- Market Update & Review

- Never Hurts To Ring The Cash Register

- Portfolio Management Guidelines

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud,Seeking Alpha

Market Update & Review

Fortunately, the market rallied on Friday as traders scrambled to hold important support levels following confirmation from Richard Clarida that the Fed has no intention of moving interest rates anytime soon. Via Bloomberg:

- CLARIDA: INFLATION PRESSURES MUTED, EXPECTED INFLATION STABLE

- CLARIDA: WE’LL WEIGH `WHAT, IF ANY, FURTHER ADJUSTMENTS’ NEEDED

- CLARIDA: FED FUNDS RATE NOW IN RANGE OF NEUTRAL ESTIMATES

- CLARIDA SAYS FED CAN AFFORD TO BE DATA DEPENDENT

- FED’S CLARIDA SAYS U.S. ECONOMY IS IN A `VERY GOOD PLACE’

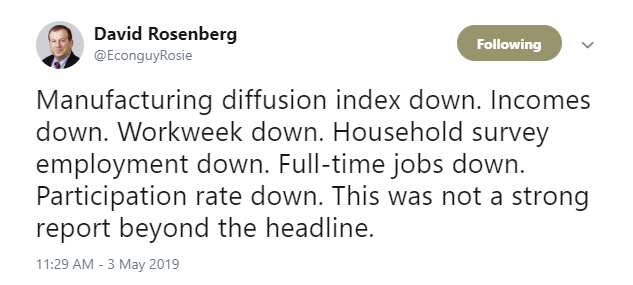

Despite headlines to the contrary, the employment report on Friday was NOT good and we will likely see a good bit of payback next month. David Rosenberg summed it up well:

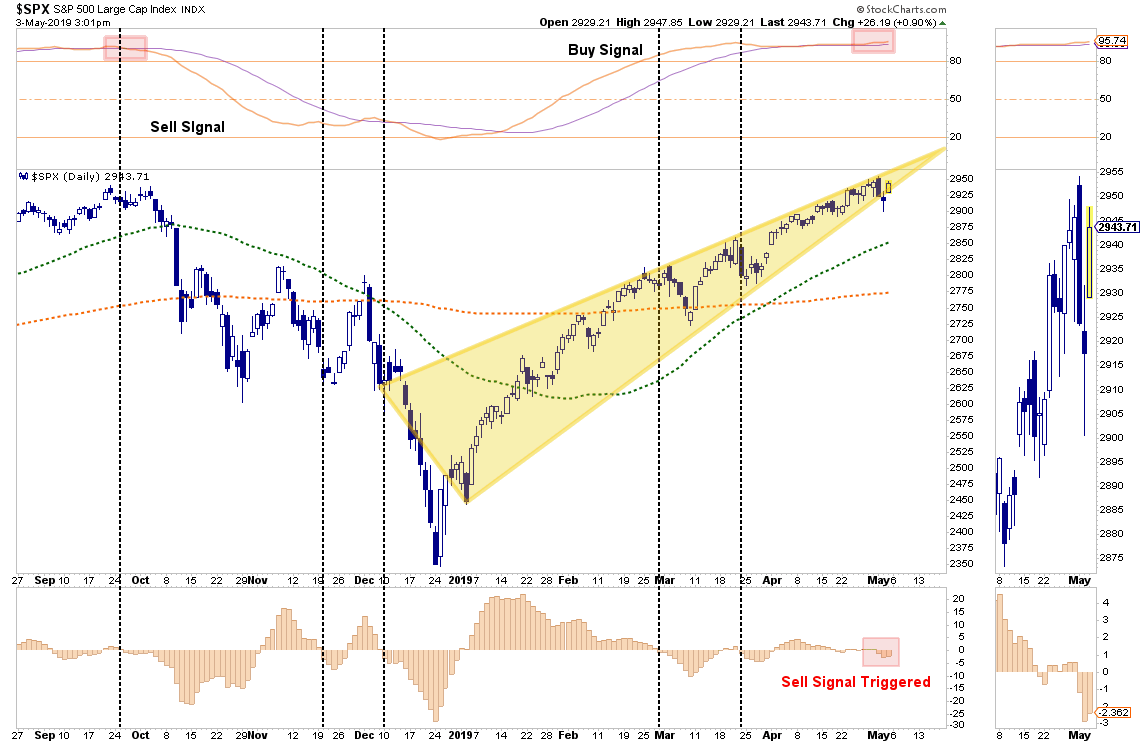

Nonetheless, the market did rally keeping us in the same place as last week.

