By David Stockman

That was fast. Two weeks ago the Goldilocks Economy was being feted (again) from one end of Wall Street to the other. Today, however, January’s in-coming data brought a 6.7% annualized CPI rate and a negative 3.1% annualized retail sales print.

Can you say stagflation!

The robo machines certainly did when the Dow futures reversed by more than 400 points hard upon the 8:30 AM releases.

Indeed, even if you don’t cotton to the seasonally maladjusted monthly data prints, which we definitely do not, its hard to see the case for goldilocks even on a year over year basis.

To wit, nominal retail sales in January were up just 3.0% on a Y/Y basis, while the CPI gained 2.1%. So if consumers are the be-all and end-all of Keynesian prosperity, where’s the beef?

Certainly the measly 0.9% gain in real consumer spending since January 2017 ain’t it.

Needless to say, the underlying trends do not remotely fit the goldilocks narrative anyway. As we mentioned a few days ago, hourly wage growth for the 80% of the work force considered to be “production and non-supervisory employees” was up just 2.4% in January while the CPI has now come in at 2.1%.

So with the household savings rate having now plunged to just 2.4%, which is virtually an all-time low, how do you get a consumer spending boom out of 0.3% annual wage growth?

Indeed, how do you possibly justify the new Fed Chair’s claim that the Yellen Fed (and Bernanke too) did a splendid job of restoring full-employment prosperity, and that these policies need to be continued full speed ahead?

As Powell said at his swearing-in ceremony:

Since then, monetary policy has continued to support a full recovery in labor markets and a return to our inflation target; we have made great progress in moving much closer to those statutory objectives…..Since then, monetary policy has continued to support a full recovery in labor markets and a return to our inflation target…..

While the challenges we face are always evolving, the Fed’s approach will remain the same. Today, the global economy is recovering strongly for the first time in a decade. We are in the process of gradually normalizing both interest rate policy and our balance sheet with a view to extending the recovery and sustaining the pursuit of our objectives.

The chart below obviously douses this entire self-serving narrative with a bath of cold water. During the last 17 years, real average weekly earnings of the core work force— men 25 years and over—have not increased by a single dime (they’re actually down from $407 to $406 per week in constant 1982 dollars).

Even as the Fed’s balance sheet has soared by 9X and the value of financial assets has nearly tripledsince the year 1997, therefore, worker paychecks have been dead in the water.

So we are not inclined to call the picture below a goldilocks economy or a measure of central bank success. Instead, it points to the rotting foundation of a once thriving capitalist economy that has been strip-mined by financialization and speculation—–the only real product of Keynesian central banking.

Nevertheless, Powell’s Orwellian transformation of failure into a roaring success is not merely institutional bluster from the Eccles Building: The entirety of Wall Street believes it, and the Fed’s egregious financial bubbles are predicated upon it.

When all is said and done, of course, both ends of the Acela Corridor are bubble-blind because they are in the business of cherry-picking the data-deltas, not analyzing of underlying trends and absolute economic levels. For example, there have been numerous episodes of purported “wage growth acceleration” since the dotcom peak, but they have obviously all been transient noise, signifying nothing except $1 per week of lower real earnings.

Not only that: Long ago fundamental financial principles were tossed on the ash-heap of history—in favor of applause for any policy foolishness out of Washington that might goose the “in-coming data” for a few months or quarter; and without any regard for the longer-term adverse consequences of rampant money printing and fiscal excess.

After all, who in their right would think that the most asinine fiscal policy in modern history—a giant tax cut and spending surge which will take the FY 2019 deficit to nearly 6.0% of GDP in the 10th year of a flagging business expansion—-is good for the economy and stock market?

That’s especially the case—given the manner in which that policy was put in place. It reflects the irrational legislative lunges of a bumbling gang of Congressional Republicans who have betrayed every semblance of fiscal rectitude that was left in the so-called conservative party in order to insulate themselves politically from the whirling dervish in the Oval Office.

And for good measure, they actually took the corporal’s guard of fiscal hawks left in their ranks—-Rand Paul and the House Freedom Caucus—-out behind the Capitol and shot them dead (politically).

Stated differently, Keynesian central banking has generated what amounts to fanatical worship of the stock market, and a resulting corrupt and addled financial culture of “whatever it takes” and “any good delta will do”.

Thus, during the last iteration of the Goldilocks Economy in 2007, the Fed heads and the Wall Street talking heads alike waxed ebulliently about the “strong” incoming data and the absence of economic imbalances that might interrupt the party. And if you think that context-free, short-term monthly and quarterly rates of change (deltas) are where it’s at, everything was indeed coming up roses.

As of mid-2007, real GDP was still rising at a 2.3% rate on a Y/Y basis and job growth had remained steady, posting 1.2% to 1.6% annual gains.

Mid-2007 Goldilocks Economy

Except it wasn’t sustainable and the above picture didn’t matter. In fact, the above chart reflects more or less the normal, natural (i.e. unaided) condition of a capitalist economy. They do grow steadily owing to population gains, productivity improvement and the wealth-seeking impulses embedded in the free market.

But capitalist growth must inevitably be interrupted when state policy creates unsustainable financial bubbles, artificial economic eruptions and loss-making malinvestments. And, needless to say, that was exactly what was going on during Wall Street’s mid-2007 goldilocks bacchanalia.

The fact is, wages, household debt and housing prices were egregiously and unsustainably out of whack. As of June 2007, nominal hourly wages had risen by just 26% since January 2000. By contrast, the Case-Shiller housing price index was up by 81% and household debt had exploded by nearly 110% in barely seven years.

