Then there are the dividends it pays its member banks.

By Wolf Richter for WOLF STREET.

In addition to a lot of smaller activities, the Federal Reserve does two financially huge things: in 2019, it held about $4 trillion in interest-bearing assets, mostly Treasury securities and mortgage-backed securities (MBS); and it owed banks about $1.5 trillion in interest-bearing reserves. Among its other activities, are its reverse-repo activities, and the costs of its own operations. On Friday, the Fed reported its preliminary results for 2019, including how much it paid the banks ($35 billion), how much it paid the counterparties of its reverse repos ($6 billion), how much it remitted back to the US Treasury Department ($54.9 billion), and how much it paid in dividends.

The Revenues:

The Fed earned $102.8 billion in interest income from the Treasury securities and MBS it held in 2019. This was down 8.5% from the $112.3 billion it earned in 2018, in part because Quantitative Tightening, with extended into July, reduced the pile of interest-bearing assets on the Fed’s balance sheet. It also earned $444 million from “services.”

The Expenses:

What it paid the banks: The Fed paid its member banks (there are over 3,000 of them) interest due on required and excess reserves that banks have on deposit at the Fed. Those reserves on deposit at the Fed — liabilities on the Fed’s balance sheet — averaged about $1.5 trillion in 2019, but had been declining through September. Also, starting at the end of July, the Fed cut rates three times, including the rate it pays on reserves. So the interest the Fed paid the banks on these reserves fell 9.1% from a year earlier, to $35.0 billion.

Note that if banks had not deposited those funds at the Fed, they would have likely bought Treasury securities for at least part of it and would have earned about the same or a higher rate of interest from the US government. When banks sit on large amounts of reserves, they’re going to try to make money off them, one way or the other.

What the Fed paid its reverse-repo counterparties: The Fed paid $6.0 billion in interest to its counterparties on securities it sold under reverse repurchase agreements (the opposite of repos). Reverse repo balances are liabilities on the Fed’s balance sheet. The Fed has been doing reverse repos for a long time. Balances started surging in 2014, peaking at over $500 billion. Then in 2017, balances started declining. In 2019, they averaged around $270 billion.

The Fed’s own operating expenses amounted to $4.5 billion.

Other expenses: The Fed also incurred expenses of $837 million related to producing, issuing, and retiring currency; $814 million for Board of Governors expenditures; and $519 million to fund the operations of the Consumer Financial Protection Bureau.

Net income and where it went:

After it was all said and done (income minus expenses), the Fed had an estimated net income of $55.5 billion in 2019. Final data will be published in its audited annual report.

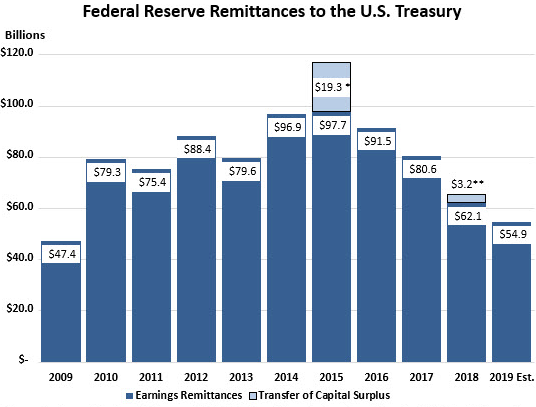

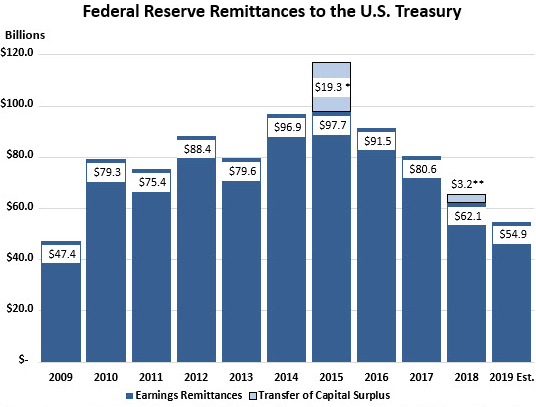

Every year, the Fed remits nearly all of its net income to the US Treasury department. For 2019, it remits $54.9 billion. This is down from a remittance of $65.3 billion for 2018 (chart vie the Federal Reserve):

The circularity: The US Treasury borrows money to fund the US deficit. This borrowing takes the form of selling Treasury securities. The Fed buys and holds a chunk of this debt, and like others gets paid interest on this debt. After it funds its operations and pays interest to the banks and counterparties, the Fed then pays the US government back what’s left over.

Dividends to its member banks. The 12 regional Federal Reserve Banks are private companies whose shares are owned by the financial institutions in their districts. The Fed pays dividends to the shareholders of the 12 regional FRBs. These dividend payments are determined by federal statute. For 2019, the Fed paid $714 million in dividends to these financial institutions.

Though $714 million in dividend payments sounds like a lot, but compared to the $35 billion the Fed paid the banks in interest, it’s practically a rounding error. Anything denominated in millions is a rounding error at the Fed where the big things are denominated in trillions. That’s the times we live in.