“While that break to the upside was indeed bullish, the market remains very confined to a rising consolidation pattern and failed to close above the intraday all-time highs from last September. With the markets trading on VERY light volume on Friday, combined short-term ‘sell signals’ forming, and pushing more extreme overbought conditions, it is too early to completely remove all risk management controls in portfolios.”

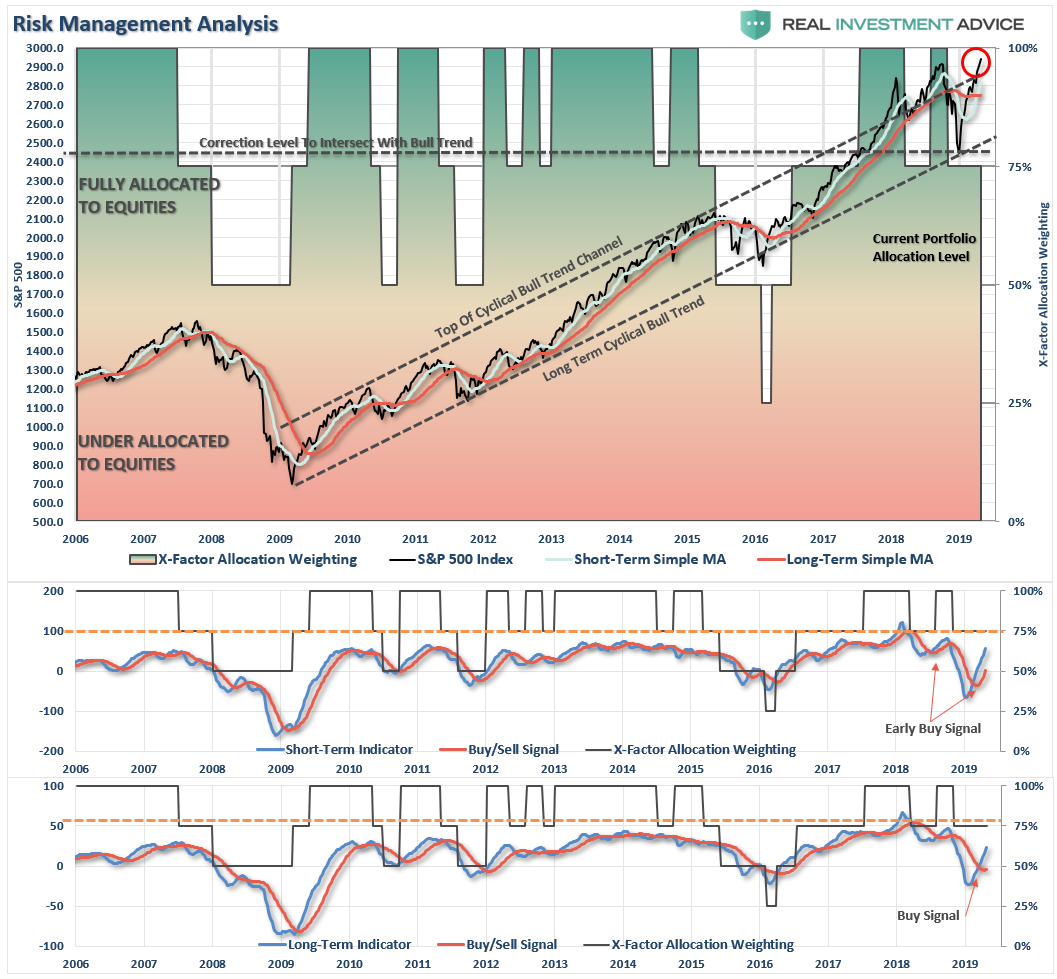

The chart below is updated from last week.

