by Golem XIV

On Wednesday Feb 7th 2007 HSBC issued a profit warning. It was the first in its 142 year history. It told its share holders it would have to take an unprecedented charge of $10.5 billion because one of its units, its sub prime lender, was in deep trouble. And so began the sub prime crisis.

Today GE issued a profit warning and cut it divided to share holders from 12 cents to 1 cent. It is only the third time since the Great Depression that GE has reduced its dividend in this way. It told its share holders it would be taking a $22 Billion charge because one of its units, its power unite, is in deep trouble.

In 2007 the banks had flooded the global market with sub-prime loans. The banks were also holding many of those same loans themselves or had transferred them to Special Purpose Vehicles (SPVs) they had set up, staffed and lent money to.

Today it is not the banking world which stands at the centre of the storm but the corporate world. In the last years they have flooded the market with junk rated bonds. At the same time they are also burdened with high yielding, leveraged and convent light loans. Taken together they are about $2.4 Trillion of debt.

2007 sub prime loans. 2018 corporate junk bonds and leveraged loans. 2007 banks and SPVs funded by the banks. 2018?

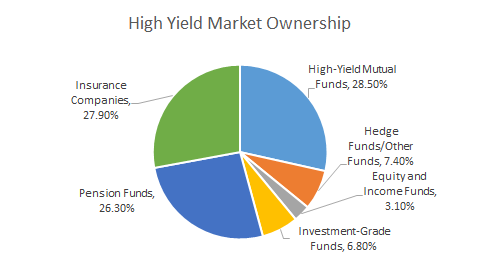

Where is this debt sitting today?

Nearly half sits in Insurance Companies and Pension funds.

Given the close ties between insurance and pensions this is not a happy picture.

Along side the pension and insurance industry who are sitting on a mountain of high risk/high return junk there is the liquidity trigger of bond backed, fixed income and high yield ETF’s. They are admittedly still small compared to the still larger mutual funds but they are a choke and panic point. The ETF market is broad in its consumer appeal but very narrow where it counts – in who makes and provides the heavy lifting for the market. There are about 5 main companies which ‘Sponsor’ which means run and control ETF’s globally. They are BlackRock, Vanguard, State Street, Invesco and Charles Schwab. According to Forbes in 2017,

Five Largest ETF Providers Manage Almost 90% Of The $3 Trillion U.S. ETF Industry

Of those 5,

…the top 3 ETF providers dominate the market with a combined market share of 82% … the top-three players also account for more than 70% of all ETF assets globally.

The sponsors in turn rely for the heavy financial lifting – to buy and sell the assets that go into an ETF, on what are called the Authorised Participants. Whoa re they? The main ones are … the big banks like Merrill Lynch, Fortis bank, Morgan Stanley, HSBC, Barclays, Citi etc. Some companies are both sponsor and authorised participant.

And some of those banks are also the people who have extended the leveraged loans and revolving credit lines to GE and others. As well as buying their bonds to put into their ETFs.

What could possibly go wrong?

Well… the Fed is trying to ‘normalise its balance sheet by withdrawing some of its liquidity. It is also trying to let interest rates rise. Taken together this is the Fed trying to bring to a much postponed end, the temporary and extraordinary measures brought in to deal with the little 2008 sub prime blip. The ECB is also trying to reduce its vast 2.4 trillion euro bond buying stimulus package of the last three years. Though it has said it will not raise interest rates till late next year. While over in China the central bank has, as far as I can see, lost control and is now more reactive than proactive. It has again and again tried tho reduce official lending and hold back the flood of shadow bank lending that fuels the property speculation market that is the centre of all regional ‘development’ and social stability in China.

Corporates are floundering in a river of debt of their own creation. They are the ones who have taken on loans they will not be able to pay if interest rates increase even a little. The banks have packaged up and sold on that leveraged loan debt and those junk bonds and they have been gobbled up by pensions and insurance companies desperate for yield after a decade of ‘temporary’ low interest rates.

This time it will not be the banks that trigger it. Not HSBC or Countrywide but GE or Caterpillar. The companies who have been propping up their share prices with endless buy backs funded by… low interest rate loans and junk bond issues. Or perhaps it will be the corporates who are merging and acquiring. Last time the top of the market was marked by and to some extent triggered by that wave of vast bank purchases. HSBC was early when in 2003 it bought one of the largest subprime lenders in america, Household International for $15 billion. Bank of America bought Merril Lynch. RBS bought ABM Ambro. Hypo bought Depfa. Every one of them saddled the purchaser with unmanageable debt and most ended in massive bail outs.

Today it is the turn of the corporates. 2016 Bayer bought Monsanto. Funded with $15 billion in bond sales. 2017 CVS, a retail pharmacy and health care company bought Aetna which is a health insurer for $70 billion 40 billion of which was funded by a bond issue. 2018, American health provider and insurer, Cygna bought Express Scripts. Funded by a $20 billion bond issue. 2015 AT&T bought DirectTV. Funded by debt. 2018 AT&T bought Time Warner. Funded by debt. AT&T’s total debt is now around $180 billion which is a larger debt than many countries. Just yesterday IBM bought RedHat for $34 billion of which about $20 billion will be backed by new debt.

Buy backs supporting share prices and while huge acquisitions attempt to capture market share or buy growth that the parent can’t generate themselves and all funded by debt.

Of course you could say that issuing bonds insulates the corporates because the interest on those bonds is fixed. Quite so. The question I would ask is who bought those bonds and what with? Was it debt?