Its been one year since Covid struck (I ended up in a hospital for 2 weeks with Covid) and office markets since haven’t recovered.

Washington D.C., the government is still leasing.

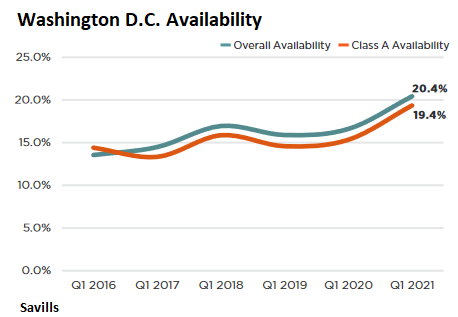

Amid surging sublease space, total availability jumped to 20.4%, “the highest in at least three decades,” as “tenants wait to lease space, lease less space, or return space to market,” according to Savills’s Washington DC report.

Total leasing activity dropped 33% year-over-year to 1.2 msf. Of this activity, near half came from federal and local government agencies.

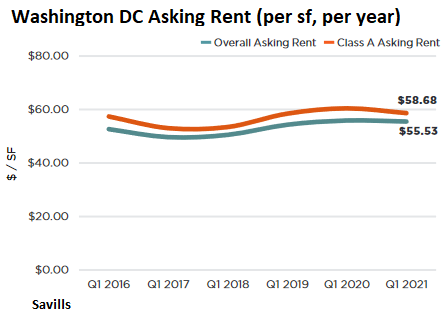

Overall asking rent ticked down to $55.53 psf per year. But “owners are being aggressive in pricing, concessions and flexibility to attract and retain tenants,” said the report. “New long-term Class A leases receive on average $148.00 psf in tenant improvement allowances and 21 months of free rent, totaling $260.00 psf in value – an increase of just over $50.00 psf since the start of the pandemic – significantly reducing tenant effective rent.” (Chart via Savills).

As Houston has shown, office markets can be in very tough slumps for years, while developers continue to build the latest and greatest office towers. In Houston, despite years of slump, there are still over 3 msf of office space under construction, though that’s down 28% from the 10-year average, according to JLL.

And when that type of long slump occurs, there is a flight to quality, with companies moving to the latest and greatest towers when their old lease terminates, and abandoning older office buildings, whose landlords might ultimately walk away from the mortgage and let the lenders worry about the collateral.

The question isn’t what to do with the latest and greatest office towers, because they will always find tenants. The question is what to do with older office buildings whose tenants move out when the lease allows them to, as part of the flight to quality. It’s those older office towers – or rather their creditors – that are in trouble when the slump drags on.

Houston has been for years the toughest major office market for landlords, after a historic office-tower construction boom collided with the Great American Oil Bust that started in 2015 and reached a crazy paroxysm in April 2020, with benchmark crude oil grade WTI collapsing briefly to minus $37 a barrel in the futures market. During 2020, hundreds of oil and gas companies filed for bankruptcy, most of them in Texas. On top of it came the Pandemic’s shift to working from home.

It is becoming increasingly clear, as companies announced their plans, that there is a long-term shift to a hybrid model, with some employees working permanently from home, others working in the office nearly all the time, and many others working from home part of the time, and showing up at the office part of the time, with hot-desking and big lounge-type meeting areas taking over desk farms. And companies can reduce their office footprints.

And now Houston is getting lots of red-hot competition in terms of vacant office space from big expensive office markets, such as San Francisco, Los Angeles, Manhattan, Chicago, Washington DC, and others.

Houston, still the toughest office market.

The available office space rose to 54.8 million square feet (msf), or 31.6% of total inventory in Q1, according to real estate and investment management services provider JLL. Available space includes vacant, sublease, and still occupied office space now being marketed as available for lease. JLL named the causes: “bankruptcies, downsizings, and layoffs.”

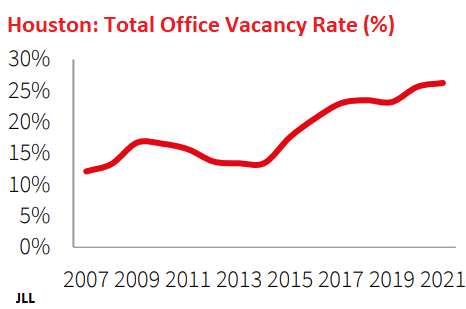

The total office vacancy rate rose for the fifth quarter in a row and hit 26.2%. Of the 19 submarkets, 15 experienced occupancy losses during the quarter (chart via JLL):

“Large blocks of sublease space continue to arrive to market,” JLL said. In Q1, sublease availability jumped to 6.4 msf.