While the market did hold inside of its consolidation pattern, we are still lower than the previous peak suggesting we wait until next week for clarity. However, a bit of caution to overly aggressive equity exposure is certainly warranted.I say this for a couple of reasons.

- The market has had a stellar run since the beginning of the year and while earnings season is giving a “bid” to stocks currently, both current and forecast earnings continue to weaken.

- We are at the end of the seasonally strong period for stocks and given the outsized run since the beginning of the year a decent mid-year correction is not only normal, but should be anticipated.

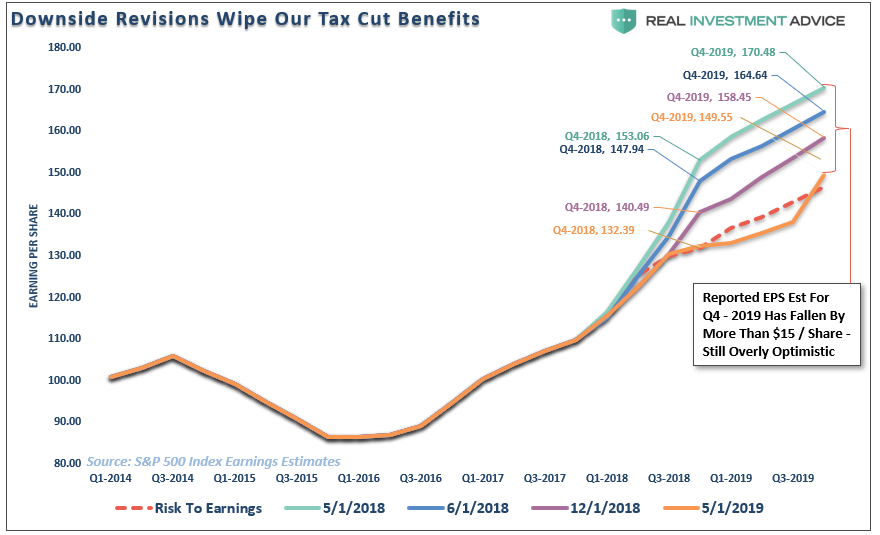

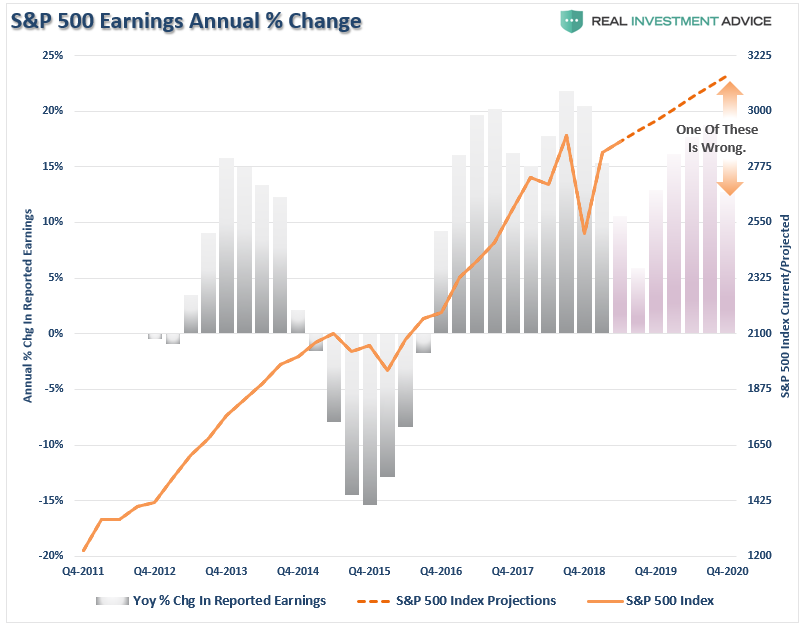

With respect to earnings, and as we have stated many times previously, estimates continue to be revised lower, and have now exceed our original revision target (red dashed line) set out in early 2018.

