by jessefelder

“Never, ever invest in the present. It doesn’t matter what a company’s earning, what they have earned… You have to visualize the situation 18 months from now, and whatever that is, that’s where the price will be, not where it is today… If you invest in the present, you’re going to get runover.” -Stan Druckenmiller

I love this quote because it really dilineates the difference between a very successful professional investor, in this case arguably the most successful of all time, and the average investor. The former is constantly trying to analyze trends and how they might play out over the coming months. The latter is looking backward at the past 18 months and extrapolating that out into the future. This is why the average investor is caught completely off guard by a major trend change and continues to mash the accelerator even as he runs headlong into a mack truck while the successful investor anticipates the truck, calmly applies the brakes and moves aside in time to avoid a fatal collision. This quote seems especially relevant today because there are so many signs pointing to the fact that the markets and economy 18 months from now could look vastly different than they have over the past 18 months. So let’s try to spend some time visualizing certain trends in the markets and how they might play out.

The most obvious and most important of these is the current backlash against shareholder-first capitalism. This is manifest in all sorts of ways at present most notably in the antagonistic attitude towards stock buybacks. Both Democrats and Republicans are now fighting over who will get to take credit for reining them in. A couple of weeks ago it was Democrats Bernie Sanders and Chuck Schumer who were railing against buybacks claiming they contributed to wealth inequality and long-term economic harm. Last week it was Republican Marco Rubio who proposed, rather than putting any prohibitions on the activity, simply taxing buybacks the same way dividends are taxes so that there is no longer an incentive to pursue one over the other. Rubio seems to hope that this would encourage companies to reinvest cash flows rather than pay them out. He even went so far as to tweet, “Right now [we] don’t have a “free market”. We have tax code which engineers economy in favor of inflating prices of shares at the expense of future productivity & job creation. If we are going to use tax code to incentivize behavior, it should be investing in productivity & jobs.”

'Tax policy changes to end this preference might, on their own, increase investment by shifting shareholder appetite for capital return.' https://t.co/VREJi4Ml0a

— Jesse Felder (@jessefelder) February 12, 2019

This bipartisan support for reining in stock buybacks can really be considered bipartisan support for ending or at least reshaping shareholder-first capitalism and replacing it with a stakeholder-first approach that benefits employees and customers as much as anyone else. This is critical to understand because, to the extent companies have been able to suppress labor and even customers through greater corporate concentration and greater influence in Washington, their profit margins have benefited. Now that the pendulum appears to be swinging back in the other direction, profit margins are at risk of reverting to historical norms. As discussed last week, this has massive implications for both earnings and valuations.

There are plenty of real issues facing modern capitalism that investors should be watching closely. One obvious area for discussion: The shift of the tax burden away from capital and on to labor since the pendulum began to swing back under Ronald Reagan. https://t.co/YN8cZu5R0d

— Jesse Felder (@jessefelder) February 11, 2019

There are also growing signs that the pendulum is already swinging back in the direction of labor. Last year saw the greatest number of strikes and walkouts since 1986.

Some 485,000 U.S. workers were involved in 20 major strikes and lockouts last year, the largest number since 1986. https://t.co/keZp61ifmc pic.twitter.com/CfkvMvVzsi

— Jesse Felder (@jessefelder) February 12, 2019

This would only be possible in an environment that gave workers reason to have the confidence to walk out like this. The ultra-low unemployment rate is one reason they have more bargaining power today but the retiring of the baby boomers creates a demographic tailwind to labor powers that hasn’t been seen in decades.

https://twitter.com/NorthmanTrader/status/1095720820431835137

Even more important is the growing trend toward deglobalization. These two factors, demographics and deglobalization, represent a reversal of the growing labor supply that was responsible for labor losing so much power over the past several decades.

Deglobalisation is a complex, slow-burn process and not yet a done deal. But already, companies are under increasing pressure to choose whether they want to do business in the US, or in China, particularly in highly contentious areas like 5G networks. https://t.co/patHDIkrew

— Jesse Felder (@jessefelder) February 11, 2019

If, indeed, demographics, social and political trends are all working to push the pendulum back in favor of labor over capital then its hard to imagine this will not have a major effect on corporate profit margins. As Warren Buffett wrote 20 years ago,

In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems—and in my view a major reslicing of the pie just isn’t going to happen.

