Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

But other construction segments are hot.

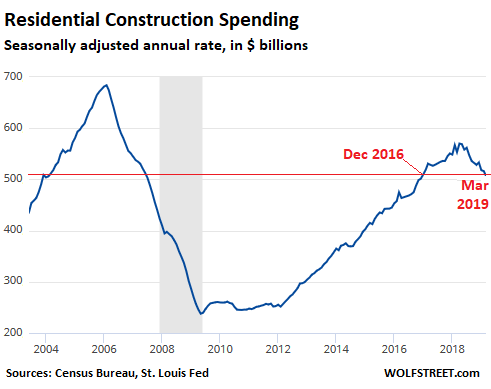

Residential construction is starting to make folks nervous. Total residential construction spending – 99% is “private” rather than “public” spending – dropped 8.4% from a year ago, the sixth month in a row of year-over-year declines, to a seasonally adjusted annual rate of $507 billion, according to the Census Bureau this morning. This was down 11% from the peak in April 2018, and the lowest annual rate since December 2016.

Residential construction spending never fully recovered from the 65% collapse following the peak in February 2006 ($684 billion annual rate) that led 22 months later to the official start date of the Great Recession. For months now, residential construction spending has once again been heading south in a disconcerting way:

Construction spending is a major factor in the US economy with big local consequences, including well-paid jobs whose economic benefits ricochet to local businesses from car dealers to sandwich shops.

In 2006, residential construction was the equivalent of 4.5% of nominal GDP ($13.8 billion). When residential construction collapsed from $650 billion in 2006 to $250 billion in 2009, it took a big bite out of the economy. But it no longer plays this kind of huge role. In 2018, residential construction was down to about 2.2% of nominal GDP ($20.5 billion), and the current downturn in residential construction is being felt less.

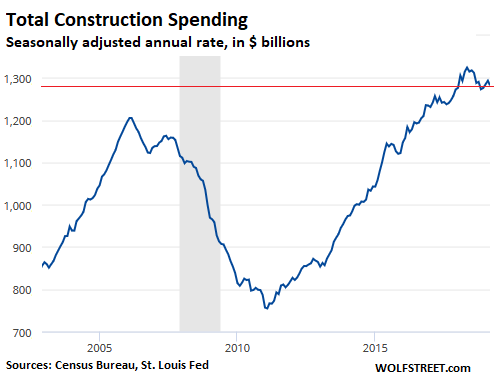

Overall construction spending – thanks to the diminished role of residential construction spending – inched down only 0.8% in March, compared to March last year, the second month in a row of year-over-year declines, to a seasonally adjusted annual rate of $1.28 trillion:

Annual rate means that at this pace, construction spending for the whole year would total $1.28 trillion.

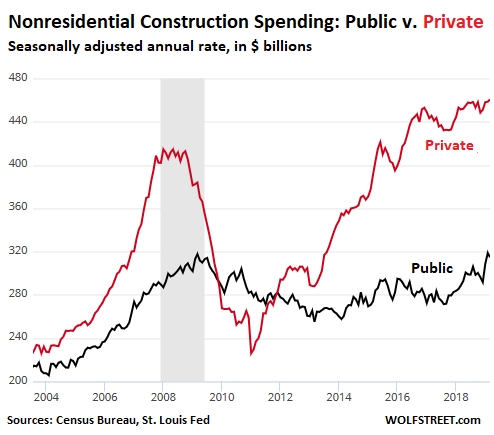

With residential construction declining sharply, nonresidential construction came to fill the holes – and much of the heavily lifting, so to speak, was done by the public, by federal, state, and municipal governments (bridges, sewer projects, administrative buildings, etc.):

- Private nonresidential construction (red line) rose 2.1% year over year to $461 billion annual rate

- Public nonresidential construction (black line) soared 9.0% year-over year to $315 billion annual rate

During the Great Recession, private nonresidential construction spending collapsed by over 40% in a short period of time, from an annual rate of $420 billion to $240 billion. Public construction rose until March 2009, and then as states and municipalities got squeezed by the budgetary effects of the Great Recession, with California famously running out of money and having to pay bills with IOUs for the second time in its history, projects got trimmed back or cancelled, and public construction spending began to decline.

It took 10 years, and 10 years of inflation, to bring public construction back to where it had been in March 2009. This was boosted by a surge that started at the end of 2017: in those 15 months, public construction spending jumped 11%.

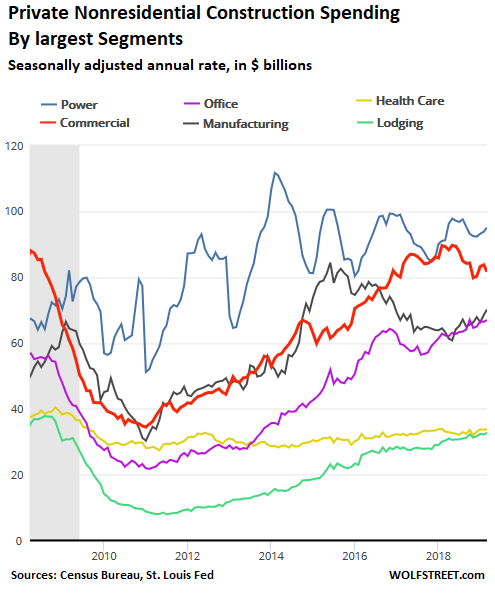

Private nonresidential construction spending is growing at a red-hot pace in some segments and declining at a red-hot pace and one segment, “commercial,” mostly warehouses and retail – the effects of the brick-and-mortar mortar meltdown on the construction of shopping malls.

Here are the largest segments, with year-over-year growth rates in March (amounts in seasonally adjusted annual rates):

- Power (blue line in the chart): +4.2%, to $95 billion

- Commercial (red line): -8.6%, to $82 billion

- Manufacturing (black line): +10.9%, to $70 billion

- Office (purple): +7.5%, to $67 billion,

- Lodging (green): +8.0%, to $33 billion

- Healthcare (yellow): +2.4%, to $34 billion.

Construction of manufacturing facilities (black line) grew strongly starting in 2011, peaked and turned around in mid-2015 when the oil bust hit equipment and supplies manufactures and when truck makers were hit by the transportation recession. It bottomed out in May 2018, and has since started to recover.

So what could tip overall construction spending into a steeper decline? A recession could and will. But barring that scenario, public construction looks to be on a growth path, especially if a significant infrastructure plan gets passed by Congress. And most major private nonresidential construction segments are on a growth track as well. Their growth will have to counterbalance falling commercial and residential construction in order for overall construction spending to not decline at a faster pace.