Note: The Q4-2019 hockey-stick earnings jump WILL BE revised down markedly over the next few months.

Why do I say that?

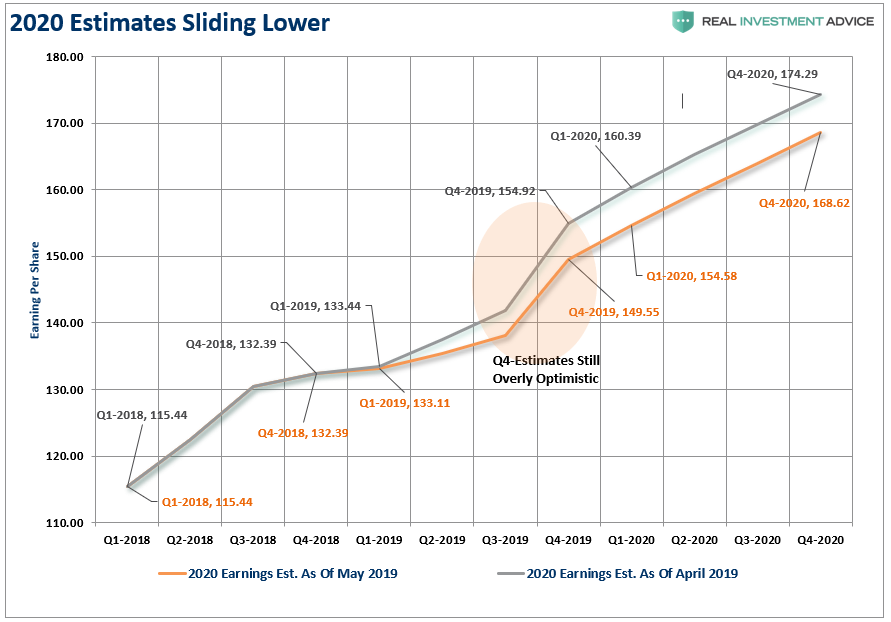

Because 2020 estimates are already being revised down rather sharply as well.

This is important as markets push all-time highs at a time when forward earnings estimates for the next 18-months are all lower than previously estimated. Despite the rise in expected earnings in 2020, the peaks of those expectations (which are predictably about 33% too high currently) are all lower than the 2018 earnings peaks.

In other words, further increases in the markets over the next two years will be a function of multiple expansion rather than increased “value.”

Such an environment tells us a few things about the market.

- In the short-term prices will be driven by momentum and optimism. (1-3 months)

- Over the intermediate-term prices will become more subject to higher volatility due to potential disappointments as “bad news” is treated as “bad news” (4-9 months)

- Longer-term the market is simply a weighing machine and current expectations of 8% annual growth rates in asset prices will be realigned with weaker earnings prospects (10-24 months)

As noted above, the market’s stellar run is set for a breather over the next couple of months. Specifically, as we approach the end of the seasonally strong period, the odds of a “reset” rise markedly. As noted on Thursday by StockTraders Almanac the seasonal “sell” signal has also been triggered. To wit:

“Yesterday after the market closed, we sent out our Tactical Seasonal Switching Strategy Sell Alert for DJIA and S&P 500…we are shifting the ETF Portfolio to a market-neutral position by adding some exposure to short and longer duration bonds.”

Never Hurts To Ring The Cash Register

This brings me to what we did with our equity portfolios last Tuesday and subsequently reported to our RIA PRO subscribers on Wednesday morning. (Try NOW and get 30-days FREE)

“A common theme through today’s report is ‘Profit Taking.’ Over the last couple of weeks, we have continued to discuss taking profits and rebalancing risks. Yesterday we sold 10% of our many of holdings prior to earnings to capture some profits. We also added to some of our Healthcare holdings which have been under undue pressure and represent value in a market that has little value currently.”

This was also a point Jim Cramer reiterated on CNBC on Thursday:

“Any time you have a remarkable run, it never hurts to take something off the table. Nobody ever got hurt ringing the register,” – Jim Cramer, CNBC

As the old Wall Street saying goes:

“Bulls make money. Bears make money. Hogs get slaughtered.”

