Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

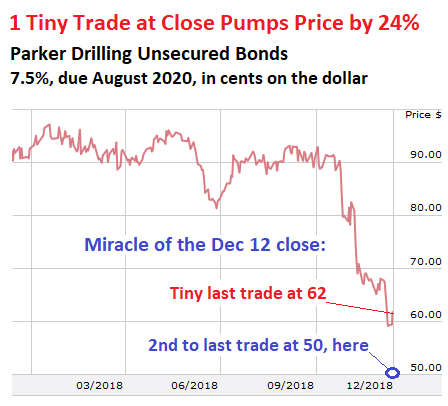

But look how the bonds got manipulated up 24% in one minute at the close.

Parker Drilling announced Wednesday morning that it had filed for a “pre-arranged” chapter 11 bankruptcy. The storied drilling contractor has been in business since 1934. It has been involved in oil fields from Alaska’s Prudhoe Bay and the Siberian Arctic to the Caspian Sea and China, in addition to its work in the US. The company had somehow survived the first Oil Bust this decade (now called “Oil Bust 1,” 2015-2016), but was so weakened that it became one of the first casualties of Oil Bust 2.

The bankruptcy filing was under an agreement with a group of creditors, the company said, with the idea to allow the company to restructure quickly. This is a classic “debt restructuring” under the supervision of a court.

The company listed $691 million in assets. This is down from$869 million in assets in its 10-Q filing with the SEC in November. And it listed $937 million in debts. This includes about $585 million that it owes to unsecured bondholders.

But top executives will be just fine.

We’ll get into more detail in a moment, but to summarize the eternally long agreement with creditors: Existing common shareholders will be almost wiped out. Creditors will get much of the new company along with some new debt. The company will reduce its debt by two-thirds and will get $95 million in new equity capital through a rights offering, which will leave it in better shape than before. And management, instead of being tarred and feathered and driven out of town for having ridden the company to ruin, will be richly reward going forward.

The deal and the filing, though long expected, must have nevertheless come as a surprise to penny-stock chasers because shares today plunged 61% from nearly nothing to even less, closing at 43 cents.

On November 22, Parker Drilling was at the top of my list of 438 stocks traded on the New York Stock Exchange that had plunged between 40% and 94% from their 52-week highs. At the time, shares closed at $1.39. Penny-stock dip chaser seeing a buying opportunity in this “cheap” stock have since been crushed. The shares went from $21 to 43 cents in less than a year.

The largest shareholders, according to the filing, include Saba Capital Management, Brigade Capital Management, Dimension Fund Advisors, and Whitebox Advisors.

A similar fate is befalling quite a few oil-and-gas stocks that have survived Oil Bust 1. Oil Bust 2 may turn out to be merciless because the Fed is now raising rates, and financial conditions are tightening for all companies, and the ensuing shakeout is tripping up weakened survivors of Oil Bust 1 first.

Bondholders started smelling a rat on October 22. For example, the 7.5% senior unsecured notes due in August 2020 traded at around 90 cents on the dollar until October 22, then they began plunging. In November, Parker Drilling warned it might not be able to repay or refinance some of its debts. Bonds plunged further. Over the last couple of days, they traded at below 60 cents on the dollar, according to FINRA/Morningstar data.

1 Tiny Trade pumps bonds 24% at the close today.

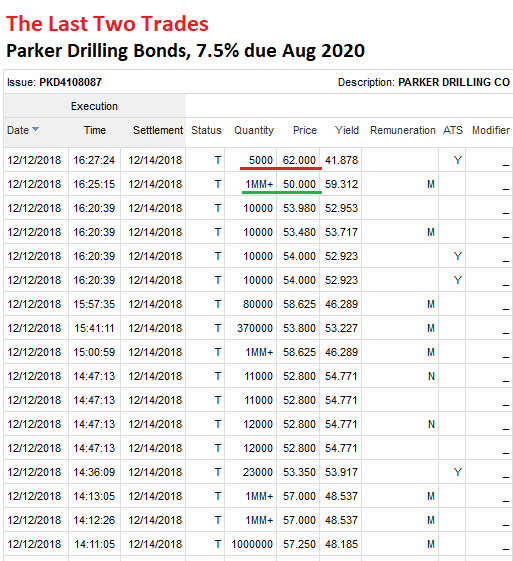

Today, after the bankruptcy filings, trades gyrated wildly allover the place, ranging from 45 cents to 62 cents on the dollar. When you look at the transaction history, you can see how crazy this is – and how profoundly manipulated.

The last tiny trade (underlined in red, below) was at 62 cents on the dollar, executed at 4:27 PM, to be the trade that would show the daily closing price.

But the trade before it, executed at 4:25 PM, was a much larger transaction, at 50 cents on the dollar (underlined in green). Data, table, and chart via FINRA/Morningstar:

Had 50 cents on the dollar been the price of the closing transaction, the chart would have shown the bonds to have plunged nearly 20% today to 50 cents on the dollar. But thanks to the tiny last-moment trade at 62 cents, which pushed up the price for everyone by 24% in a single stroke, the chart shows a gain. I have marked the last trade at 62 and the second to last trade at 50. Go figure!

Ironically, Moody’s still rates these bonds Caa2; Standard& Poor’s rates them even higher, B-, both in deep junk but well above “default” (my cheat sheet on credit ratings)

Who gets what? The #1 Issue in Bankruptcy Court.

Existing common shares and existing preferred shares will be cancelled. Their holders will get some crumbs and can participate in the rights offering by buying rights to the New Common Shares to be issued. Here is what the company said the Capital Stock of New Company will be, post-closing, on a fully-diluted basis (rounded). I highlighted the common stock:

New Company Capital Stock:

- Rights Offering (see below): 41.9%;

- Put Option Equity Premium: 3.4%;

- Converted 2020 Notes: 18.8%;

- Converted 2022 Notes: 34.4%;

- Existing Preferred Stock: 0.6%;

- Existing Common Stock: 0.9%.

Of the New Common Stock offered in the Rights Offering:

- Holders of unsecured notes can purchase up to 63.2%;

- Holders of existing common stock can purchase up to 22.1%;

- Holders of existing preferred stock can purchase up to 14.7%.

Holders of existing common stock will also receive 60% of the new warrants, and holders of existing preferred will receive 40% of the new warrants. At this point, no one knows if these warrants will ever have any value.

But you gotta take care of your own.

The executives, having ridden the company into bankruptcy, will be retained and richly compensated going forward. For example, Chairman and CEO Gary Rich: He became CEO in October 2012 and Chairman in May 2014. He negotiated for himself an annual base salary of $745,000 with an annual bonus of $1.49 million, plus a target bonus, plus 49.8% of the Incentive Equity Pool exclusively set up for a handful of executives.

This Equity Incentive Pool will get “no less than” 9% of the New Common Stock. Up to 40% of this pool will be issued to the participating executives as restricted stock of the new company and up to 60% will be issued as non-qualified stock options in the new company.

The company expects to emerge from bankruptcy protection in early 2019. The restructuring plan is subject to court approval and stakeholder approval.