Clearly, Buffett was wrong and there was a major reslicing of the pie over the past couple of decades. He was right, however, in anticipating the political problems that would inevitably rise out of such and outcome and these are precisely what we are witnessing right now.

Paul Tudor Jones: 'I think we've got a mania going on in buybacks and a mania going on in terms of shareholder primacy. I'm really nervous about what the ultimate social consequences are in this country.' https://t.co/Tb4DOHTUoK

— Jesse Felder (@jessefelder) February 12, 2019

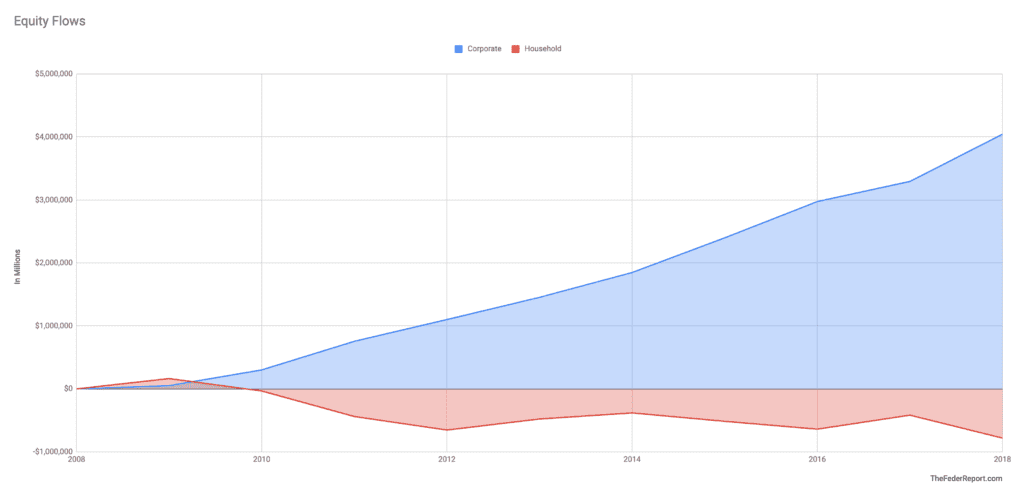

It’s not hard to imagine, given the current sentiment and trends in this regard, that we see legislation like Rubio’s or something similar actually go into effect. This obviously represents a major headwind for the stock market as it would severely restrict its single greatest source of demand over the past decade. Without buybacks, or without the same level of demand from corporations, can stocks continue to weather the demographic headwinds of an aging population persistently reducing equity exposure by neccesity? I would guess not. The chart below plots total stock buybacks versus household equity flows from 2009 to 2018.

