” So far in fourth quarter reporting season, with 11 percent of the results reported for the S&P 500, three-quarters of companies have actually surprised Wall Street’s forecasters. Earnings are shaping up to be better than people expected.” – CNBC

While it is a correct statement, it is also shows the problem with the “earnings silly season.”

As I noted in this past weekend’s Real Investment Report:

“With earnings season underway, there is support in the short-term for asset prices but remember that earnings are only beating sharply downgraded estimates. (This is the equivalent of companies scoring a 71 after the level for an “A” was reduced from 90 to 70)”

In other words, while the media is pounding the table screaming “buy, buy, buy,” investors should take a step back and remember that investing is ultimately a function of “actual” earnings, revenues, and cash flow. Or, as Warren Buffett once quipped:

“Price is what you pay. Value is what you get.”

To explain the issue, which ultimately becomes a major problem for investors, we have to jump into a DeLorean for a quick trip back to January 1, 2018.

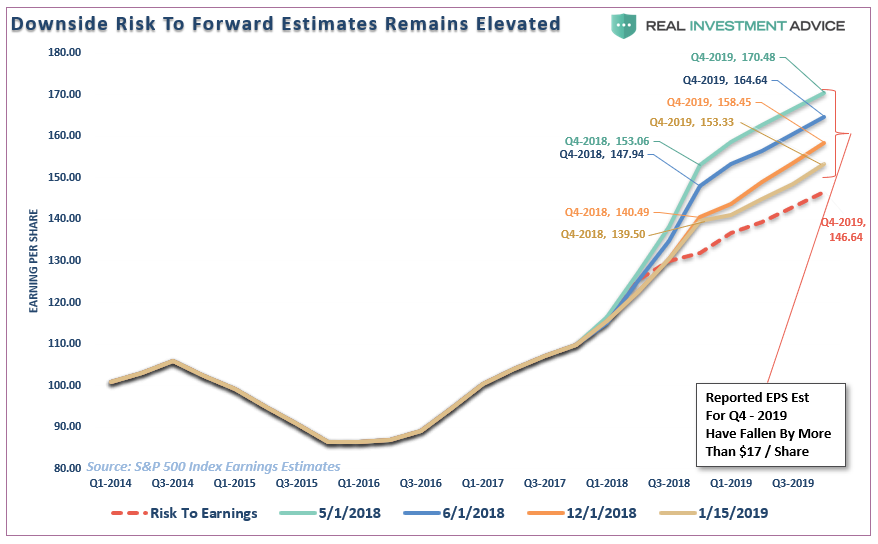

At that point, Wall Street analysts were predicting earnings were going to rise to $156.75 per share by the end of 2019. With the S&P 500 trading at 2695.81 forward P/E’s were a “bargain” at just 17.19x earnings.

However, by May, analysts were chasing each other to be the highest estimate on Wall Street (bullish headlines get clicks) and pushed the 2019 number to a whopping 170.48 per share. With the market at 2734.62 at the end of May, it was time to “buy, buy, buy” as the market was “cheap, cheap, cheap” at just 16x earnings.

The only problem is that if you bought the market in June of 2018 based on its “cheapness,” it was a poor decision as forward earnings estimates turned out to be grossly wrong.

Over the last couple of years I have repeatedly produced the following chart which shows the problem with forward estimates. In just the last month, Wall Street earnings estimates fell by more than $3 per share pushing the total decline to more than $17 per share from the peak.

The red-dashed line is from an early 2018 where I discussed the fallacy of “tax cuts.” In reality estimates must eventually reflect real, organic, economic growth. Tax policy changes do not boost revenue growth at the top line.

Not surprisingly, such has been exactly the case, and despite a 20% correction from the peak of the market last year, consequently at a time when investors were told to “buy, buy, buy” because profits were exploding, investors are paying more today for each dollar in earnings today than they were in June, 2018.

