Purchasing a house is one of the largest financial transactions an individual will make in his or her life. Yet, many people tend to glaze over some key points when they consider purchasing a home. These include solidly understanding where we are in our current interest rate cycle, where rates are headed, knowing if real estate is too expensive and if one should wait before purchasing.

Current Interest Rate Cycle: Where Are We?

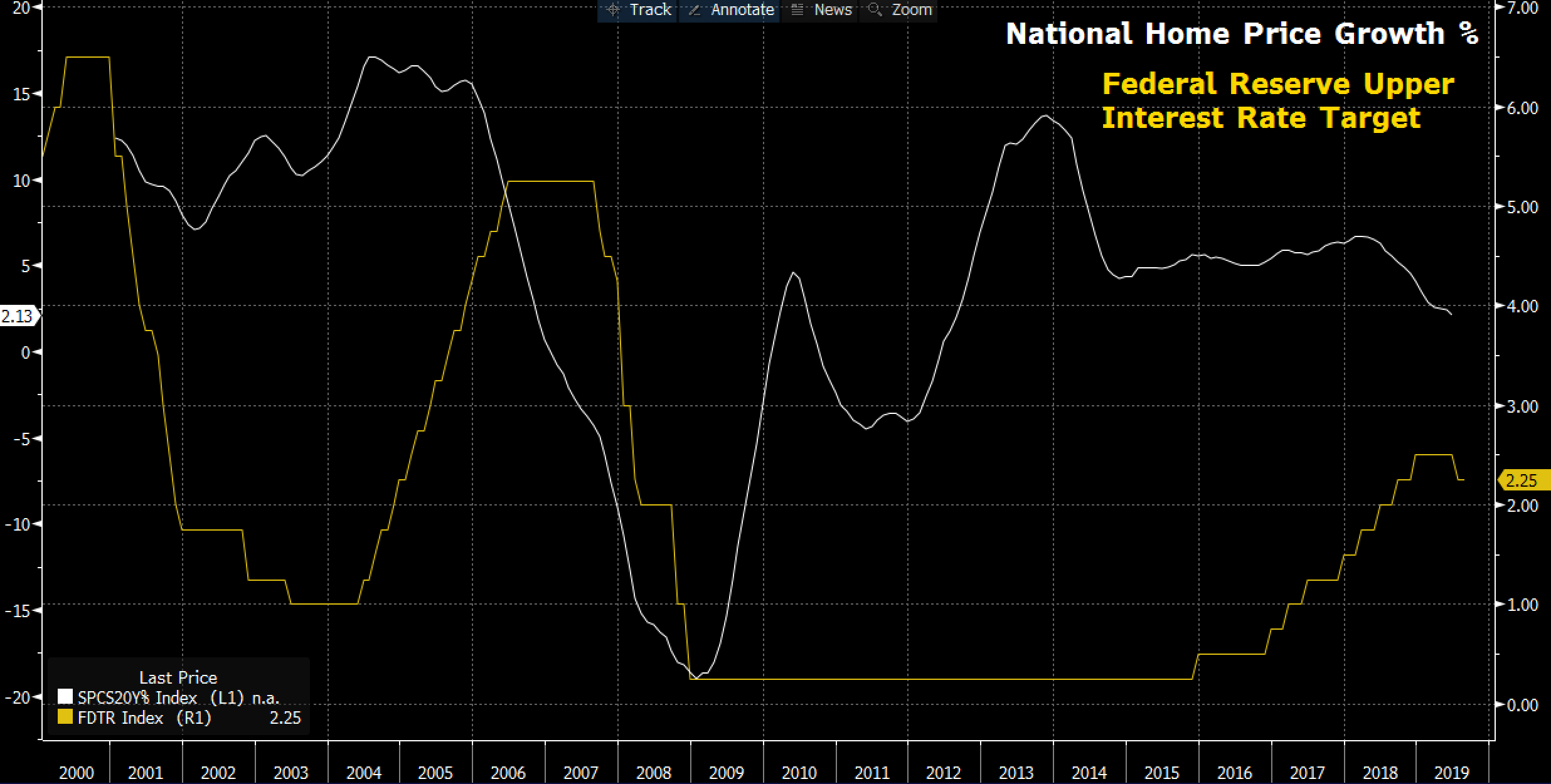

You can see that as weakness in the economy permeates and eventually lowers housing prices, the Federal Reserve is forced to lower interest rates. This loosening is an attempt to make home buying, and overall lending, more attractive so that consumers and lenders alike will stimulate the economy.

