By Wolf Richter for WOLF STREET.

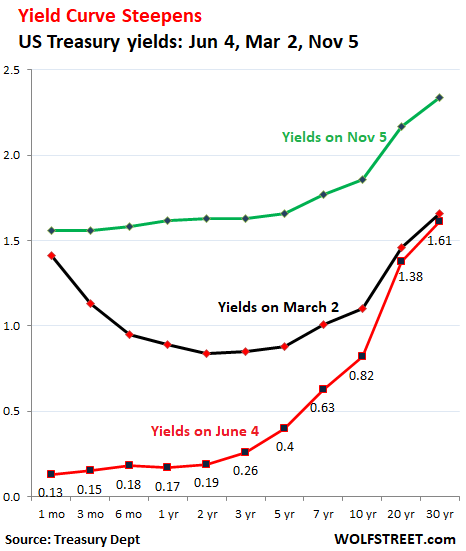

The 30-year Treasury yield has been rising for six days in a row, closing on Thursday at 1.61%, up from 1.41% on May 29, and up from 1.17% on April 20, and the highest since March 19, when the Fed was unleashing its multi-trillion dollar Everything Bubble Bailout.

The 20-year yield closed at 1.38%, the highest since March 4. The 10-year yield closed at 0.82%, the highest since March 26. Obviously, these yields are still in the financial repression torture basement, but the rises are showing some impatience in the market.

The short-term yields are just a hair above zero, with the one-month yield at 0.13%, which makes for a curiously steep yield curve. The red line shows Treasury yields at the close today, from the one-month yield to the 30-year yield. The blue line shows the yields on March 2, before the desperate rate cuts and bailouts. And the green line shows the yields on November 5, 2019:

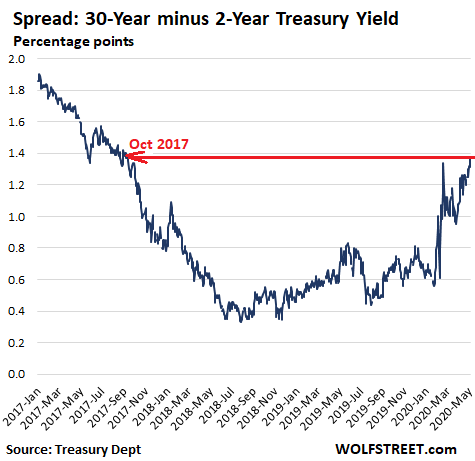

This is the steepest yield curve since October 2017, when measured by the spread between the 2-year yield and the 30-year yield (30-year yield minus 2-year yield), which today widened to 1.37 percentage points, the widest since October 2017:

And this widening of the spread and thereby the steepening of the yield curve has been happening although the Fed has bought $1.6 trillion in Treasury securities since early March, as part of its $2.9 trillion Everything Bubble Bailout.

When a yield curve steepens, it is sometimes associated with the reaction in the market to a strong economy. And that would be a good thing. But this is the worst economy in our lifetimes, and any improvement – there will eventually be some improvement – will just make the economy a little less terrible.

Rather than seeing a strengthening economy, markets might be worrying about inflation, given all this money-printing in combination with trillions of dollars in government stimulus spending, even as the economy is in terrible shape.

Stagflation of the 1970s was a condition where the economy was in decent shape, compared to today’s economy, but just wasn’t growing much, while inflation was ballooning. Today’s economy is an unspeakable fiasco, and a big bout of inflation that would eviscerate the purchasing power of labor – of the lucky ones that still have jobs – would create a phenomenon far worse than stagflation.

The Fed would of course welcome a big bout of consumer-price inflation that will eviscerate the purchasing power of wages.

This inflation would allow it to declare victory over the fake deflation monster. The Fed is not likely to react to inflation, having already hammered home many times that interest rates are going to stay low for a long time. Markets see this too. If consumer-price inflation takes off, under the combined pressure from money-printing and stimulus-spending – while wages cannot keep up because of high unemployment, thus further crushing those that make a living by working – the Fed is going to pat itself on the back.

The economy is currently under a rare combination of simultaneous supply and demand shocks in many aspects as factories and service establishments were shut down, and as companies have slashed capacity, from airlines and container carriers to automakers, creating tight supply in some areas.

But there is also the demand shock, given that tens of millions of people have lost their jobs – but demand for consumer goods is being boosted by enormous stimulus spending. And this combination of supply and demand shocks, along with enormous stimulus spending and money-printing, can produce some peculiar results.

Inflation, at these still super-low long-term yields, would be a serious threat for bondholders as their bonds would lose much of their purchasing power over the term of the bond. And there would be very little yield to compensate them for that loss of purchasing power. The rise in yields, and the steepening of the yield curve might be an expression of a growing distaste for this type of scenario.

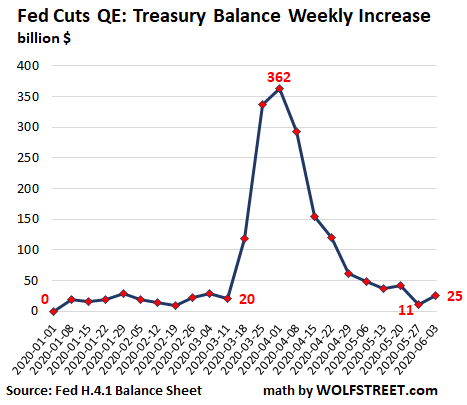

And then there is this: The Fed has been cutting back its purchases of Treasury securities. Its balance of Treasuries increased by $25 billion over the past week, according to its balance sheet today. A week ago, the balance increased by just $11 billion. This is still a lot of money-printing, but it’s way down from $300+ billion in the weeks at the end of March and early April, and it’s right back where it had been before the Fed kicked off its Everything Bubble bailout:

The Fed could still impose “yield curve control” over the market, where it essentially pegs long-term yields via forward guidance and by buying long-term bonds to maintain the peg. This is now being discussed and might happen later this year.

The Bank of Japan has been doing this for years. To dodge this, Japanese banks, pension funds, and other entities have chased yield overseas. This has turned Japanese banks into the most fervent buyers of Collateralized Loan Obligations (CLOs), backed by junk-rated leveraged loans issued by overleveraged US companies that are now toppling. Yield curve control has insidious side effects.

And in an inflationary scenario, yield curve control would make Treasuries as unappealing for long-term bondholders as a toxic-waste dump.