Helicopter Money for Wall Street & the Wealthy: $2.06 Trillion in 5 Weeks. Regular folks, forget it.

By Wolf Richter for WOLF STREET.

Since the Fed announced its market bailouts and interventions on March 15, it has printed and handed to Wall Street $2.06 trillion. But here is the thing: This was front-loaded, and over the past two weeks, it has cut its bailouts in half, and it has stopped lending new funds to its SPVs that were expected to buy all manner of securities, including equities, junk bonds, and old bicycles. But those loan amounts haven’t moved in four weeks. What it has bought were Treasury securities and mortgage-backed securities – and it’s cutting back on those too.

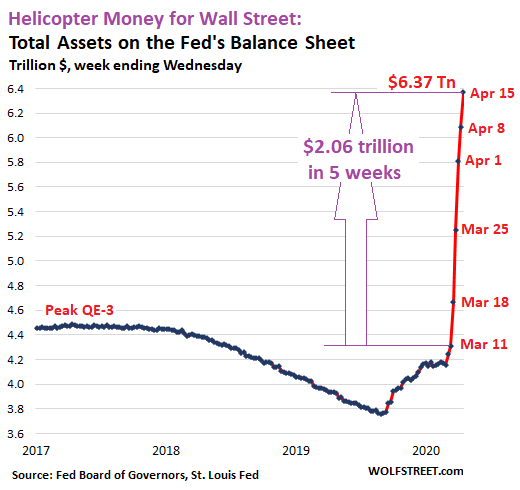

Total assets on the Fed’s balance sheet rose by $285 billion during the week through April 15, reported Thursday afternoon, to $6.37 trillion. Over the past five weeks, including the partial bailout-week which started March 16 and ended March 18, total assets increased by these amounts. Note the big taper from $586 billion and $557 billion early on to $287 billion in the latest week:

- $356 billion (Mar 18, partial bailout week started Mar 16)

- $586 billion (Mar 25)

- $557 billion (Apr 1)

- $272 billion (Apr 8)

- $285 billion (Apr 15)

The $6.37 trillion of assets on the Fed’s balance sheet are mostly composed of Treasury securities, mortgage-backed securities (MBS), repurchase agreements (repos), “foreign central bank liquidity swaps,” and “loans” to its Special Purpose Vehicles (SPVs). We’ll go through them one at a time.

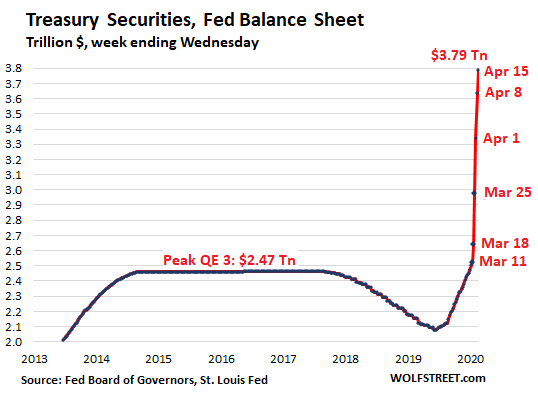

Treasury securities purchases get slashed.

The Fed added $154 billion in Treasury securities during the week, down 47% from the $293 billion it had added the week before, and down 57% from the $362 billion it had added two week ago. This is a major factor in the Big Taper of QE-4.

The sharp reduction in purchases of Treasuries confirms for now that the Fed is sticking to its announcement that it would drastically cut QE after the initial blast.

Fed Chair Jerome Powell in a webcast on April 10 said that the Fed would pack away its emergency tools once “private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth.” Whatever that means.

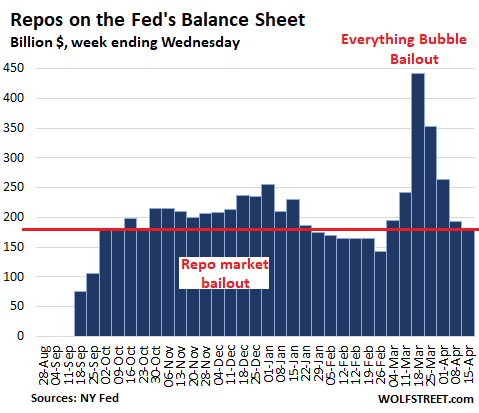

Repos fizzle further.

The Fed was offering gazillion per day in overnight repos plus over a gazillion a week in term repos. But since the beginning of its asset purchases, repos have receded into the background, and there have been few takers. The Fed has now reduced its offerings. And there is only a trickle of activity. Repo balances on the Fed’s balance sheet have now dropped to $181 billion. This decline in repos also contributes to the Big Taper of QE-4:

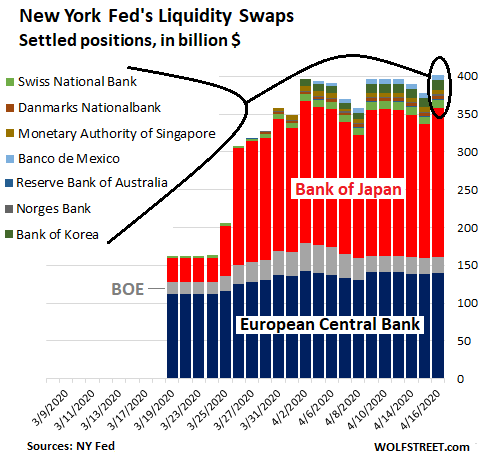

Central Bank Liquidity Swaps: BOJ & ECB

The Fed has “dollar liquidity swap lines” with the ECB, the Bank of Japan, and the central banks of Canada, England, Australia, New Zealand, Norway, Sweden, Switzerland, Denmark, Singapore, South Korea, Brazil, and Mexico. The total on its balance sheet increased by $20 billion from the prior week to $378 billion but has been in the same range all April. Of note:

- 83% of outstanding liquidity swaps are with the ECB ($138 billion) and the BOJ ($176 billion).

