Is that a red flashing light on the control panel of “the man behind the curtain”?

Among the many “interesting” (a safe word to use in perilous times) signs and portents swirling around us, here are five financial tidbits “of interest.” What do they mean? The answer is of course nothing. There are many “interesting” things with no discernible meaning. Being “interesting” is enough.

1. Just like in 2000, proponents claim “this time it’s different.” Back then, the claim was that since the Internet would be growing for decades, dot-com stocks could go to the moon and beyond.

The claim the the Internet would continue growing was sound, but the prediction that this growth would drive stock valuations into a never-ending bubble was unsound.

Once again we hear reasonable-sounding claims being used to support predictions of a never-ending rise in stock valuations. Some observers find this “interesting.”

2. Similarity in 2000/2021 stock charts. Technical analyst Sven Henrich posted charts of Cisco Systems in early 2000 and Tesla in early 2021: Clear and Present Danger. The similarity is, well, “interesting.”

3. Similarity in 2000/2021 NASDAQ volume spikes. Technical analyst Tom McClellan posted a chart of NASDAQ volume in a ratio with New York Stock Exchange (NYSE) volume. Extreme Point for Nasdaq Volume. Notice the recent spike into dot-com era territory. Hmm, “interesting.”

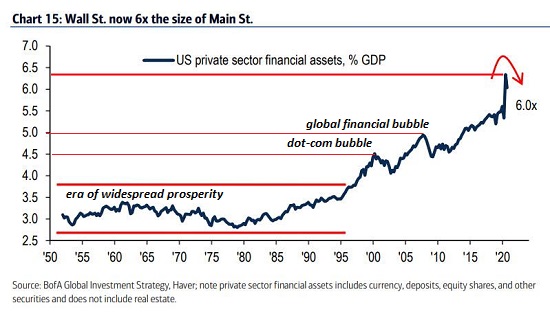

4. Financial assets as a percentage of Gross Domestic Product (GDP) hit an all-time extreme. Note that in the “Glorious Thirty” postwar years (1946-1975) of broad-based prosperity, financial assets were around three times GDP. Now financial assets are over six time the GDP.

This ratio increased with every one of the three bubbles since the mid-1990s: the dot-com bubble in 1999-2000, the Global Financial Meltdown in 2008-09 and now the bubble of 2020-21. That financial assets are now six times the size of the “real economy” (GDP) is an “interesting” data point

5. Despite assurances that “this time it’s different,” all speculative bubbles pop because they are based in human emotions. We attempt to rationalize the bubble by invoking the real world, but bubbles are manifestations of human emotions and the feedback of being in a herd of social animals. I’m not sure if this even qualifies as “interesting” or not; perhaps it’s too “obvious” to be “interesting.”

Is that a red flashing light on the control panel of the man behind the curtain? Probably nothing, pay no attention….