Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

The Fed’s efforts to raise interest rates across the spectrum have borne fruit only in limited fashion. In the Treasury market, yields of longer-dated securities have not risen as sharply (prices fall when yields rise) as they have with Treasuries of shorter maturities.

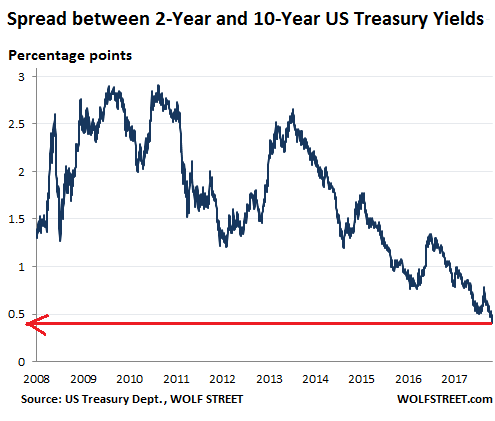

The two-year yield has surged to 2.41% on Tuesday, the highest since July 2008. But the 10-year yield, at 2.82%, while double from two years ago, is only back where it had been in 2014. So the difference (the “spread”) between the two has narrowed to just 0.41 percentage points, the narrowest since before the Financial Crisis:

This disconnect is typical during the earlier stages of the rate-hike cycle because the Fed, through its market operations, targets the federal funds rate. Short-term Treasury yields follow with some will of their own. But the long end doesn’t rise at the same pace, or doesn’t rise at all because there is a lot of demand for these securities at those yields.

Investors are “fighting the Fed”— doing the opposite of what the Fed wants them to do – and the difference between the shorter and longer maturities dwindles, and it dwindles, and it causes a lot of gray hairs, and it dwindles further, until it stops making sense to investors and they open their eyes and get out of the chase, and suddenly long-term yield surge higher, as bond prices drop sharply. That’s why short sellers have taken record positions against the 10-year Treasury recently: they’re waiting for yields to spike to the next level.

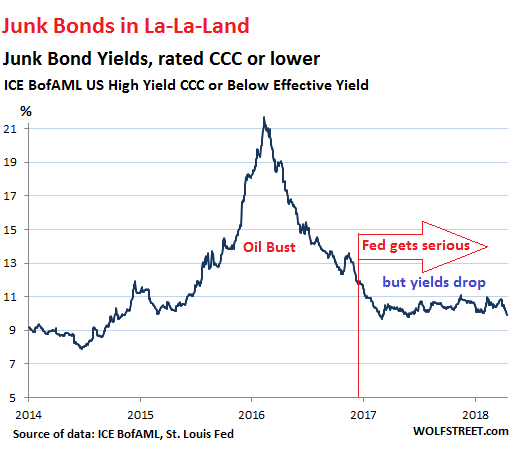

But this disconnect – this symptom of investors fighting the Fed – in the Treasury market is mild compared to the disconnect in the junk bond market. There, investors have completely blown off the Fed. At least in the Treasury market, 10-year yields have risen since the Fed started getting serious about rate increases in December 2016. In the junk bond market, yields have since fallen.

In other words, despite the Fed’s tightening, the junk bond bubble has gotten bigger. And investors are not yet showing any signs of second thoughts.

At the riskiest end, the average yield of junk bonds rated CCC or lower dropped two percentage points since the Fed got serious about tightening, from 11.9% in December 2016 to 9.9% currently (per ICE BofAML US High Yield CCC or Below Effective Yield index):

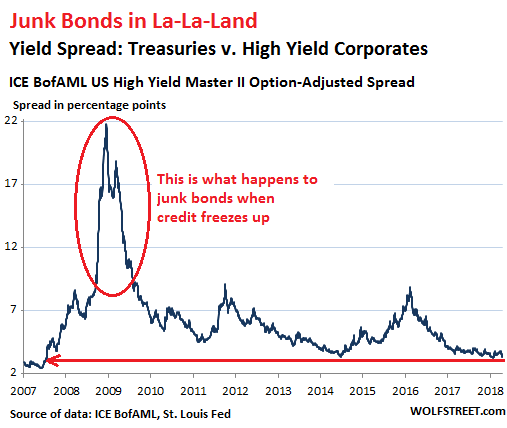

The difference in yield between junk bonds (high risk) and Treasury securities (low risk) is how much investors insist on getting paid for taking more risks. When the spread narrows – hence, when the “risk premium” shrinks – investors are chasing yield and are taking ever larger risks for ever smaller amounts in compensation.

And the spread between the broad junk-bond index and equivalent Treasury yields has narrowed to 3.33 percentage points. Beyond the brief dip on January 26 (to a spread of 3.23 points), it’s the narrowest spread since the la-la days in July 2007 before the Financial Crisis put an end to it (ICE BofAML US High Yield Master II Option-Adjusted Spread via St. Louis Fed):

These days, investors are so eager to chase yield that they’re engaging in huge risks with little extra compensation. This is precisely one of the conditions in the financial markets that the Fed is targeting with its tightening policies. It wants yield spreads to widen. It wants risk premiums to grow. It wants long-term Treasury yields to rise, and it wants junk bond yields of equivalent maturities to rise faster than Treasury yields.

All this means is that the Fed wants bond prices to head south.

Eventually, the Fed wins. And when it does, junk bond yields have a tendency to blow out as the companies that issued those bonds suddenly get caught in a credit squeeze and have trouble servicing that debt. The last two charts above show how far and how suddenly junk bond yields can blow out, as bond prices collapse: during the Financial Crisis and during the oil bust – and that was just an oil bust for crying out loud, and not even a recession.

But not yet. For now, the market is in total denial and happily chasing yield and taking on more risks. And for the Fed, it’s a sign that its tightening job has really just begun.

Short-term interest rates have surged. But are banks paying their depositors these rates? Well, they do offer higher rates, but not to their own clients. Read… Why Aren’t Big Banks Paying Higher Interest Rates on Deposits though Rates Have Surged?