Yes, markets are hovering near all-time highs and everything certainly seems to be firing on all cylinders. However, such is ALWAYS the case before a correction begins. Such is the nature of markets.

Currently, the markets have had a stellar run since the beginning of the year, and as we wrote previously if you sold everything today, and went to cash, it is unlikely you will miss much between now and the end of the year. (We aren’t recommending you do that, it is just to illustrate a point)

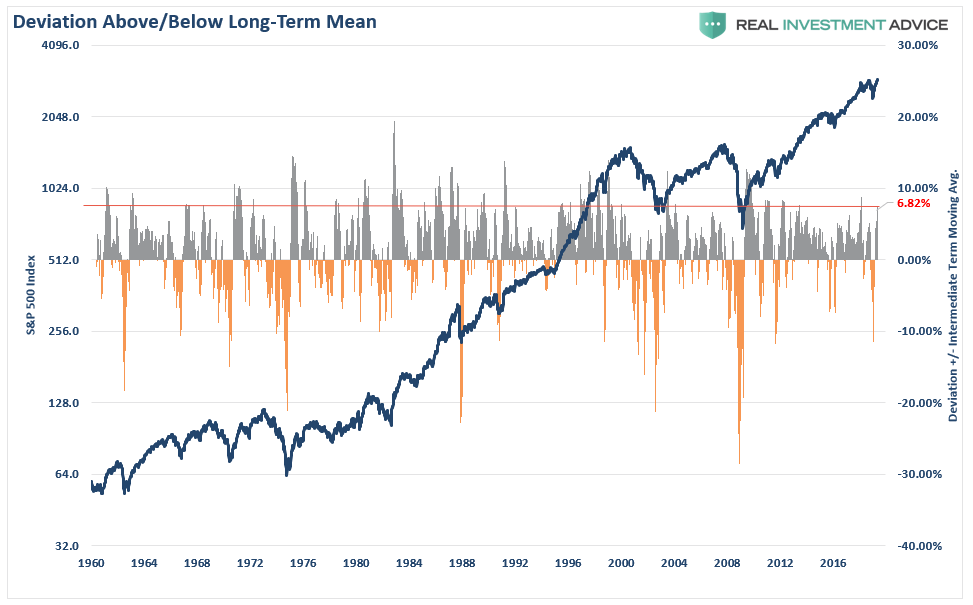

The reason is because of a chart we posted earlier this week in “A Warning About Chasing This Bull Market.”

“At almost 7% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations.”

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019.