When companies are leasing office space that they no longer need due to downsizing, or never needed in the first place and were just leasing for potential future use, they can put the space on the market as a sublease. And because they’re just trying to cover some of their costs and don’t need to make money on the subleases, they can do so at much lower rents than direct leases by landlords. And this is happening massively.

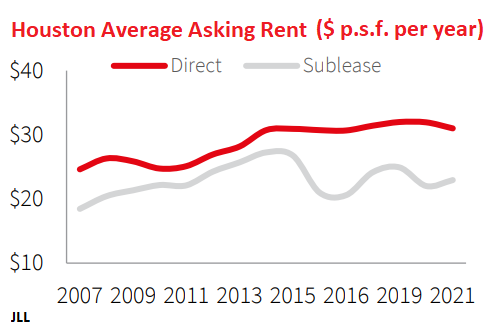

Overall asking rents have started to tick down (red line) to $31 per square foot (psf) per year, but sublease asking rents are 26% lower, at $22.93 psf. Asking rents are the advertised rents. But landlords may work out a more attractive deal with their tenants, including concessions, free rent, and improvement allowances (chart via JLL):

Total market-wide leasing volume in Q1 plunged 66% from the five-year average to 1.3 msf, as “tenants continued to postpone leasing decisions.”

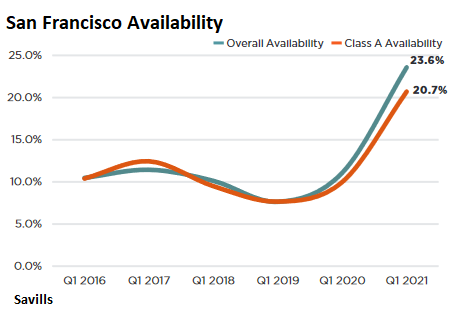

San Francisco, once one of the hottest office markets, suddenly approaches Houston.

Sublease inventory rose by another 200,000 sf to a new historic high in Q1 of 8.9 msf, according to real estate services provider Savills. Last year, San Francisco’s sublease space blew by Houston’s 6.4 msf, though Houston’s office market is over twice the size of San Francisco’s.

The total availability rate rose to 23.6%, from the single digits two years ago (chart via Savills):

“Current conditions will present an unprecedented opportunity for occupiers to secure space in a once incredibly tight leasing environment as owners will soon need to compete with the tsunami of sublease space,” Savills said in its San Francisco Market Report. It’s how a presumed office shortage suddenly turns into a majestic office glut.

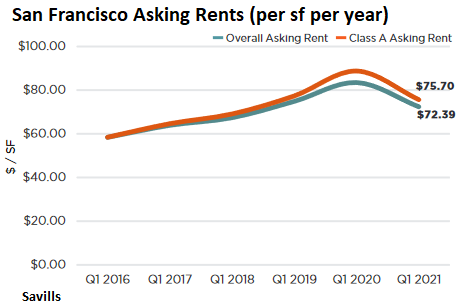

Overall asking rents have declined by 13% and Class A asking rents by 15% year-over-year. According to Savills: “With the glut of available space on the market, expect additional decline in coming quarters as landlords shift from a ‘closed market’ phase into a repricing stage once tenants’ appetite for space begins to re-emerge in full and the sublease market becomes real competition.” (Chart via Savills).

Leasing activity has collapsed, with just 0.4 msf leased, down 75% from 1.6 msf in Q1 2020 and down 85% from 2.5 msf in Q1 2019. Of the leases that were signed, over half were lease renewals.

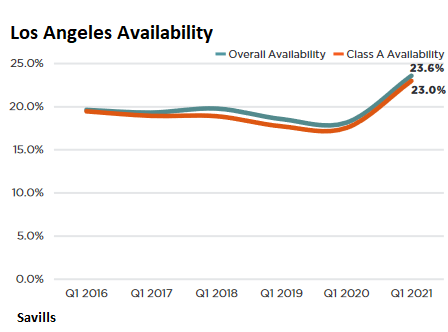

Los Angeles.

Office availability rose to 23.6% in Q1, the highest since 2009, according to Savills’ Los Angeles Market Report. Subleases space soared to 9.0 msf. And ‘“shadow” availability – space which is available but not currently advertised – will be a bigger issue in 2021, especially in trophy buildings,” the report said (chart via Savills).

