The fact we have the lowest interest rates in 5000-years is indicative of the economic challenges we face. Such was a note brought to my attention by my colleague Jeffrey Marcus of TPA Analytics:

“BofA wants you to know that ‘Interest rates haven’t been this low in 5,000-years.‘ That’s right, 5000 years. ‘In the next 5,000 years, rates will rise, but no fear on Wall Street this happens anytime soon,’ said David Jones, director of global investment strategy at Bank of America. This should not come as a shock to anyone who has been watching, given that the FED’s balance sheet is now an astonishing $8.5 trillion and that fiscal spending has caused the U.S. debt to balloon to over $28 trillion (For reference, the U.S. GDP is $22 trillion).

All of this really means that the FED and the U.S are in a tough spot. They need a lot of growth to dig out from mountains of debt, but they cannot afford for rates to move too high or debt service will become an issue.“

Yes, rates will probably rise at some point in the next 5000-years. However, currently, the primary argument is that rates must increase because they are so low.

That argument fails in understanding that low rates are emblematic of weak economic growth rates, deflationary pressures, and demographic trends.

Short-Term Rate Rise Can’t Last

In recent weeks, interest rates rose sharply over concerns of a debt-ceiling default and inflationary fears. But, asMish Shedlock noted, five factors are spooking the bond market.

- Debt Ceiling Battle: Short Term, Low Impact

- Supply Chain Disruptions: Medium Term, Medium Impact

- Trade Deficit: Long Term, Low-to-Medium Impact

- Biden’s Build Back Better Spending Plans: Long Term, High Impact

- Wage Spiral: Long Term, High Impact

“I said early on that if Progressives get their way on spending plans, especially their demands to have 80% clean energy by 2030 it would set off a bout of stagflation. The rise in bond yields and a slowing economy are now linked.” – Mish Shedlock

He is correct. The problem, however, between today, and the 1970s, is the massive debt and leverage levels in the U.S. economy. Thus, any significant rise in rates almost immediately leads to recessionary spats in the economy.

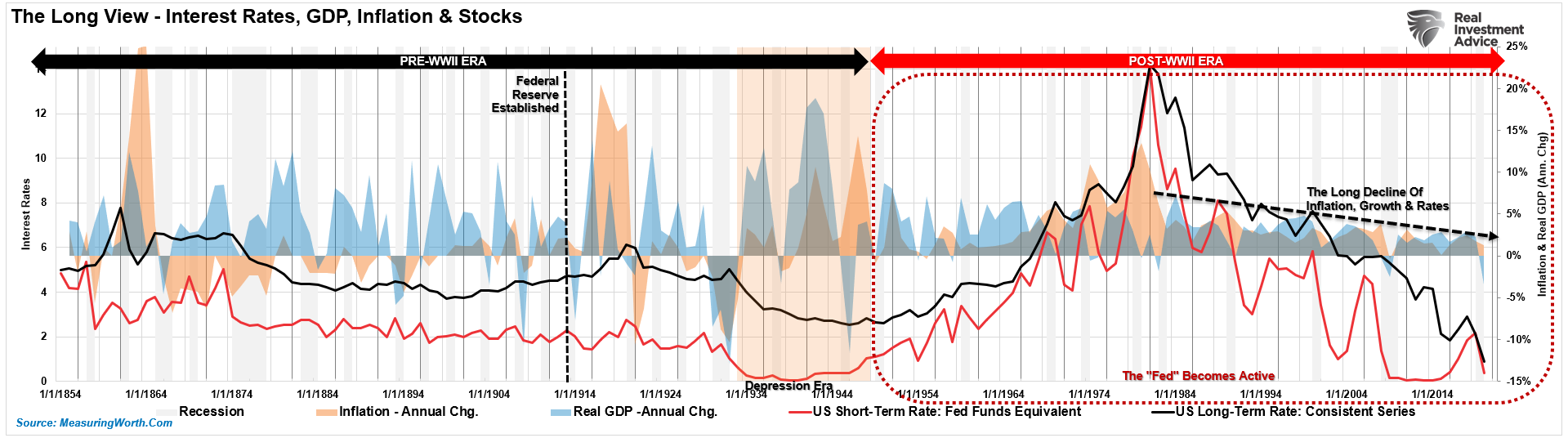

A Long History Of Rates & Economic Growth

The chart below shows a VERY long view of interest rates in the U.S. (equivalent rates to the Federal Funds Rate and 10-year Treasury) since 1854.

