via Zerohedge:

A common refrain among the bullish talking heads on CNBC in recent months has been that whether one includes the Fed’s invisible hand in “price discovery”, or excludes it as so many naively continue to do, the result would be the same as stock fundamentals are still very strong. But is that really the case or are they just talking their book?

According to a new report from Goldman strategist Christian Mueller-Glissman, the answer is the latter.

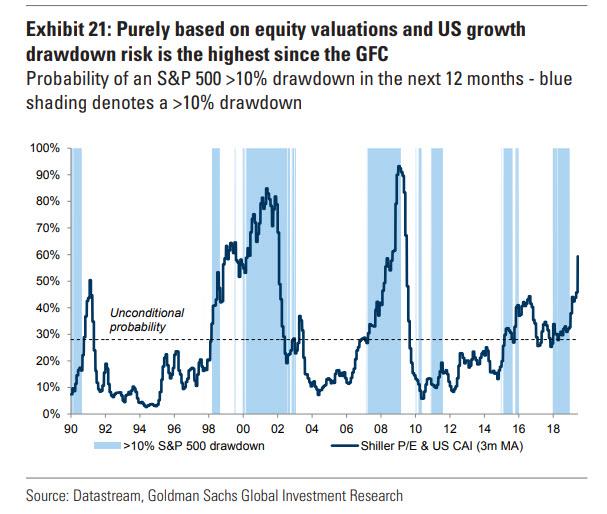

As the Goldman analyst writes, “valuations of risky assets have increased materially YTD” just in case anyone has failed to notice. This, contrary to what one may hear on CNBC is very troubling, because as the Goldman report notes, “purely based on elevated equity valuations, as measured by the S&P 500 Shiller P/E, and current growth, according to our US Current Activity Indicator (CAI), the risk of an equity drawdown of more than 10%”, i.e. a sharp market drop, or for lack of a better word, crash, “is the highest since the GFC.”

Indeed, as shown in the chart below, the risk of a market crash in the next 12 months is now well above 50% (it is approaching 60%), and the highest level since the global financial crisis, when it hit 90%.

Why is the market ignoring this rising risk of growing corporate imbalances and buying stocks at any opportunity? Because as Goldman concedes “after a small drawdown in May, central banks have helped buffer volatility in June.”

Even so, the strategist warns that “to stabilise risk appetite on a sustained basis and anchor volatility, better global growth is needed. Until then, markets remain vulnerable to monetary policy disappointments and political risks. And another buyback blackout period has started this week, which reduces a key demand for equities.”

And speaking of rising risks, Goldman looks ahead and cautions that 3Q – which will begin in just 4 days – brings several uncertainties besides the US/China trade tensions with pending key EU appointments, the new ECB president, potential for more tensions in Italy budget negotiations into September and the Excessive Deficit Procedure (EDP) by the EU, rising tensions in the Middle East (Iran, Turkey), the upcoming OPEC+ meeting end of June and US Tech regulation. Also US budget discussions comments on October 1 and could again result in a government shutdown. And of course there are rising risks around Brexit – European implied volatility, as measured by the V2X future, is starting the price excess volatility for the October 31 deadline.

In short, the wall of worry is about to get a whole lot higher – how much longer can algos keep climing it?