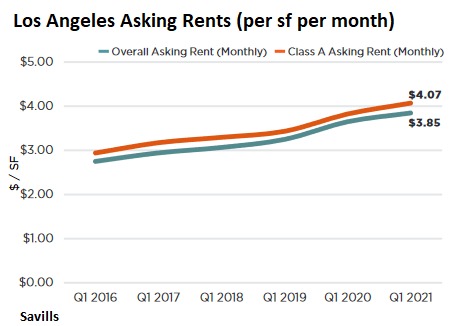

Leasing activity in Q1 plunged by 49% from a year ago to 2.0 msf. But asking rents “remain stubbornly high” and ticked up to $3.85 per square foot per month (or $46.20 per year)

“As seen in the past few quarters, the current elevated asking rents are misleading as landlords will have to be aggressive in securing tenants in the face of softer market conditions. Concessions such as parking abatement and contraction rights [a right in the lease to reduce the size of the office at a future date] have become prevalent again and are not expected to go away anytime soon,” according to Savills.

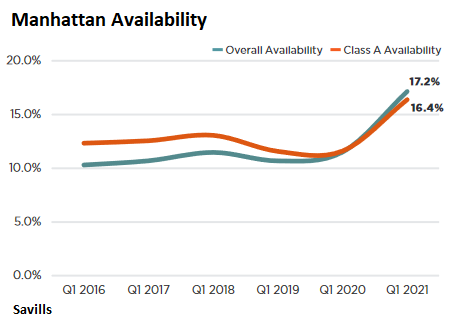

Manhattan, the biggie.

In the largest office market in the US, availability soared to 17.2%, “the highest level in at least three decades,” according to Savills, “with both direct and sublease space continuing to flood the market.” Sublease availability jumped 3.4 msf in Q1 to 22 msf. And an additional 7.9 msf of direct space came on the market, including “some notable additions from a few shuttered coworking locations.” (Chart via Savills).

Leasing activity in Q1 plunged by 48% year-over-year and by 13.7% from Q4, to 4.0 msf.

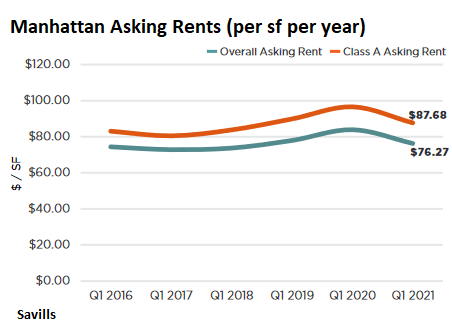

The average asking rent dropped by 9.1% year-over-year to $76.27 psf per year. Not included in asking rents are concessions which, for new long-term Class A leases, “increased substantially;” In addition, average tenant improvement allowance rose by 15.5% to $124.85 psf, and average free rent rose 17.4% to 13.5 months, according to Savills.

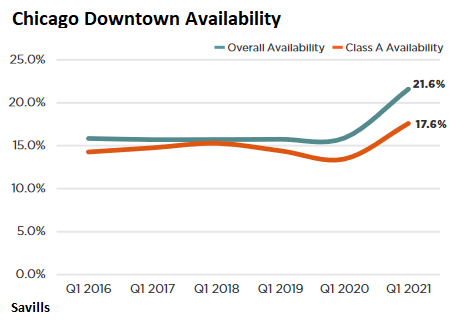

Downtown Chicago.

Total availability jumped to 21.6%, exhibiting “no signs of slowing down,” according to Savills’ Chicago report. In the Central Loop, availability surged to 24.3% (chart via Savills):

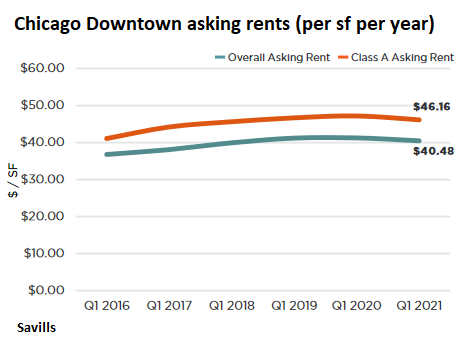

Despite Q1 leasing activity solidly stuck in collapse mode, down by 73.5% year-over-year, landlords have not budged much on asking rents. But “many landlords have shown inclination for heavily discounted rents, increased concessions, and significant flexibility for occupiers who are active and ready to make leasing decisions,” the report said (chart via Savills).

Savill’s covers other cities like Atlanta and Philadelphia. Sorry Columbus and Cleveland Ohio … you aren’t big enough to justify a Savills report. BUT, most US cities are the same story …. slow recovery from Covid.