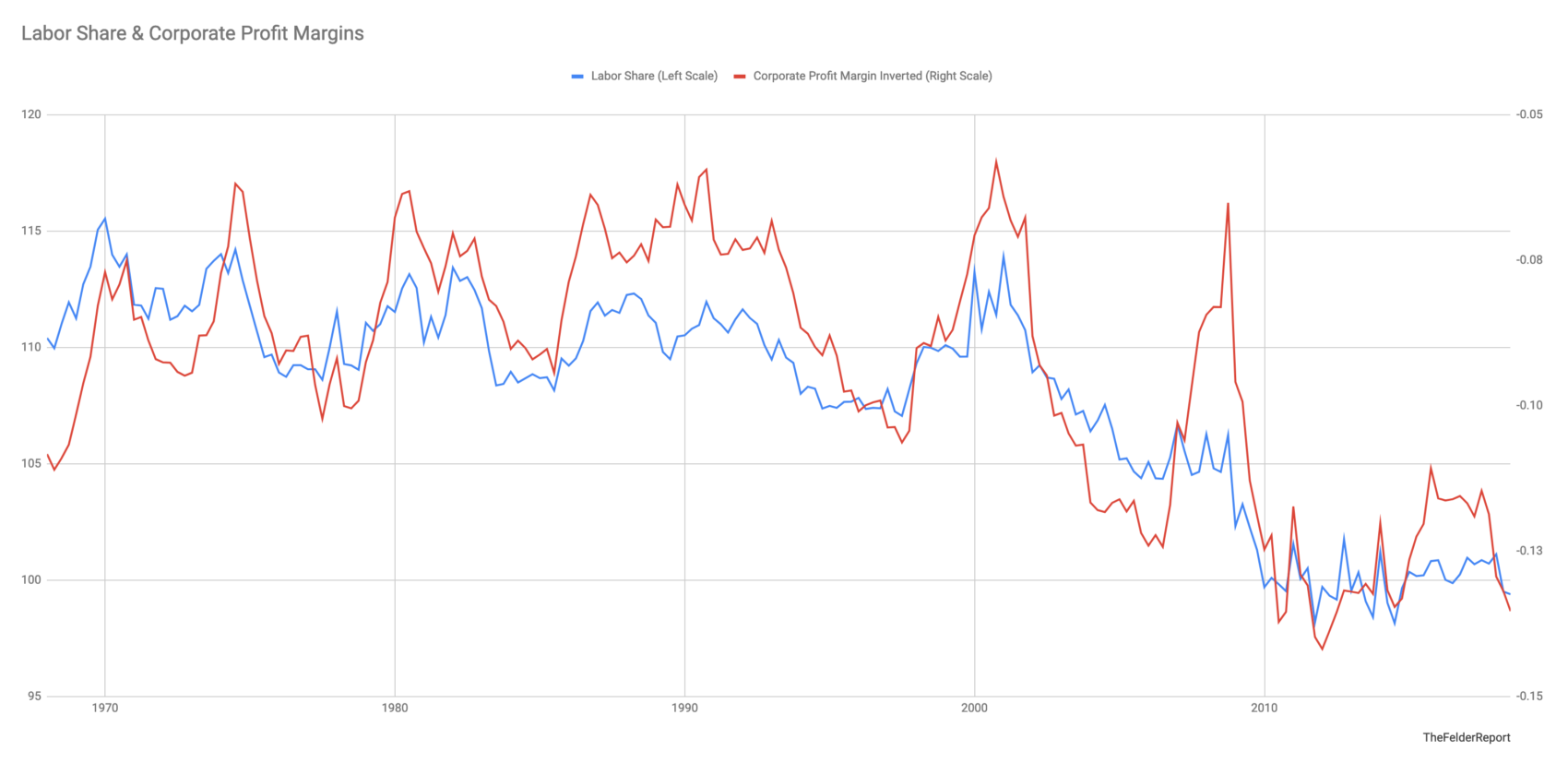

More importantly, over the long run a shift from a shareholder-centric mentality to a stakeholder one is probably a very good thing for both the economy and for the equity market but in the short run it will put immense pressure on corporate America’s bottom line. Just think of how the markets have been propped up by an acceleration of the shareholder first mentality in recent years and it’s not difficult to see how the reversal of that could lead to a painful unwind. The chart below plots labor share of national income along with corporate profit margins (inverted). Notice how highly correlated these are. It should be obvious to anyone who looks at this chart that rising corporate profit margins have come entirely at the expense of labor.

More importantly, over the long run a shift from a shareholder-centric mentality to a stakeholder one is probably a very good thing for both the economy and for the equity market but in the short run it will put immense pressure on corporate America’s bottom line. Just think of how the markets have been propped up by an acceleration of the shareholder first mentality in recent years and it’s not difficult to see how the reversal of that could lead to a painful unwind. The chart below plots labor share of national income along with corporate profit margins (inverted). Notice how highly correlated these are. It should be obvious to anyone who looks at this chart that rising corporate profit margins have come entirely at the expense of labor.