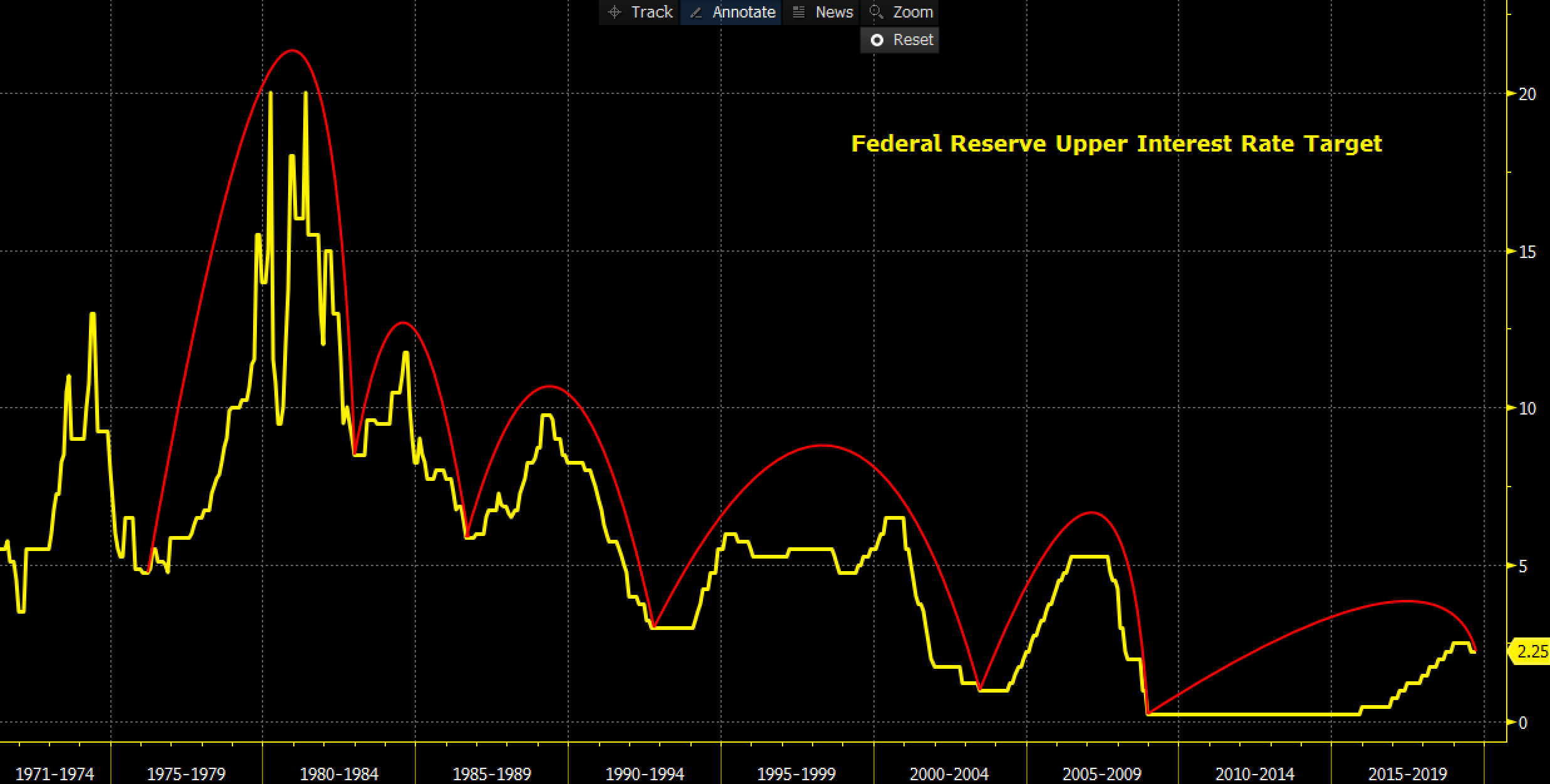

The Federal Reserve recently made its first rate cut since 2008. While interest rate cycles aren’t always linear on the way up or down, our current cycle lasted for 128 months. This is the second longest behind the 1992-2003 cycle shown by the green curve in the chart below. As of the third quarter 2019, many economists predict further downside to interest rates.