In a word, the trends in the chart below were infinitely more important than the short-term deltas in the Goldilocks Economy chart above. You don’t grow debt 4X faster than income for long.

Alas, the housing and debt bubbles reached their asymptote a few months later and the Fed’s Keynesian house of cards came tumbling down. In short order, the mid-2007 Goldilocks Economy turned into the disastrous picture below.

Yet neither the Fed nor Wall Street saw it coming. The Fed minutes just after the Lehman meltdown in September 2008, for example, reveal serious doubts about whether a recession had actually even commenced.

That get’s us back to the fundamental flaw in Keynesian central banking: Now that households have reached Peak Debt and the C-suites of corporate American have been turned into financial engineering joints, its patented formula of falsifying the cost of money and debt no longer works any magic on main street; it only systematically inflates financial asset prices and fuels relentless speculation and the invention of financial time bombs—- such as doubly short Vol ETFs for the homegamers and risk parity trades for the Ray Dalio’s of the world.

At length, of course, the bubbles burst and the financial time bombs—which have no economic value-added and would never emerge on the free market—blow sky high. That inexorable cycle, in turn, triggers panicked C-suite efforts to buck up share prices and rescue stock option values by means of sweeping “restructuring actions” (i.e. massive liquidation of jobs, inventories, fixed assets and inflated goodwill from failed M&A deals).

In a word, under the current regime of Keynesian central banking, the financial tail wags the main street dog. The Goldilocks Economy on main street is not a sign of sustainable prosperity; it’s the natural condition of the free market waiting to get bushwhacked by the next periodic collapse of Bubble Finance.

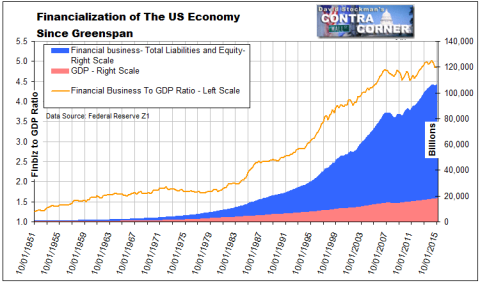

Needless to say, that’s exactly where we are now. Financialization of the US economy has continued to intensify and has now reached hideous proportions. Whereas, the total debt and equity value of the financial sector (banks, brokers, GSE’s, insurance companies, mutual funds, REITs etc) had traditionally amounted to 1.5-2.0X GDP, and had reached 3.5X on the eve of the financial crisis, it now totals more than $100 trillion and exceeds 5X GDP.

Accordingly, the financial sector amounts to a dangerous, bloated economic walrus waiting to rollover on the main street economy.

So we aren’t crediting the currently benign data-deltas during this particular reprise of the purported Goldilocks Economy, either. Like in 2007, what counts is the underlying fundamental trend, and as we showed yesterday, this time the US economy is fixed to be monkey-hammered by a doozy.

To wit, there could be no more destructive lurch of policy than the perfect storm of: (1) the eruption of giant fiscal deficits during the year-ten sell-by date of a tired business expansion; (2) an epochal pivot toward massive QT (quantitative tightening) by a greenhorn team of Keynesian central bankers who are mesmerized by their own propaganda and the Goldilocks Economy delusion; and (3) more than three decades of structural deterioration in the main street economy which has brought the net national savings right nearly down to the zero-bound.

In a word, the wholesale abandonment of fiscal responsibility by Washington could not have come at a worse time. It has left the national savings rate so out of whack—-that it is rapidly heading toward negative territory. And that’s a condition which is off-the-charts historically and which is even less logically sustainable than the housing price and debt boom that preceded the Great Financial Crisis.

Two decades ago (1997), the household savings rate was still respectable at 7.0% of disposable personal income, and amounted to $366 billion in nominal dollars. Likewise, net business savings totaled $279 billion, while government dis-saving (deficit) was just $105 billion or negative 1.0% of GDP.

Accordingly, net national savings totaled $540 billion or 6.7 % of national income. By contrast, both household savings and business savings today have diminished relative to national income, while government dis-savings totaled $806 billion or 4.2% of national income at an annual rate during Q3 2017.

Moreover, when the Federal deficit soars to $1.2 trillion in the year ahead and you add the state and local deficit to the total, the resulting $1.5 trillion of government dissaving cannot possibly be offset by business and households. Even if household savings do not deteriorate further (which would keep a tight lid of consumption spending), combined household and business savings would amount to only $1.2 trillion (Q3 2017 annual rate).

Needless to say, we think there is only one way to close the gap: Yields will soar in order to elicit higher savings and discourage gross investment. That doesn’t add up to a Goldilocks Economy in any way, shape or form.

To be sure, it is quite certain that the Donald’s new Yellen in trousers and tie has no clue that the national savings rate is fixing to pierce the zero-bound from above. He and his minions are hell-bent on replenishing their dry powder and shrinking the Fed’s elephantine balance sheet.

That will powerfully and positively strengthen the dollar (and notwithstanding its recent pure trading swoon) versus the other major currencies, whose central banks are adopting the Fed’s shift to QT on a tentative and lagging basis.

Stated differently, the other central banks and sovereign authorities are likely to be selling USTs—directly or indirectly—to prevent their currencies from plummeting. Consequently, as we will address in Part 4, the off-shore financing of the US economy will likely reach its sell-by date as well.

Just since the eve of the financial crisis, the US economy has effectively borrowed $6 trillion from abroad. And that’s surely another unsustainability that’s lurking below the placid surface of the Goldilocks Economy 2.0.

Mr. Stockman makes a strong case.