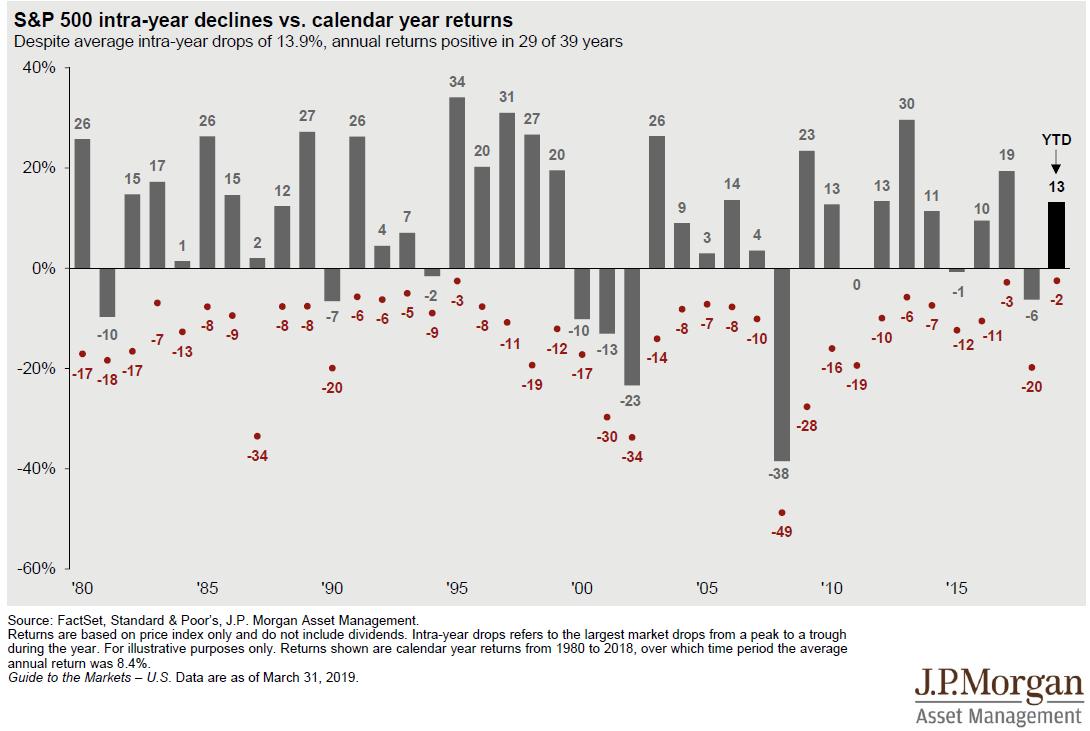

As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.

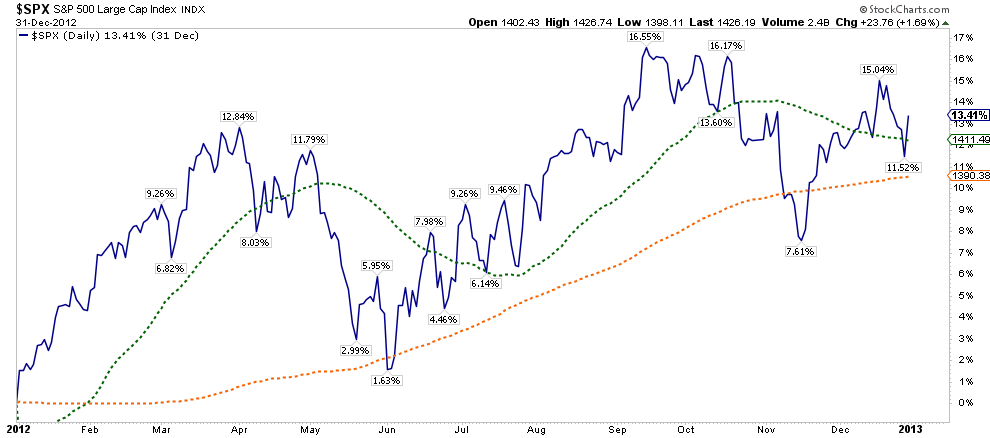

Let’s take a look at what happened the last time the market started out the year up 13% in 2012.

So far, it looks a whole lot like this year.

“From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.”

Given that every given year has some sort of corrective action in it, betting this year will be different is a low probability event.

Doug Kass laid out a decent laundry list of non-trivial risks that not only currently exists but in many cases are expanding.

- Slowing Domestic Economic Growth: I see going forward nominal GDP in the U.S. at nearly recessionary growth levels. There was less than meets the eye in the first-quarter headline Real GDP growth rate of 3.2%. The accumulation of inventories, large doses of government spending and a sharp improvement in exports will likely subtract from the second-quarter growth rate. Moreover, consumer spending is clearly slowing (first-quarter consumer durable spending was down 5%), along with housing and non-residential construction now. Commodities are down in each of the last five days and are now at a seven-week low. Finally, credit card charge-off rates are rising sequentially, as are delinquency rates.

- Slowing Non-U.S. Economic Growth: Economic confidence in the European Union has hit a 10-month low. Hong Kong exports to China are falling post haste (down 10% in March). Finally, last night’s disappointing Chinese data questions the foundation of growth in that region.