Where Are Interest Rates Going?

Interestingly, every interest rate cycle since the ‘80s has peaked lower and lower. With more of a push toward globalization, more economies are working at full capacity and aren’t experiencing the year-over-year growth that propelled globalization from the ‘80s to now. On top of this, we have a much more service-based economy that increasingly relies on consumerism with less and less emphasis on manufactured goods. This shift in the way Americans exchange value isn’t always captured in proportion by GDP, which of course, is a huge metric for the Federal Reserve when considering their stance on national monetary policy.

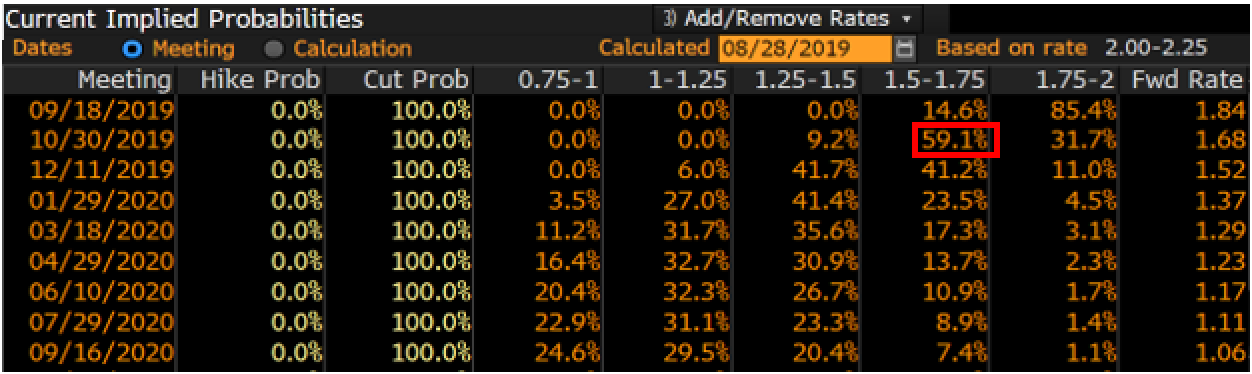

I expect the Federal Reserve’s upper bound interest rate target to decline, given that global macroeconomic data has had a sustained period of decline with areas in complete contraction. The Federal Funds futures are financial contracts that represent the market’s opinion about where the Federal Funds rate will be at the end of the contract. The probabilities these contracts imply are shown above. These speculators bet it’s more likely than not that we’ll be .5% lower by the end of October than we are now (2.25%). This could come in the form of two .25% rate cuts; one on Sept. 18 and another on Oct. 30, or as a one .5% rate cut. A .5% rate cut would imply the Federal Reserve has deep concerns about the economy and wants to take quick action to backstop whatever issue they might foresee.