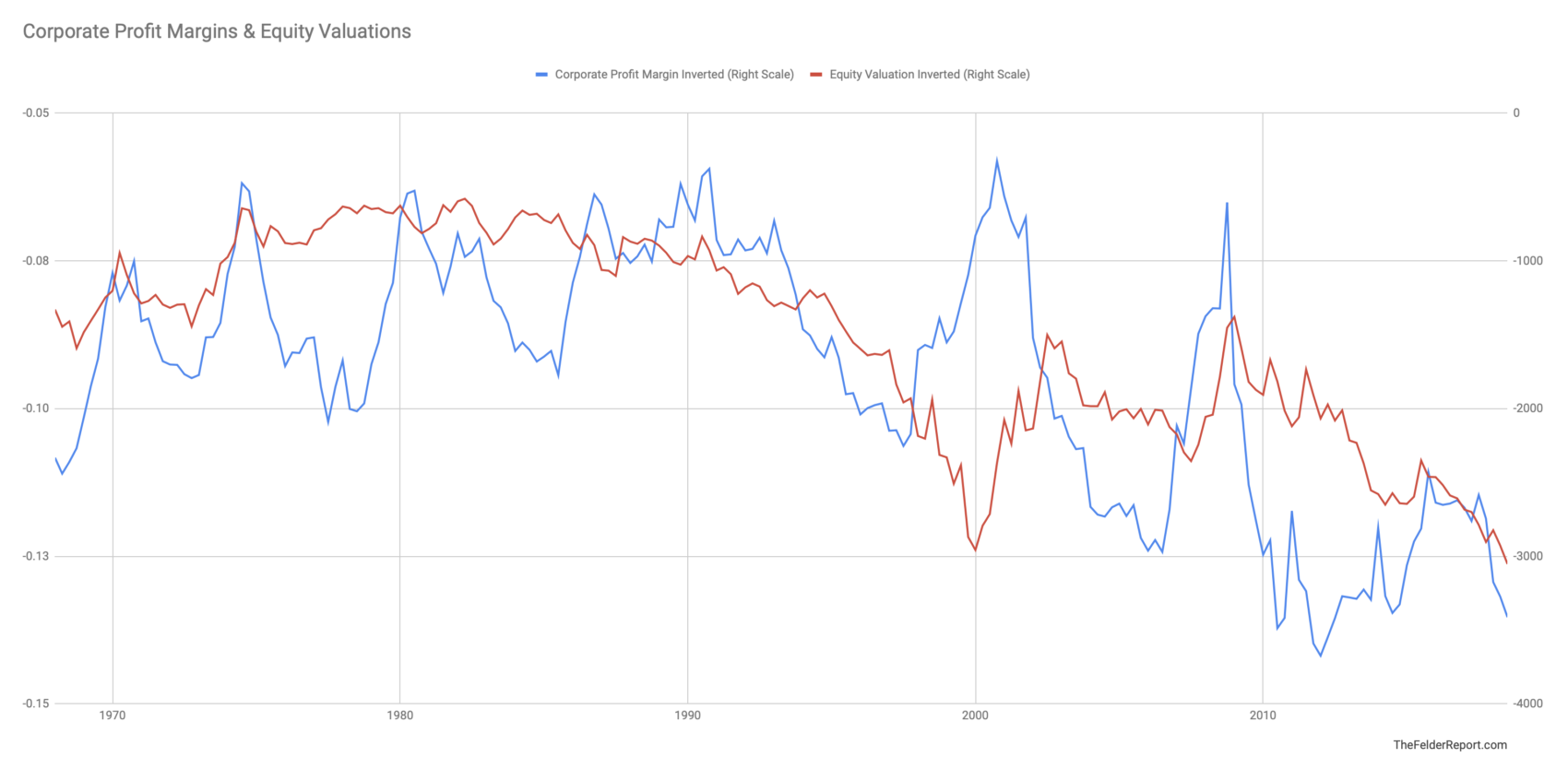

This next chart plots corporate profit margins (inverted) alongside equity valuations (inverted). It should also be clear to anyone who looks at this that the unprecedented equity valuations the market carries today are, to a great extent, a result of record profit margins (which allow for even more stock buybacks).

Put these three charts together and it becomes clear that the greatest equity bubble in history has been driven entirely by a shareholder first mentality that has exploited labor to benefit shareholders like we have never seen before anywhere in the world and buybacks have played a massive role. As Edward Chancellor noted last week, as a result of all of this our stock market is is more highly valued today than the Mississippi Company was at its peak.

