Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

Residential Construction Skids, Nonresidential Construction Stagnates. The delay gave markets a break from lousy data.

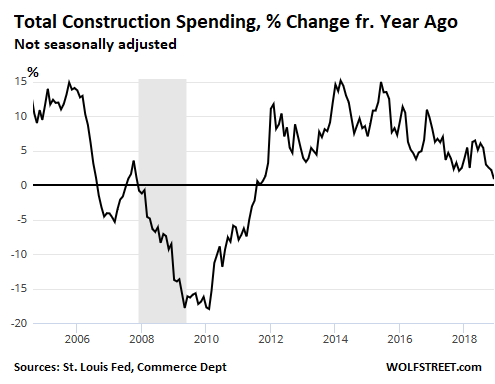

OK, it looks like GDP growth, released last week for the fourth quarter (+2.6% annualized rate), will be revised lower on March 28, given today’s data on construction spending for December, which had been delayed due to the government shutdown.

Construction spending fell 0.6% in December from November, based on a seasonally adjusted annual rate, released today by the Commerce Department. Compared to December a year earlier, total construction spending inched up only 0.8% (not seasonally adjusted), the lowest growth rate since Oct 2011, coming out of the great recession. For the whole year of 2018, construction spending rose 4.1% (not seasonally adjusted), showing that the downturn came late in the year:

Construction spending peaked in 2005, then declined through the Great Recession and into early 2010, followed by a catch-up building boom with year-over-year growth rates of over 20% for brief periods and over 10% for most of the time between mid-2012 and late 2015.

Construction spending, at nearly $1.3 trillion in 2018, accounted for over 6% of the US economy. It can’t be offshored and has a large secondary impact on the economy, from companies buying construction equipment to workers buying new vehicles and sandwiches. It matters to the US economy.

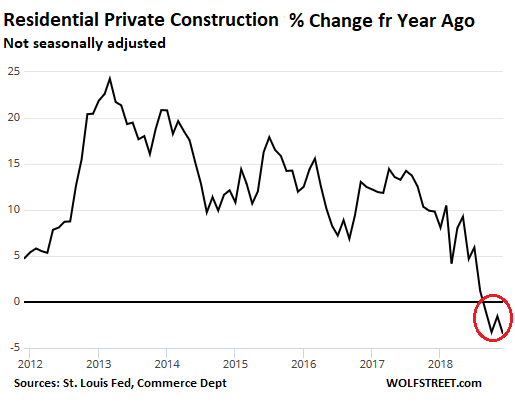

Private residential construction was the problem. Spending on single-family houses, multi-family apartment buildings, etc., but not public residential construction, fell 3.5% in December compared to December 2017 (not seasonally adjusted), the fourth month in a row of year-over-year declines:

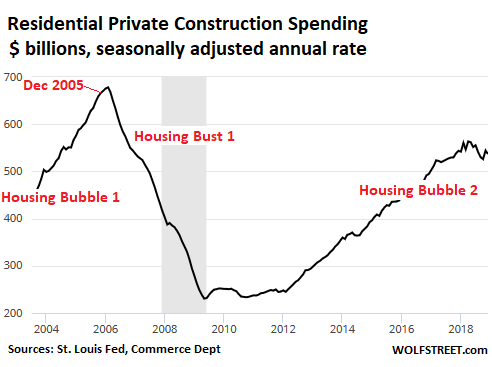

In terms of dollars, private residential construction is forming a peculiar pattern: An epic construction boom during Housing Bubble 1, an epic construction bust during Housing Bust 1, and a construction boom during Housing Bubble 2 that is now losing its grip. In December, private residential construction spending, at $537 billion seasonally adjusted annual rate, while down from December a year earlier, was more than double the range during the 3-year span between 2009 and 2012, but remains below the crazy peak in 2005 (December 2005 $671 billion):

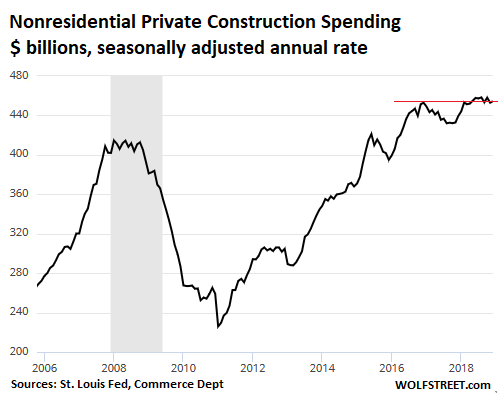

Private non-residential construction – office buildings, warehouses, hospitals, manufacturing facilities, etc., but not including projects for oil-and-gas drilling – rose 3.8% compared to December 2017. But December 2017 is an easy comparison: that month, spending had dropped 3.5% year over year. Compared to December 2016, spending in December 2018 was about flat, stagnating at $454 billion seasonally adjusted annual rate:

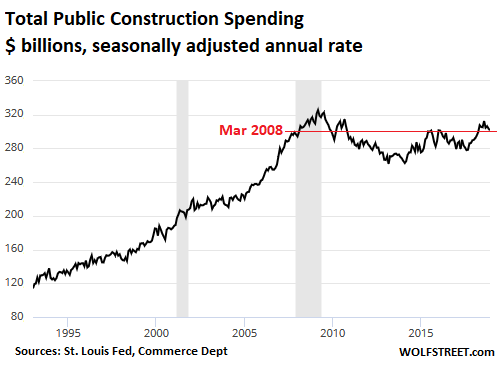

Public construction spending – including on the infamous US infrastructure such as highways and water-and-sewer systems – rose 4.2% year-over-year in December (not seasonally adjusted). But in dollar terms, it has not gone anywhere in 20 years, after peaking in March 2009. December’s spending at $301 billion seasonally adjusted annual rate was back where it had first been in March 2008:

This report on December construction spending was another in a series of reports for late last year that had been delayed due to the government shutdown, and that showed, when they were finally released, an economy whose growth was slowing toward the end of the year, with some actual year-over-year declines cropping up, such as in residential construction.

For the markets, the government shutdown, and the accompanying blackout of economic data, was precisely what was needed the most to sustain the blistering rally in January and February. But this data is now trickling out. And it is putting together the uninspiring image of an economy that is growing but at a considerably slower rate than earlier in 2018, and is right back in the range of where it had been in prior years despite the enormous dual stimulus of huge tax cuts and ballooning government spending.