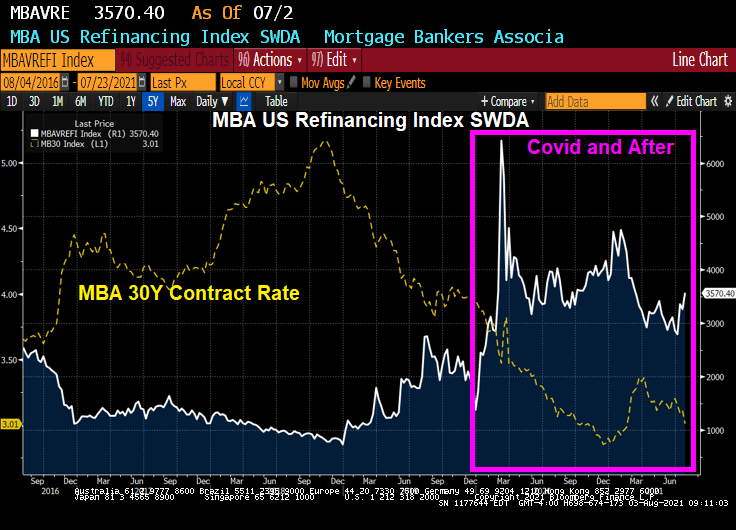

Things have not been the same since the Covid outbreak in early 2020. And that includes mortgage refinancing.

As The Fed poured on the gas to the economy, mortgage rates (that were already declining) fell further stimulating a refinancing wave in March 2020 that has remained elevated since compared to pre-Covid levels.

But if The Fed taking its monstrous foot off the mortgage refi accelerator pedal?

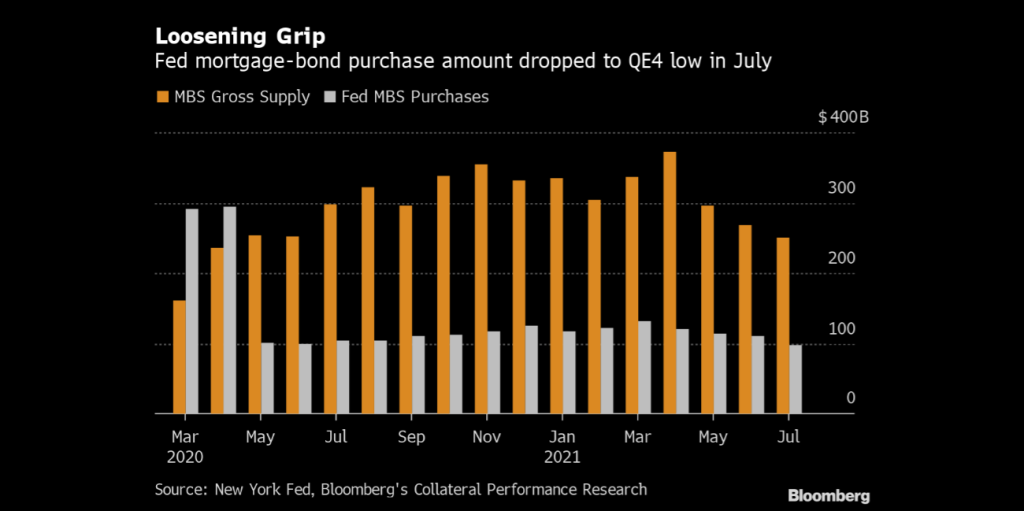

(Bloomberg) — The Federal Reserve purchased the least amount of bonds in July since the beginning of this round of quantitative easing, at least in dollar terms.

This isn’t due to any tapering on the part of the central bank, but the result of the recent slowdown in the prepayments seen in the $2.4 trillion already on their balance sheet. As the Fed isn’t only adding $40 billion each month to their holdings, but reinvesting all these paydowns back into mortgages as well, a slowdown in prepayments leads to a drop in support for the sector, albeit with a lag.

Last month saw the Fed purchased just $98.2 billion in mortgage bonds, the lowest amount for any calendar month since QE4 began in March 2020. Overall gross supply for Fannie Mae, Freddie Mac and Ginnie Mae came in at $249.9 billion in July, down 7% from June and the third straight month of decline, according to data from Bloomberg’s Collateral Performance Research tool.

So luckily for mortgage bond investors, this drop off in the central bank’s support came during the same month when agency mortgage supply declined. In fact, agency mortgage bond gross supply last month was the lowest since April 2020.

Putting aside the two out-sized months of March and April 2020 — when the Fed purchased all gross mortgage supply — average monthly Fed purchases have been $112.7 billion.

While in dollar terms the Fed support saw a steep decline — down 11.4% from June and 12.9% below the monthly average seen since May 2020 — on the basis of what percentage of total gross supply was taken down, July was right in line at 39.3%. The average, excluding March and April 2020, has been 37%.

The latest Fed schedule calls for $54 billion of purchases over the next two weeks, which if maintained over the entire month implies about $108 billion for August, which is right on its monthly average in dollar terms.

The overriding question for mortgage investors is when will the Fed begin to taper its support. With the lockdowns already having dealt a harsh blow to the economy and a rising threat of more to come as the Delta variant spreads, it’s arguable that the Fed may continue QE at its current pace for longer than many are forecasting.

The agency mortgage sector ended Monday with the entire UMBS 30-year coupons underperforming their hedges for a second day in a row. After a tough July, investors are hoping to see a turnabout but valuations are still tight.

The rally in Treasuries has left mortgage unable to keep up, with the U.S. 10-year yield crossing the 3 p.m. ET mark at 1.18% on Monday, down five basis points and its lowest since Feb. 11, according to data compiled by Bloomberg News.

This week’s economic data releases will bring the July prepayment speed report Thursday afternoon, which is expected to see aggregate Fannie Mae 30-year speeds drop about 5% from the previous month.

To allow families to save more money, lenders will no longer be required to pay the Enterprises a 50-basis point fee when they deliver refinanced mortgages. (FHFA Eliminates Adverse Market Refinance Fee, July 16, 2021)

Here we go again. The Biden Administration is pushing Fannie Mae and Freddie Mac to increase homeownership rates by lowering credit standards. And now taking the safety off the mortgage refinancing torpedo.