Here Richmond takes offense with the argument that weak growth for much of this cycle has prevented “excesses” from building, and hence an already long cycle can last even longer. As he says “we disagree and see excesses all over the place, driven in part by years of ultra-low rates.” He notes the following specific details:

Credit markets have grown by 116% in this cycle, and leverage is at unprecedented levels for a non-recessionary environment.

Low quality BBB issuance was 44% of total IG supply in 2017, a record as far back as we have data, and B rated or below loan issuance is now two thirds of total loan supply.

LBOs levered over 6x are now a higher percentage of new LBO loans than in 2007. Covenant quality is considerably weaker than pre-crisis, while the debt cushion beneath the average loan is much lower.

Investors have reached for yield in fixed income in this cycle in a massive way. Foreign flows have flooded into the asset class, arguably treating US credit as a rates product, while liquidity needs have risen, with mutual fund/ETF ownership of credit now over 19% vs. 11% pre-crisis.

Excesses are apparent even outside of corporate credit, with underwriting quality deteriorating in auto lending in this cycle, while non-mortgage consumer debt is at a high, and CRE prices are ~25% above prior-cycle peaks.

Stock-buyback activity has been substantial in this cycle, credit valuations have rarely been richer, and consumer confidence has not been this high since 2000.Summarizing, and “cutting through the details” Morgan Stanley says that it has high conviction in the following two points:

Excesses have to be out there, given what central banks have done in this cycle – i.e., rates near or below zero for nearly a decade and round after round of QE globally, and

the excesses are always difficult to spot as markets are rising, and then become obvious after the turn (how did I miss that?). We think this time is no different. To be clear, excesses are not everywhere. For example, credit quality did not deteriorate in places like housing and US financials in this cycle. However, this simply tells us that the problems of the last cycle will not be the same as the problems of the next.As a result, 2018 is when the critical mass of excesses finally spills over, or, to reuse the title, “the levee finally breaks”:

While the excesses may be out there, that has arguably been the case for a while. The difference, we think, is that more cracks are now forming under the surface, which in our view, means a turn is closer than the consensus believes. For example, outside of corporate credit, we have seen signs of weakness and tighter credit conditions in places like commercial real estate. Consumer delinquencies are rising across products (i.e., autos, credit cards, and student loans). And in corporate credit, one sector after the next is exhibiting “idiosyncratic” problems (e.g., Retail, Telecom, and Healthcare to name a few). All of this is consistent with a late-cycle environment where the yield curve is flattening, correlations in markets are dropping, the economy is at (or arguably through) full employment, the Fed is well advanced in its tightening cycle (we think), and equity multiples are expanding.

Full article:

http://www.zerohedge.com/news/2017-11-27/morgan-stanley-turns-apocalyptic-credit-cycle-turn-closer-many-believe

The issue of liquidity is not a small one.

Investors mistakenly assume there is ALWAYS a buyer at the price at which they wish to sell.

This is wrong.

While the answer is “yes,” as there is always a buyer for every seller, the question is always “at what price?”

At some point, that reversion process will take hold. It is at that point where the storms all collide into a massive wave of panic driving selling. It will not be a slow and methodical process, but rather a stampede with little regard to price, valuation or fundamental measures.

It will be the equivalent of striking a match, lighting a stick of dynamite and throwing it into a tanker full of gasoline.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will cause catastrophic spreads between the current bid and ask pricing for ETF’s, junk bonds, and option pricing. As investors are forced to dump positions to meet margin calls, the lack of buyers will form a vacuum causing rapid price declines which leave investors helpless on the sidelines watching years of capital appreciation vanish in moments.

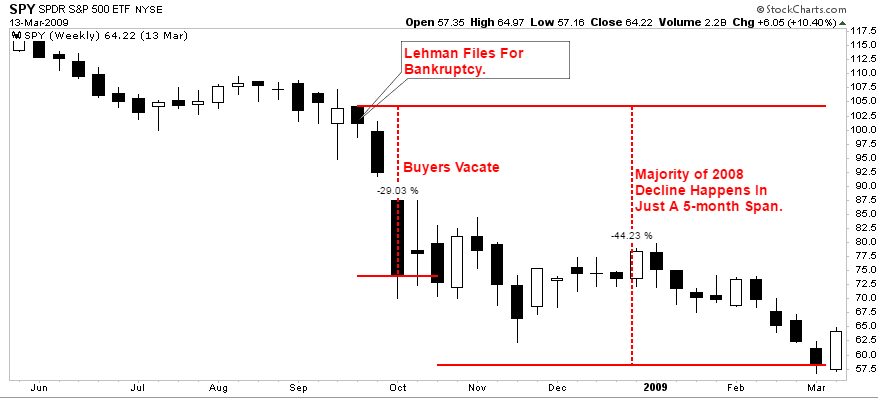

Don’t believe me? It happened in 2008 as the “Lehman Moment” left investors helpless watching the crash.

Over a 3-week span, investors lost 29% of their capital and 44% over the entire 3-month period. This is what happens during a margin liquidation event. It is fast, furious and without remorse.

http://www.zerohedge.com/news/2017-11-27/perfect-storm-coming-market-crisis

Chris Whalen on The Yellen Put

The Yellen Put has increased the debt load in the US and globally, but left the financial markets even more fragile than in 2007. A key measure of this danger was illustrated recently in Grant’s Interest Rate Observer, quoting Asset Allocation Insights, which notes that since 2008 the duration of the Bloomberg Barclays US Aggregate Bond Index has increased 62% to 6.2 years.

Simple translation: Via manipulation of the credit markets, the FOMC has temporarily suppressed growing bond market volatility measured by duration. The Yellen Put means that bond prices will likely move at a brisk pace as and when volatility returns, a pace that will stun complacent investors. But meanwhile, the weight of the Fed’s $4 trillion bond portfolio first is going to result in an inverted yield curve.

As the spread on 2s vs 10s in the US Treasury market relentlessly closes in on zero, the FOMC is grudgingly being forced to admit that open market purchases of securities may not actually impact the CPI or job creation. And remember, as Grant’s notes with understandable pleasure, that the bond market is now dominated by long-dated Treasury paper and corporate debt with minuscule coupons. And there is also a hidden duration extension risk event buried inside the $10 trillion market for mortgage backed securities, which will fall much faster in price than corporate debt. Again, the relevant terms here are volatility and option-adjusted duration.

https://www.theinstitutionalriskanalyst.com/single-post/2017/11/26/The-Yellen-Put

More Iowans Choose Faith-Based Health Plans

NY schools just got bad fiscal news

Pa.’s top pension earners take home hundreds of thousands a year

Bad news for NY schools: Pension costs rising

Fort Worth Is The Latest Texas City To Grapple With Serious …

Snyder: To protect our future, we must pay past debts

Stanford Study: Rising Cost of Public Employee Pensions Eat Up …

The $275K retirement expense you can’t afford to ignore

China’s debt is growing at a faster pace despite years of efforts to …

China’s central bank governor, Zhou Xiaochuan, made global headlines with a warning last month of the risks of a “Minsky moment”, referring to a sudden ..

Japan plans extra budget of $24-26 billion for fiscal 2017: sources