- The Bank of England is far behind ($22 billion).

- And there no swaps with the central banks of Canada, Brazil, New Zealand, and Sweden.

The chart below shows daily balances by country. The balance sheet is for the week ended Wednesday. But the chart also includes Thursday (right column):

Under these swap agreements, the Fed lends newly created dollars to the other central bank and takes their newly created domestic currency as collateral. The exchange rate is the market rate at the time of the contract. These swaps have a maturity of 7 days or 84 days. When the swaps mature, the Fed gets its dollars back, and the other central bank gets its own currency back. The Fed carries these swaps on its balance sheet valued in dollars at the exchange of the agreement.

Why do the ECB and BOJ want dollars?

The ECB and the Bank of Japan – the biggest users of the swaps – preside over export-focused economies that both have large trade surpluses with the US and through those surpluses obtain a constant flow of dollars.

In addition, their currencies are the second and third largest global reserve currencies (dollar’s share down to 61.8%; euro’s share at 20.1%; yen’s share at 5.6%).

Further, the BOJ’s foreign exchange reserves include $1.2 trillion in US Treasury securities.

In other words, neither the ECB nor the BOJ need the dollars for trade. They need them to support their banks and companies have large dollar-denominated debts and speculative bets that they need to refinanced with cheap dollars. And those swaps make that possible.

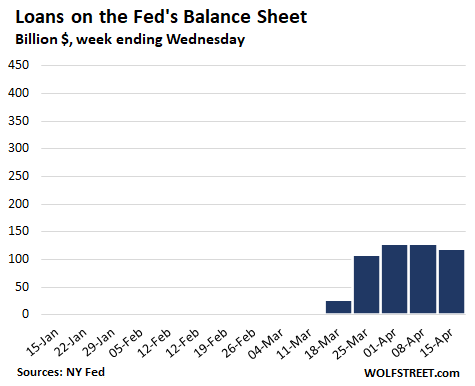

“Loans” stalled.

The category of “Loans” is a group of accounts that track what the Fed lends to its SPVs that it set up and what it lends to its Primary Dealers (the big broker-dealers and banks it does business with). The Fed can lend money to these SPVs which then can buy – even though it would be illegal for the Fed itself to buy – all kinds of stuff, including corporate bonds, junk bonds, equities, and what not. There was a burst of activity four weeks ago, but nothing has happened since then.

The balances of “Loans” fell to $120 billion (from $129 billion the prior two weeks). The chart is on the same vertical scale as the repo chart. After the initial burst, nothing:

As you can see in the chart above, the Fed has purchased practically nothing over the past weeks… just jawboning the markets. The loans by category:

- Primary credit: $41 billion, down from $43 billion. Expanded recently to include “fallen angel” junk bonds, but the Fed hasn’t bought any yet. The amounts outstanding predated the “fallen angel” expansion.

- Secondary credit: $0 (to purchase corporate bonds, bond ETFs, and even junk-bond ETFs). But none were purchased.

- Primary Dealer Credit Facility: $35.6 billion (up from $33 billion)

- Money Market Mutual Fund Liquidity Facility: $52 billion (down from $53 billion). This is the money market bailout where a few weeks ago the Fed bought corporate paper and other assets. No additions since the initial burst.

Note that “Secondary credit, which has been expanded to buy corporate bonds and junk-bond ETFs, has a zero balance. The Fed hasn’t bought anything yet. It has just been jawboning. And that was enough to trigger a huge rally in bond ETFs, including the iShares iBoxx high-yield corporate bond ETF.

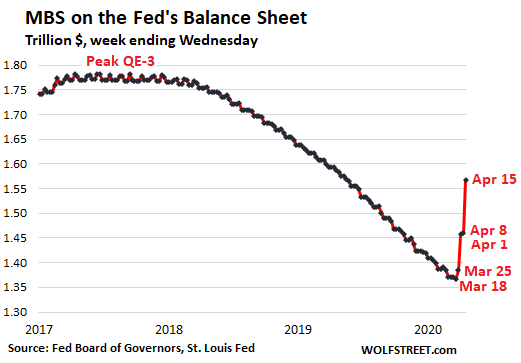

MBS.

The Fed has drastically cut its purchases of MBS over the past two weeks, as reported by the New York Fed:

- $157 billion (week ended Mar 25)

- $145 billion (week ended Apr 1)

- $109 billion (week ended Apr 8)

- $59 billion (week ended Apr 15)

But there are two complications with MBS.

One, holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down or are paid off. Given the boom in mortgage refinancing due to the lower interest rates, these pass-through principal payments have become a tsunami. Just to maintain its balance of MBS, the Fed would need to buy a significant amount every week.

Two, MBS trades take a while to settle, and the Fed books the trades only after they settled. So what we’re seeing on the Fed’s balance sheet lags the actual trades by some time.

The increase of $108 billion is a mix of these two: purchases from the big burst on March 25 and April 1 that finally settled minus the pass-through principal payments it received:

If…

Since March 11, the Fed printed $2.06 trillion and handed it to Wall Street and asset holders. The sole purpose of this was to inflate asset prices and bail out asset holders. The potential crumbs offered to small businesses or the real economy have not happened yet.

If the Fed had sent that $2.06 Trillion to the 130 million households in the US, each household would have received $15,800. But forget it, this was helicopter money for Wall Street and for asset holders – particular those with the riskiest bets – and for no one else.