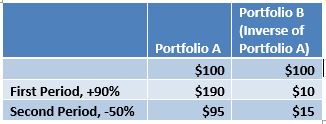

Imagine two portfolios, A and B, worth $100 each. In the first time period, portfolio A gains 90% and Portfolio B loses 90%. So A is worth $190 and B is worth $10. Then, in the second period, Portfolio A loses 50% and Portfolio B gains 50%. So at the end of the second period, Portfolio A is worth $95 and Portfolio B is worth $15.

You now understand why ETFs that deliver the inverse daily return of an index don’t always work, and sometimes deliver radically unexpected returns. After the second period Portfolio A has lost 5% cumulatively; it has gone from an initial value of $100 to $95. But Portfolio B is far from being up 5% cumulatively, despite having delivered the inverse of Portfolio A for two periods. Instead Portfolio B is down 85% cumulatively.

Something like this is what happened to ETFs that shorted volatility or the VIX in February. When volatility spiked 90%, ETFs shorting it dropped by a commensurate amount. But when volatility calmed down again, the ETFs couldn’t bounce back. They were finished.

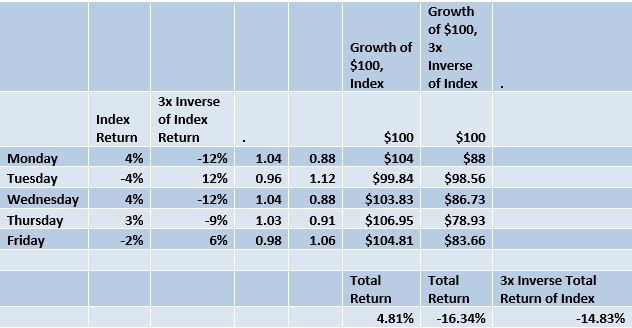

Now the stock market rarely moves more than 10% in one day. So how realistic is what happened to inverse VIX funds with regard to inverse S&P 500 funds? It’s true that there will not likely be that kind of quick meltdown in an inverse S&P 500 Index fund, but it’s also true that investors can be surprised in an inverse fund. And those surprises can be magnified in multiple inverse funds. For example, a 3x inverse fund can produce a return that more than one percentage point away from what you’d expect in just one volatile trading week.

Now, one could say that the difference between the actual return of the inverse fund and what one might have expected isn’t that large in our hypothetical example. However, the discrepancy between the actual result of the inverse fund and what one might expect occurs just after one week. A longer volatile period could create a bigger discrepancy.

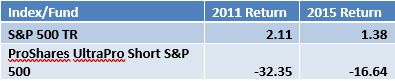

In a real life situation, over a period of time greater than one week, the difference can be large. For example, in 2011, when the S&P 500 Index gained 2.11%, the ProShares UltraPro Short S&P 500 ETF (a 3x inverse fund) lost a whopping 32%, according to Morningstar. Again in 2015, when the index gained 1.38%, the fund dropped more than 16%.

Perhaps stock market inverse funds can be used over short periods of time for trading purposes. But the experiences of 2011 and 2015 with the ProShares 3x inverse fund should deter anyone from using them for an extended period of time.

A better way to short the market would be to short a long ETF like the SPDr S&P 500 ETF (SPY) or to buy put options on this or any other S&P 500 ETF. A put option gives you the right to sell an underlying security at a prearranged price conferring protection on you if the underlying security’s price drops.

Otherwise, holding some extra cash can help combat a volatile, overpriced market. That doesn’t mean selling all your stock holdings if your investment goal is years away, even if you think stocks are overpriced. Moving completely into or out of markets rarely produces a good outcome. It means making adjustments to your allocation to reflect your views. Remember your views can be wrong, or it can take a long time before you’re proven correct. So make your adjustments gently. And, if you need help managing a portfolio, please click this link.

John Coumarianosis an Analyst for Clarity Financial, LLC, and is a contributing editor to the Real Investment Advice Website. He has been an analyst at Morningstar and a writer for MarketWatch and the Wall Street Journal. Follow John on Twitter.