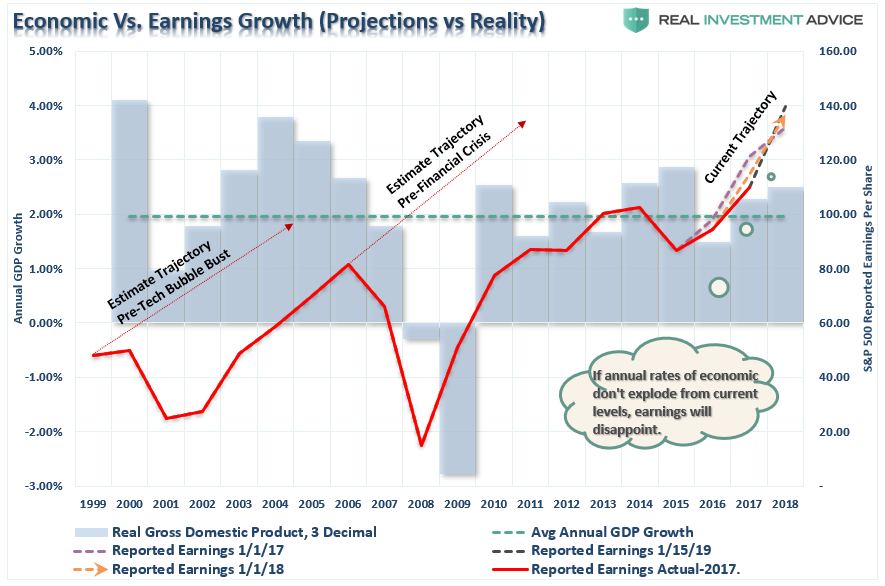

To get a better sense of just how much those forecasts have been downwardly revised, the chart below compares where estimates were at the beginning of 2018 for the end of 2019.

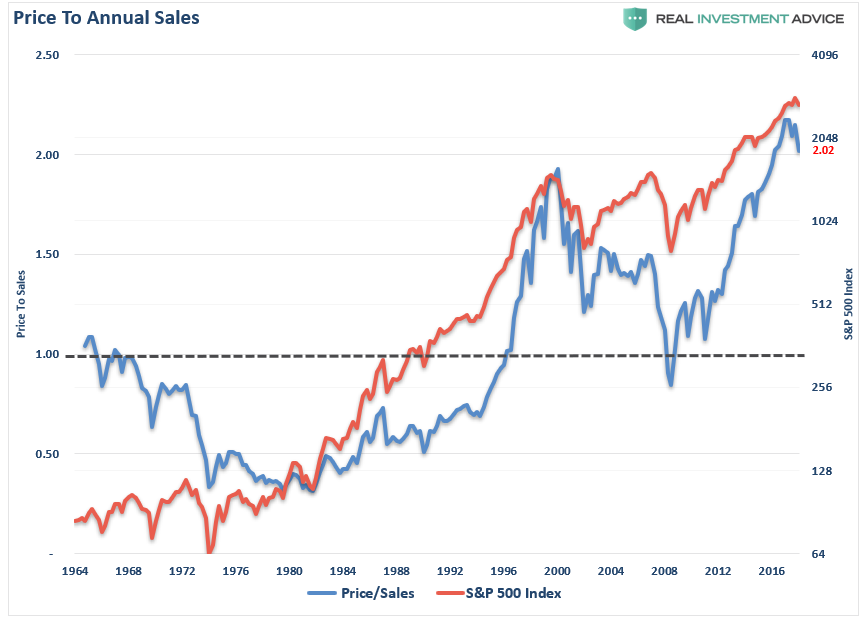

In other words, equities have gotten MORE expensive over the last 6-months rather than less. However, given that bottom line earnings per share is grossly manipulated through share repurchases, accounting gimmicks, and outright “fudging,” more on this in a moment, top-line revenue gives us a much more accurate picture of the excessive prices being paid for stock ownership. Currently, investors are paying 2x sales which exceeds the peak paid in 2000.

However, investors quickly dismiss fundamental realities for the promise of future riches. Of course, this is the “modus operandi” of Wall Street to bring gamblers into the casino. As I discussed in “The Problem With Wall Street Forecasts,:”

“The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the possibilities for unexpected, random events. In a 2010 study, by the McKinsey Group, they found that analysts have been persistently overly optimistic for 25 years. During the 25-year time frame, Wall Street analysts pegged earnings growth at 10-12% a year when in reality earnings grew at 6% which, as we have discussed in the past, is the growth rate of the economy.

This is why using forward earnings estimates as a valuation metric is so incredibly flawed – as the estimates are always overly optimistic roughly 33% on average.”

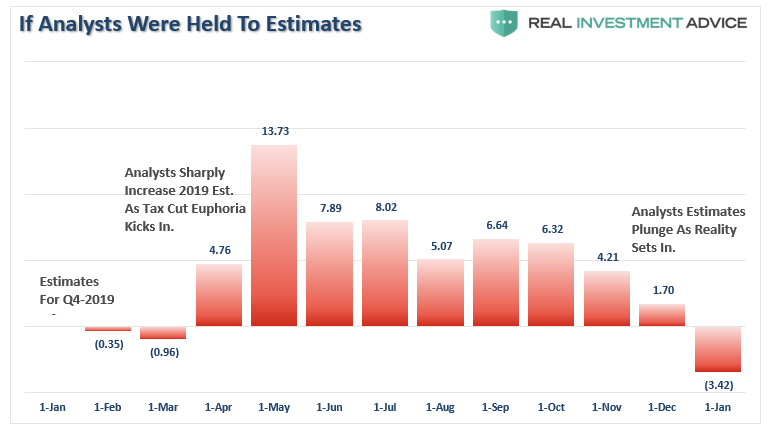

Yet, even while this data is readily apparent, Wall Street analysts continue to same game of starting with wildly exuberant estimates and then lowering estimates until companies can beat them.