As central bankers struggle to reverse their post-crisis monetary measures, the lessons imparted by the Mississippi Bubble are more relevant than ever. https://t.co/hwymsCCtjj ht @htsfhickey

— Jesse Felder (@jessefelder) February 14, 2019

What we are seeing today, both politically and socially, is a direct backlash against this explicit favoring of shareholders at the expense of labor. Over the next 18 months, it’s very hard to see how these trends towards a rebalancing of the American pie don’t continue to gather steam. We live in a society now where not only memes go viral but so do politicians and political ideologies. According to Pew Research, young people will make up nearly 40% of the vote by 2020…

Millennials and Gen Z will together make up nearly 40% of the vote by 2020 https://t.co/SEgR7WOI3s pic.twitter.com/bf4AdXF2eA

— Jesse Felder (@jessefelder) February 14, 2019

…and, according to The Economist, the majority of these folks have a favorable view of socialism, mainly as a way to combat the obvious inequities they seen in the world around them.

Some 51% of Americans aged 18-29 have a positive view of socialism. https://t.co/pToNebXnjU pic.twitter.com/iFI5KkESUV

— Jesse Felder (@jessefelder) February 14, 2019

The companies that best represent the exploitation of both labor and customers to the exclusive benefit of shareholders through are none other than the FANG stocks.

Rising Inequality Is Tech’s Fault, After All https://t.co/zks7uh6Jqr pic.twitter.com/9RtH47OcEn

— Jesse Felder (@jessefelder) February 14, 2019

Specifically, Facebook, Google and Amazon should be concerned. Already in Germany, it seems they have declared the business model of abolishing privacy in the name of monetizing data essentially illegal.

'The FCO’s theory is that Facebook’s dominance is what allows it to impose on users contractual terms that require them to allow Facebook to track them all over.' https://t.co/gfSN0B6tLq

— Jesse Felder (@jessefelder) February 11, 2019

The Government Accountability Office here in the U.S. last week argued the Congress should pursue similar legislation.

The Government Accountability Office, which gives nonpartisan advice to Congress, said in a report released Wednesday that "this is an appropriate time for Congress to consider comprehensive internet privacy legislation." https://t.co/V6Q6gSdR4K

— Jesse Felder (@jessefelder) February 13, 2019

And it appears there is plenty of support for a reinvigorated FTC in enforcing the laws these companies, most notably Facebook, have already violated time and time again.

For the FTC, a significant punishment levied against Facebook could represent a new era of scrutiny for Silicon Valley companies after years of privacy missteps. https://t.co/K7JmDDZw7P

— Jesse Felder (@jessefelder) February 15, 2019

At the same time, the mutiny inside Google seems to be growing apace.

Google bears the responsibility of being one of the most influential companies in the world, but it has misused its power to place profits above people. Executives seem to have forgotten the ethos of the company’s earliest employees — “don’t be evil.” https://t.co/RMnXcLJtOF

— Jesse Felder (@jessefelder) February 14, 2019

And, as the backlash against Amazon shows, people are more closely associating big tech directly with wealth inequality.

These cities are the spatial embodiment of the rocketing inequality of the past several decades, which shows that it’s quite easy to grow a city, or a nation, or a global economy while only the very, very, very rich eat up all that income growth. https://t.co/ttft0eQ2jS

— Jesse Felder (@jessefelder) February 15, 2019

In this way, the shift in power back in favor of customers and employees may be more threatening to big tech than to any other sector or group. And it appears they are already feeling a great deal of pressure.

The switch to less detailed disclosure invariably occurs just when the established metric starts to sour. The change allows companies to bury the bad news. https://t.co/YRQvVMFnLt

— Jesse Felder (@jessefelder) February 12, 2019

In addition to the growing trends of restoring privacy rights and overhauling the antitrust framework, another trend that appears to favor labor over capital is the growing talk of a federal jobs guarantee as a part of a Green New Deal. If companies were forced to compete for employees with the Federal Government paying a $15 minimum wage it could possibly represent an inflationary catalyst like we haven’t seen in a very long time, especially if it were to come while the unemployment rate is already so low.