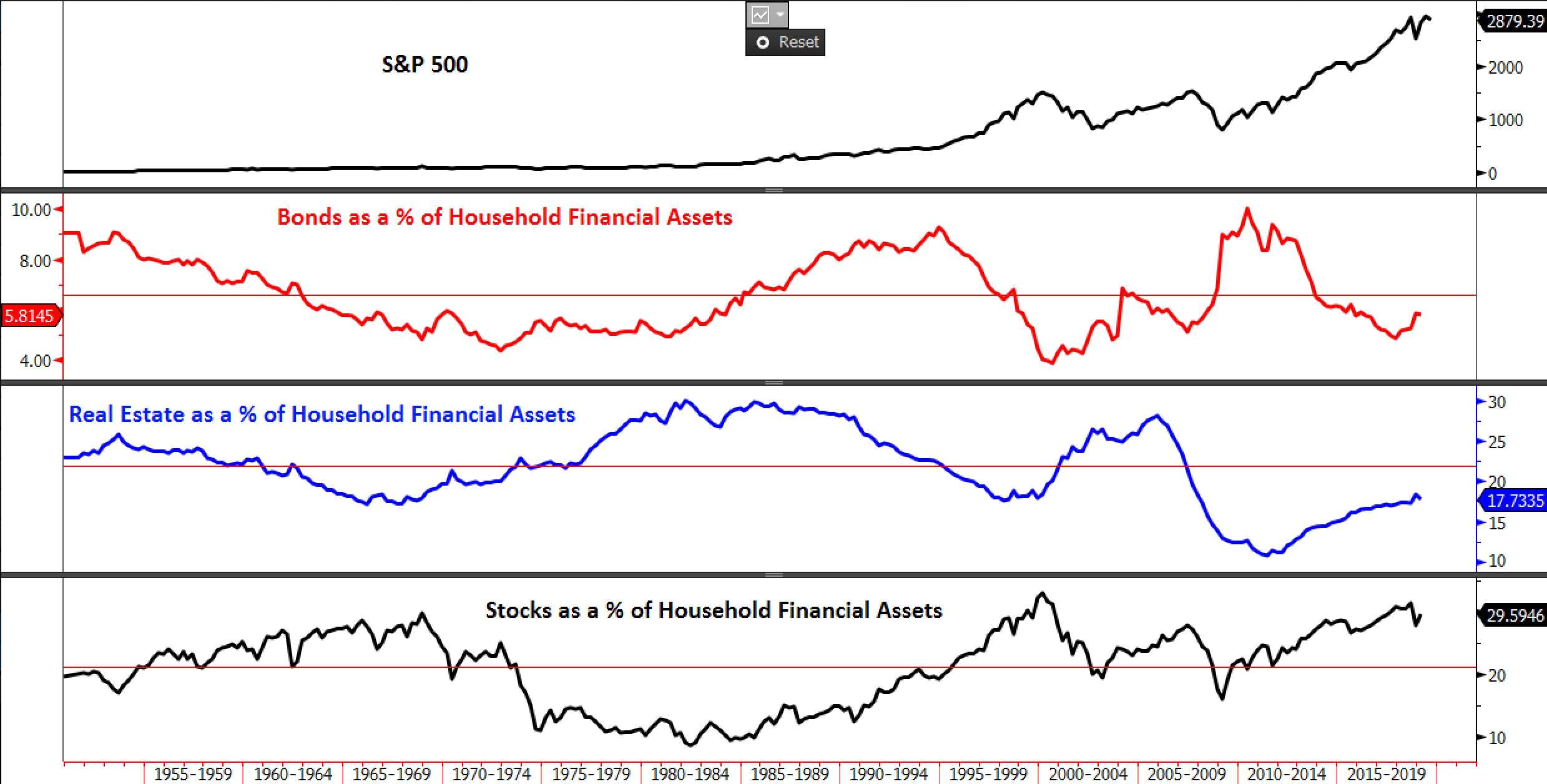

The chart above is one of my all-time favorites. The lines, from top to bottom, show the S&P 500, bonds as a percent of household net worth, real estate as a percent of household net worth and stocks as a percent of household net worth. The horizontal red lines on each panel represent the average for each of those respective assets as a percent of household ownership. An investor would be wise to sell what is highly valued, due to high demand and ownership of that asset, and buy what is cheap as demand is low and potential for an increase in demand is high.

Take, for example, the tech bubble in which the chart above would have demonstrated stocks were overvalued compared to their average percent of ownership assets, bonds were near all-time lows as a percent of household balance sheets and real estate had just gone below its average ownership rate. This would have been nice to see back then. Currently, the chart above would suggest: Bonds = BUY, Real Estate = BUY/HOLD, Stocks = SELL.

Real estate has appreciated significantly since the 2008 financial crisis and some homes are worth more now than they were before the bubble. But this doesn’t imply it’s a bad time to buy a house. Real estate is not a saturated market and is still below its long-term average as a percent of household net worth.

Conclusion

If purchasing a home is your next financial venture, good for you. Although it’s not the most optimal time to enter the housing market, the likely future of interest rates and current rate of home value as a percent of household financial assets still show that it can be an attractive opportunity. Our Financial Sense team wishes you the best of luck! Make sure to consider an adjustable rate mortgage (ARM) and do your research before making any financial decisions.

Disclosures: This article in no way attempts to make any recommendations toward investing or not investing in real estate. This article is meant to assist retail investors and prospective homebuyers in understanding the macro forces at play in the real estate market and provide insight into the market via data information.