Since investors don’t hold analysts accountable, it is a game which is played out each quarter so that Wall Street can sell their wares. The reality is that if analysts were held to their original estimates, instead of 70-80% of companies beating estimates every quarter, it would be exactly the opposite.

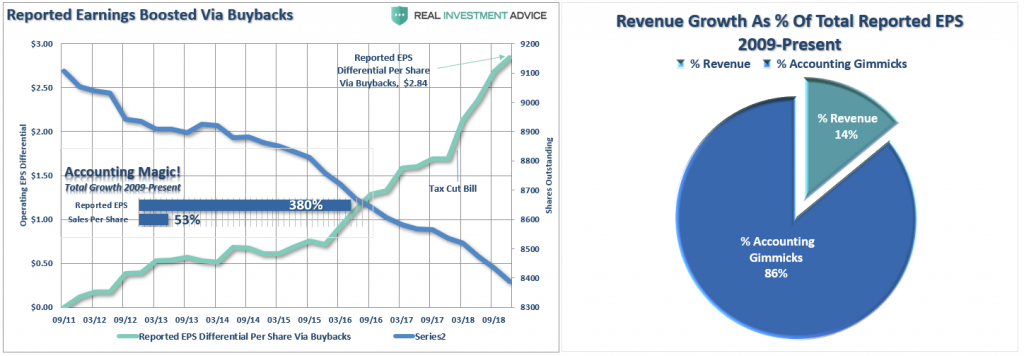

As noted above, the biggest drivers to bottom line earnings has been accounting gimmicks, share repurchases, and tax cuts. Revenue growth, as a percentage of the total, has shrunk to just 14% even though reported earnings per share surged by almost $3/share from repurchases.

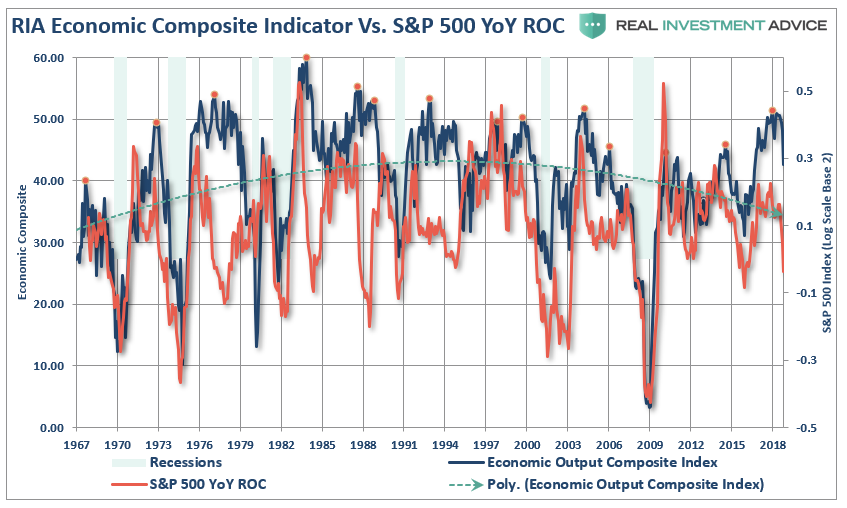

However, even with the recent decline of forward estimates, they still remain far too lofty for 2019. Economic growth is slowing and, as I penned just recently (see article for composite index makeup), the domestic economy has already shown early signs of a more significant slowdown. Given that corporate profits are a function of economic activity, it should not be surprising that the rate of change of the S&P 500 is closely tied to annual changes in the Economic Output Composite Index.

The “sugar high” of economic growth seen in the first two quarters of 2018 was from a massive surge in deficit spending and the rush by companies to stockpile goods ahead of tariffs. While those activities create the “illusion”of growth by pulling forward “future” consumption, it isn’t sustainable and profit margins will follow suit very quickly.

The point here is simple, before falling victim to the “buy the market because it’s cheap based on forward estimates” line, make sure you understand the “what” you are actually paying for.

Wall Street analysts are always exuberant hoping for a continued surge in earnings in the months ahead. But such has always been the case.

Currently, there are few, if any, Wall Street analysts expecting a recession at any point in the future. Unfortunately, it is just a function of time until the recession occurs and earnings fall in tandem.

Wall Street is notorious for missing the major turning points of the markets and leaving investors scrambling for the exits.

2018 should have been a wake-up call. 2019 could well be the problem.