses.

The big bang “will have a very, very good impact on liquidity,” said Jason Granet, chief Libor transition officer at Goldman Sachs Group Inc.

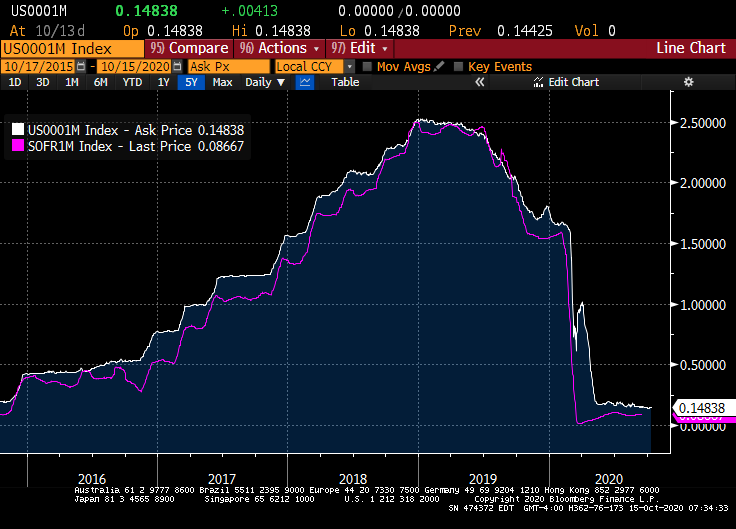

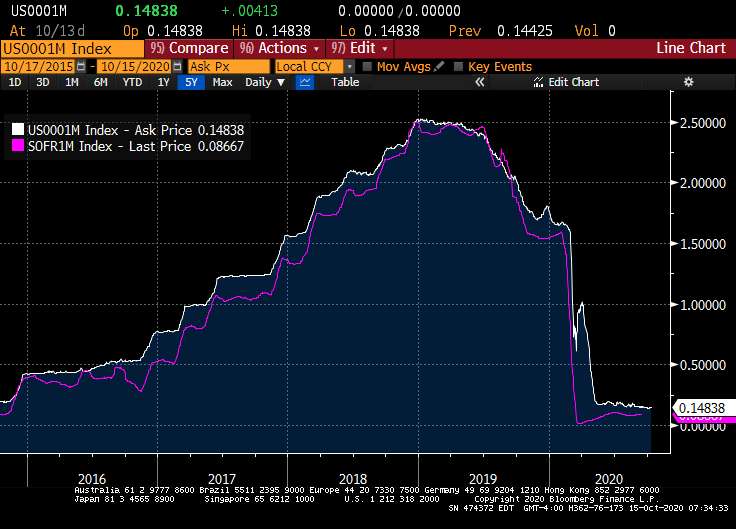

SOFR is really just The Fed Funds Target upper bound (yellow line) less 16 basis points or so.

Here is the SOFR vs Swaps curves.

Much ado about nothing?