In the Green New Deal, trillion-dollar price tags are a feature, not a bug. That is because its mission is to create “millions of good, high-wage jobs” in “front-line and vulnerable communities.” The higher the price tag, the more jobs it creates. https://t.co/GBJeOWwI63

— Jesse Felder (@jessefelder) February 14, 2019

Proponents of the New Green Deal acknowledge that it would be incredibly expensive. I have seen estimates that suggest the cost, including the jobs guarantee, could be as much as $3 trillion per year. Supporters of the plan also freely admit there’s no way to raise enough revenue to pay for it; instead, they suggest simply allowing the federal deficit to grow by the amount necessary to fund the programs.

The austerity argument has lost ground as both economists and politicians embrace budget deficits and rising debt loads. https://t.co/JnByuzPU8A pic.twitter.com/HxeLiu7mfH

— Jesse Felder (@jessefelder) February 13, 2019

With the deficit already expected to top $1 trillion this year, quadrupling that number would take it from roughly 5% of GDP to as much as 20%.

The U.S. budget deficit totaled $318.9 billion in the first quarter of the 2019 fiscal year, a 41.8% increase from the same period last year, according to data released by the Treasury Department. https://t.co/MdJpNV306U

— Jesse Felder (@jessefelder) February 14, 2019

Certainly, this would represent a significant test of the underlying thesis behind MMT. With the Treasury already tasked with finding buyers for a record amount of issuance this would only put even greater pressure on the institution.

'America will need to sell an eye-popping $12tn of bonds in the coming decade. It will require about a 6% shift in global asset allocations to absorb the debt. What if investors don’t want to make that shift?' https://t.co/NhuSZfTetl

— Jesse Felder (@jessefelder) February 8, 2019

Still, MTT proponents argue, the Fed can always act as buyer of last resort, meaning the Federal Government has the ability to task Jay Powell & Co. with keeping interest rates low by any means necessary. This sort of fiscal dominance would be entirely unprecedented in our country and thus would represent a massive risk to the dollar and to its station as global reserve currency. This might be why global central banks have been selling dollars for gold to the greatest degree in half a century.

Over the past year, central banks emerged as big buyers of gold, with purchases up almost 75%. They acquired $27bn worth of bullion — the most in almost half a century.https://t.co/x99vnCo6Cx

— Jesse Felder (@jessefelder) February 12, 2019

Certainly, the gold price seems to be sniffing out these risks to the dollar. While the bottoming process has felt very long and drawn out over the past few years it is hard to deny that’s exactly what it is. And as soon as these risks to the dollar are deemed clear and present dangers the gold price will have already soared.

"I have long postulated that someday the PBOC or the BOJ would come for gold in a big way, and that when that happened, gold wouldn’t be moving by $50s or $100s, but instead would explode higher by $500s or $1,000s." –@kevinmuir https://t.co/0ro8pBlTov pic.twitter.com/9nW4yKKKwZ

— Jesse Felder (@jessefelder) February 15, 2019

Putting all of these things together, it seems the risk to the equity markets may be as high as it has ever been and will only be growing over the coming 18 months as these nascent trends gather momentum. Should the attack on buybacks succeed it would mean the stock market would lose its most significant source of demand. Just as threatening to share prices, however, would be a growing labor share of profits as a result of social, political and demographic trends. At the same time, pressure on the Fed to allow a reckoning for shareholders rather than make good on the Fed put could easily arise out of these sentiments, as well, especially if the Jay Powell and his cohorts are tasked with monetizing the debt in order to support the working man rather than focusing entirely on supporting financial assets.

Unfortunately, an inexorably growing financial system, combined with an increasingly toxic political environment, means that the next major financial crisis may come sooner than you think. https://t.co/XEfJ7yYLHi

— Jesse Felder (@jessefelder) February 11, 2019

With the rise of passive investing the number of investors looking forward and anticipating these potential risks may be lower than ever before. The market, by way of providing above-average returns with below-average volatility in recent years, has strongly conditioned them to believe their rear-window methodology is not only superior to any other but the only way to drive. However, if only several of these trends grow and manifest into public policy there’s a Mack truck heading for this market. And those with the wherewithal to see it coming ought to do their best to move to the sideline and let it pass by.