- The Earnings Recession: A strengthening currency, sub-4% nominal U.S. GDP growth and rising wage and salary costs pose threats to corporate profitability this year. While estimates have improved from year-end, first-quarter profits still look to be down by more than 2%. According to Rosie (David Rosenberg), fully 84% of those companies issuing guidance have been negative. Second-quarter profits look negative, again. As I have chronicled, profit margins peaked several quarters ago (3Q 2018). Going forward, it seems to me that commodities and interest expenses are likely troughing and that wage growth may accelerate from here, pressing margins. Finally, don’t fall for the fact that 77% of the reporting companies have beat “estimates.” This is what I refer to as the “Twit Olympics” where estimates are taken down and guided to levels that almost certainly will be beat.

- The Last Two Times the Fed Ended Its Rate Hike Cycle, a Recession and Bear Market Followed

- The Strengthening U.S. Dollar: More than 40% of the S&P component’s sales are non U.S.-based. A strong U.S. currency will be a profits headwind over the remainder of 2019.

- Message of the Bond Market: Stated simply, the 10-year U.S. note is sending the message of slowing global economic growth.

- Untenable Debt Levels: I have already spent quite a lot of time making the case that debt is a governor to growth. The greatest subset threat is sovereign debt, which for now is being ignored.

- Credit Is Already Weakening: With GDP up by more than 3% in real terms in the first quarter, one should be asking, “Why are bank credit and leveraged loans weakening?” The proliferation of “covenant lite” financing and the existence of increasingly excessive leverage are worrisome. Bankwide loans are weakening (are inventories bloated?); it’s the most sluggish trend seen since 2016. The ratio of debt upgrades to downgrades this year is also at the worst level in three years. As well, the leveraged loan market is seeing outflows and distressed debt is beginning to see an acceleration in write-offs. Finally, the search for yield, coupled with low interest rates, causes mischief and the misallocation of resources — for example, the silly issuance of 100-year Argentina bonds that now sell for about 66 cents on the dollar (they were issued at par).

- Valuation: Many claim that the “Powell Pivot” and its likely ramifications of lower rates for longer provides a cover for equities. But stocks, currently valued at 17x forward earnings, are now more than two price-to-earnings (P/E) multiple points above the average level of the last decade — a period of time in which rates were mostly at or near generational lows.

- Positioning Is to the Bullish Extreme: As noted last week by my pal Peter Boockvar, chief investment officer at Bleakley Advisory Group, the net speculative position in short VIX futures is at an all-time high. And all-time is a long time.

- Rising Bullish Sentiment (and The Bull Market in Complacency): The CNN Fear & Greed Index is extended toward Greed now. Barron’s Big Money Poll lists only about one-sixth of the respondents as bearish.

- Non-Conformation of Transports: The Dow Theory is shining an amber light in 2019’s sea of market green. I am surprised so few technicians have mentioned this warning flag.

It’s a lot.

However, where that laundry list of worries is long, none of them are going to be the “one” which gets the market. It is the combination of these issues which provide the “fuel” to amplify the impact of an unexpected, exogenous event which ignites selling in the markets.

Since it is ALWAYS and unexpected event which causes sharp declines in asset prices, this is why advisors typically tell their clients “since you can’t predict it, all you can do is just ride it out.”

This is not only lazy, but ultimately leads to the unnecessary destruction of capital and the investors time horizon.

Portfolio Management Guidelines

“Great. Now that you told me all this, what can, or should, I do about it.”

Advice without a solution is not really all that beneficial, so I thought I would share with you the portfolio rules that drive own own investment discipline at RIA Advisors.

While the fundamental, economic and price analysis forms the backdrop of overall risk exposure and asset allocation, it is the following set of rules which define the “control boundaries” for all specific actions.

- Cut losers short and let winner’s run. (Be a scale-up buyer into strength.)

- Set goals and be actionable. (Without specific goals, trades become arbitrary and increase overall portfolio risk.)

- Emotionally driven decisions void the investment process. (Buy high/sell low)

- Follow the trend. (80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

- Never let a “trading opportunity” turn into a long-term investment. (Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

- An investment discipline does not work if it is not followed.

- “Losing money” is part of the investment process. (If you are not prepared to take losses when they occur, you should not be investing.)

- The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

- Never, under any circumstances, add to a losing position. (As Paul Tudor Jones once quipped: “Only losers add to losers.”)

- Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short. (Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

- When markets are trading at, or near, extremes do the opposite of the “herd.”

- Do more of what works and less of what doesn’t. (Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

- “Buy” and “Sell” signals are only useful if they are implemented. (Managing a portfolio without a “buy/sell” discipline is designed to fail.)

- Strive to be a .700 “at bat” player. (No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

- Manage risk and volatility. (Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

These are the rules that we TRY and follow. We are human like everyone else and make mistakes along the way. But those deviations are nearly always quickly punished, lessons are relearned, and course corrections are made.

How you choose to manage your portfolios are up to you. I just hope you find some value in the lessons we have learned the “hard way” over the last 25+ years.

If you need help or have questions we are always glad to help. Just email me.

See you next week.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

If you are NOT an RIA PRO subscriber you are missing the most important part of each weeks’ newsletter.

- Sector & Market Performance Analysis

- Portfolio Recommendations

- What We Are Doing With Our Clients.

Try it today for FREE for 30-days.

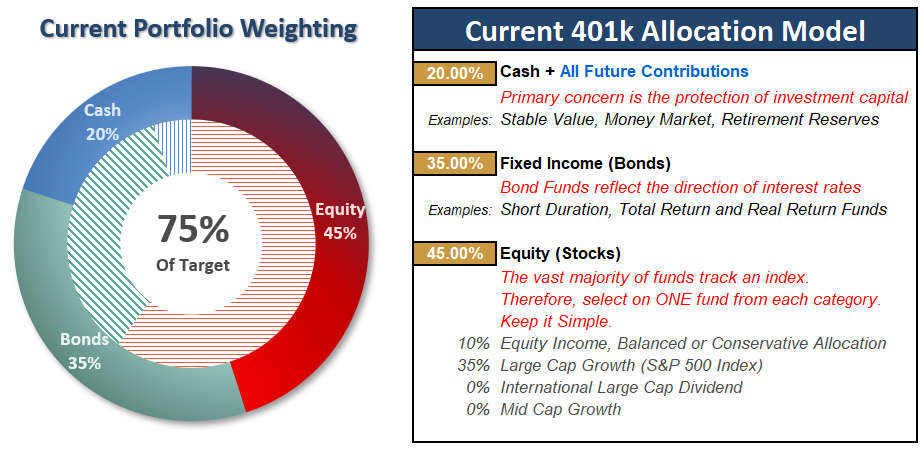

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Sell In May

The market finished just about where it started last week. The good news is that the break of the consolidation pattern was narrowly reversed on Friday keeping offense on the field for now. However, a “seasonal sell” signal was triggered which also keeps us a bit more cautious as we head into the “dog days of summer.”

As stated above, given the run higher this year, a retracement this summer is highly likely which will provide the best opportunity to tactically take portfolios to 100% of target. As stated last week:

“As is always the case, by the time these more ‘bullish” actions occur, the risk/reward opportunity in the short-term is not generally favorable. In this case, in particular, the angle of ascent of the markets from the December lows has been more abnormal than not.”

That opportunity is coming soon, and is why “patience” is required when investing.

Again, with both “buy” signals now in place we WILL move target allocations move to 100% equity exposure on any corrective actions which reduces the extreme overbought short-term condition without violating important support.

In the meantime, we can prepare for this opportunity by continuing our actions we have recommended over the last several weeks.

- If you are overweight equities – take some profits and reduce portfolio risk on the equity side of the allocation. However, hold the bulk of your positions for now and let them run with the market.

- If you are underweight equities or at target – remain where you are until the market gives us a better opportunity to increase exposure to target levels.

If you need help after reading the alert; don’t hesitate to contact me.

Exciting News – the 401k Plan Manager is “Going Live”

We are making a “LIVE” version of the 401-k allocation model which will soon be available to RIA PRO subscribers.You will be able to compare your portfolio to our live model, see changes live, receive live alerts to model changes, and much more.

This service will also be made available to companies for employees. If would like to offer our service to your employees at a deeply discounted corporate rate please contact me.

Stay tuned for more details over the next couple of weeks.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.