Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

So what’s going on here?

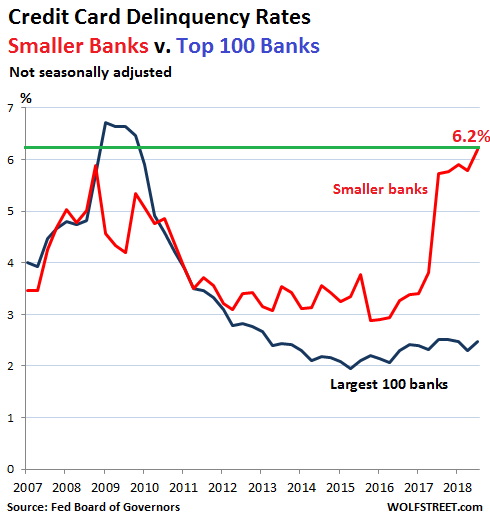

In the third quarter, the “delinquency rate” on credit-card loan balances at commercial banks other than the largest 100 banks – so the delinquency rate at the 4,705 smaller banks in the US – spiked to 6.2%. This exceeds the peak during the Financial Crisis for these banks (5.9%).

The credit-card “charge-off rate” at these banks, at 7.4% in the third quarter, has now been above 7% for five quarters in a row. During the peak of the Financial Crisis, the charge-off rate for these banks was above 7% four quarters, and not in a row, with a peak of 8.9%

These numbers that the Federal Reserve Board of Governors reportedMonday afternoon are like a cold shower in consumer land where debt levels are considered to be in good shape. But wait… it gets complicated.

The credit-card delinquency rate at the largest 100 commercial banks was 2.48% (not seasonally adjusted). These 100 banks, due to their sheer size, carry the lion’s share of credit card loans, and this caused the overall credit-card delinquency rate for all commercial banks combined to tick up to a still soothing 2.54%.

In other words, the overall banking system is not at risk, the megabanks are not at risk, and no bailouts are needed. But the most vulnerable consumers – we’ll get to why they may end up at smaller banks – are falling apart:

Credit card balances are deemed “delinquent” when they’re 30 days or more past due. Balances are removed from the delinquency basket when the customer cures the delinquency, or when the bank charges off the delinquent balance. The rate is figured as a percent of total credit card balances. In other words, among the smaller banks, at the end of Q3, 6.2% of the outstanding credit card balances were delinquent.

So what’s going on here?

The credit card business is immensely profitable, and so banks are willing to take some risks. It’s immensely profitable for three reasons:

- The fee the bank extracts from every transaction undertaken with its credit cards (merchant pays), even if the credit-card holder pays off the balance every month and never incurs any interest expense.

- The fees the bank extracts from credit card holders, such as annual fees, late fees, etc.

- The huge spread between the banks’ cost of funding and the interest rates banks charge on credit cards.

So how low is the banks’ cost of funding? For example, in its third-quarter regulatory filing with the SEC (10-Q), Wells Fargo disclosed that it had $1.73 trillion in total “funding sources.” This amount was used to fund $1.73 trillion in “earning assets,” such as loans to its customers or securities it had invested in.

This $1.73 trillion in funding was provided mostly by deposits: $465 billion in non-interest-bearing deposits (free money), and $907 billion in interest bearing deposits; for a total of $1.37 billion of ultra-cheap funding from deposits.

In addition to its deposits, Wells Fargo lists $353 billion in other sources of funding – “short-term and long-term borrowing” – such as bonds it issued.

For all sources of funding combined, so on the $1.73 trillion, the “total funding cost” was 0.87%. Nearly free money. Rate hikes no problem.

In Q3, Wells Fargo’s credit-card balances outstanding carried an average interest rate of 12.77%!

So, with its cost of funding at 0.87%, and the average interest rate of 12.77% on its credit card balances, Wells Fargo is making an interest margin on credit cards of 11.9 percentage points. In other words, this is an immensely profitable business – hence the incessant credit-card promos.

With credit cards, the US banking system has split in two.

The largest banks can offer the most attractive incentives on their credit cards (cash-back, miles, etc.) and thus attract the largest pool of applicants. Then they can reject those with higher credit risks – having not yet forgotten the lesson from the last debacle.

The thousands of smaller banks cannot offer the same incentives and lack the marketing clout to attract this large pool of customers with good credit. So they market to customers with less stellar credit, or with subprime-rated credit — and charge higher interest rates. 30% sounds like a deal, even if the customer will eventually buckle under that interest rate and will have to default.

That’s why banks take the risks of higher charge-offs: They’re getting paid for them! But at some point, it gets expensive. And if it takes a smaller bank to the brink, the FDIC might swoop in on a Friday evening and shut it down. No biggie. Happens routinely.

The real problem with credit cards isn’t the banks – credit card debt is not big enough to topple the US banking system. It’s the consumers, and what it says about the health of consumers.

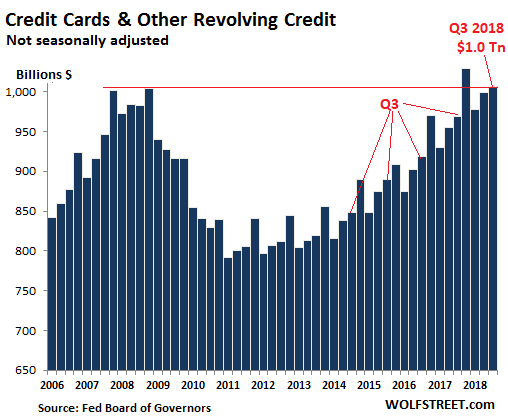

The overall numbers give a falsely calming impression. Credit card debt and other revolving credit has reached $1.0 trillion (not seasonally adjusted). This is about flat with the prior peak a decade ago.

Since the prior peak of credit-card debt in 2008, the US population has grown by 20 million people, and there has been a decade of inflation and nominal wage increases, and so the overall credit card burden per capita is far lower today than it was in 2008 (though student loans and auto loans have shot through the roof). So no problem?

But this overall data hides the extent to which the most vulnerable consumers are getting into trouble with their credit cards, having borrowed too much at usurious rates. They’ll never be able to pay off or even just service those balances. For them, there is only one way out – to default.

The fact that this process is now taking on real momentum — as demonstrated by delinquency rates spiking at smaller banks — shows that the group of consumers that are falling apart is expanding. And these are still the good times, of low unemployment in a growing economy.