Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

The once hot asset class of high-end student housing runs into reality.

“Student housing” is no longer the spartan cramped dorm room. It’s a global asset class. Part of this subcategory of multifamily apartment properties has gone up-scale, and the mortgages to fund these properties, just like the mortgages that fund regular apartment buildings, are packaged into commercial mortgage backed securities (CMBS) – including by the Government Sponsored Enterprises, such as Fannie Mae – and sold to investors. But the private sector has carved out a niche in packaging student housing into CMBS. And that’s a good thing for taxpayers, because these “private-label CMBS” are now going delinquent in large numbers.

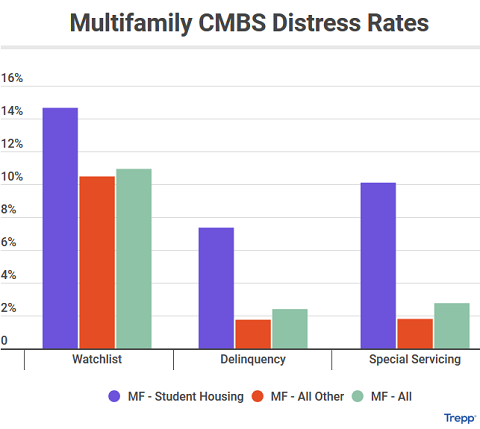

In August, the percentage of student-housing CMBS that were delinquent and have been turned over to a special servicer spiked to 7.3% of total outstanding balances, according to Trepp, which analyzes CMBS. The rate of CMBS that aren’t delinquent yet but have already been turned over to a special servicer rose to 2.8% of the total outstanding. And so, the combined rate of student housing CMBS in special servicing has jumped to 10.1% (purple bar on the right, chart via Trepp):

In addition, another 14.6% of Student-housing CMBS that are not yet delinquent and have not been turned over to special servicing are now on the watchlist (purple bar on the left in the above chart).

In dollar terms: Of the $4.5 billion in private-label student housing CMBS, $331 million are delinquent as of August, and $123 million, while still current, are already in special servicing. In total, $454 million, out of $4.5 billion, are in special servicing.

But for the recent vintages of CMBS, the delinquency rate is a lot higher: $1.5 billion of the $4.5 billion in student housing CMBS are backed by mortgages on properties that were constructed in 2010 or later. According to Trepp, many of these mortgages were securitized into CMBS within two years after construction, “meaning little or no operating history was provided.” The delinquency rate of these CMBS has spiked to 15.3%!

This comes on a backdrop of loose money, low interest rates, and historically low default rates by other multifamily CMBS: With student housing excluded, only 1.8% of the remaining multifamily CMBS are in special servicing (red bar on the right in the chart above).

In broader terms, the Trepp delinquency rate for all CMBS in August fell to another post-Financial Crisis low of 2.5%. Even the battered brick-and-mortar retail CMBS sported a delinquency rate, at 4.1%, that was far lower than the student housing delinquency rate.

But the student housing sector was once red-hot with investors. According to the Green Street Commercial Property Price Index, prices of student housing properties soared 56% from the peak before the Financial Crisis. In fact, the property price index for student housing barely dipped during the Financial Crisis, before it took off gain.

But the sector faces some challenges, including:

Oversupply of luxury student housing units. Not only oversupply, but also the whole notion of “luxury student housing” in the era of crushing student debt. Sure, some students are floating in moolah, but most students are struggling to get by. An insider who has been working in student-housing construction for many years told me:

“I was always shocked by the luxury and presumption of entitlement embedded in the marketing, such as top of the line fitness facilities when there is already a fieldhouse on campus, appliance packages for people who never cook but eat at the cafeteria, etc. All this has added to the cost and to student debt.”

Falling student enrollment. According to the National Center for Education Statistics, total undergraduate student enrollment surged by 37% between 2000 and 2010, from 13.2 million to 18.1 million students — thus whetting the appetite for the student housing industry. But then came the Financial Crisis and other factors such as soaring tuition, and to the greatest surprise of the industry, total enrollment has since declined by 7% through 2017, to 16.8 million students.

Thus, even as supply of high-end student housing is increasing, the supply of students, so to speak, is declining.

The issue with student housing isn’t the low end. There is always demand for affordable student housing. It’s at the high end where things are cracking – and more precisely at a specific corner of high-end. Trepp:

Generally speaking, the student housing market is relatively barbelled in terms of inventory quality.

One end consists of older, lower-end developments with more dated amenity offerings. Since “low end” housing construction is constrained and most campuses have a steady supply of frugal students as well as money-conscious parents, this part of the market usual soldiers on.

On the other end, there is a constant new supply of amenity-rich multifamily units coming onboard – which has triggered – as we like to say – the “student housing amenity race.” The housing options that find it hardest to compete are those complexes that were amenity-rich 10 years ago and remain pricey, but now seem dated.

At these older high-end properties, so the 2010-plus vintages, landlords can’t keep up their occupancy levels, given the already limited number of students who can afford them and the onslaught of new high-end student housing, and given the requirement to charge uncompetitive premium rents to service the debt. Hence, the CMBS delinquency rate on these older vintages that has soared to 15%.

Clearly, many graduates who are now struggling with piles of student loans lived in low-end student housing or outright dumps, trying to get by, in line with the bifurcation among American consumers.

But in the era of relentlessly soaring student debt [The State of the American Debt Slaves, Q2 2019]…

…and in the era of campaign promises (whatever they’re worth) of forgiving part of this student debt at the expense of taxpayers, the whole notion of “luxury student housing” and how it was funded and securitized and sold to investors, and how those involved profited along the way, clarifies the role of the University-Corporate-Financial Complex, and how it has hooked into the government-guaranteed money flow. And students are just the conduit.

Services are Hopping. The #1 Biggie is Hopping the Fastest. It all adds to GDP! Read... The Financialization of the US Economy