Interest rates are a function of the general trend of economic growth and inflation. More robust rates of growth and inflation allow for higher borrowing costs to be charged within the economy. Such is why bonds can’t be overvalued. To wit:

“Unlike stocks, bonds have a finite value. At maturity, the principal gets returned to the lender along with the final interest payment. Therefore, bond buyers are very aware of the price they pay today for the return they will get tomorrow. As opposed to an equity buyer taking on investment risk, a bond buyer is loaning money to another entity for a specific period. Therefore, the interest rate takes into account several substantial risks:”

- Default risk

- Rate risk

- Inflation risk

- Opportunity risk

- Economic growth risk

“Since the future return of any bond, on the date of purchase, is calculable to the 1/100th of a cent, a bond buyer will not pay a price that yields a negative return in the future. (This assumes a holding period until maturity. One might purchase a negative yield on a trading basis if expectations are benchmark rates will decline further.) “

What Caused Rates To Rise Previously

Interest rates rose during three previous periods in history. During the economic/inflationary spike in the early 1860s and again during the “Golden Age” from 1900-1929. The most recent period was during the prolonged manufacturing cycle in the 1950s and 60s. That cycle followed the end of WWII where the U.S. was the global manufacturing epicenter.

However, notice that while interest rates fell during the depression era, economic growth and inflationary pressures remained robust. Such was due to the very lopsided nature of the economy at that time. Much like the current economic cycle, the wealthy prospered while the middle class suffered. Therefore, money did not flow through the system leading to a decline in monetary velocity.

Currently, the economy once again is bifurcated. The upper 10% of the economy is doing well, while the lower 90% remain affected by high joblessness, stagnant wage growth, and low demand for credit. Moreover, for only the second time in history, short-term rates are at zero, and monetary velocity is non-existent.

The difference is that during the “Great Depression,” economic growth and inflationary pressures were at some of the highest levels in history. Today, the economy struggles at a 2% growth rate with inflationary pressures detracting from consumptive spending.

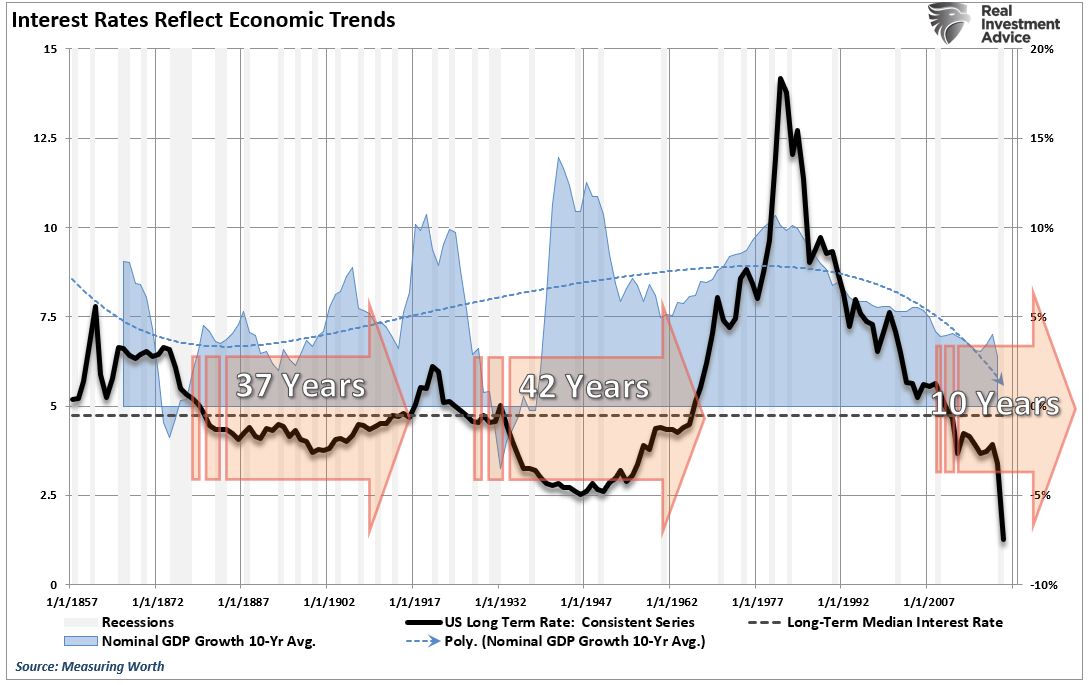

Low Rates Can Last A Long Time

Interest rates are ultimately a reflection of economic growth, inflation, and monetary velocity. Therefore, given the globe is awash in deflation, caused by weak economic output and exceedingly low levels of monetary velocity, there is no pressure to push rates sustainably higher. The dashed black line is the median interest rate during the entire period.

(Note: Notice that a period of sustained low interest rates below the long-term median averaged roughly 40 years during both previous periods. We are only currently 10-years into the current secular period of sub-median interest rates.)

The following chart overlays the 10-year average economic growth rate. As you will notice, and as discussed above, rates rise in conjunction with more substantial levels of economic growth. Such is because more substantial growth leads to higher wages and inflation causing rates to rise accordingly.

Today, the U.S. is no longer the manufacturing epicenter of the world. Labor and capital flow to the lowest cost providers to effectively export inflation from the U.S., and deflation gets imported. Technology and productivity gains ultimately suppress labor and wage growth rates over time. The chart below shows this dynamic change which began in 1980. A surge in debt was the offset between lower economic growth rates and incomes to maintain the “American lifestyle.”

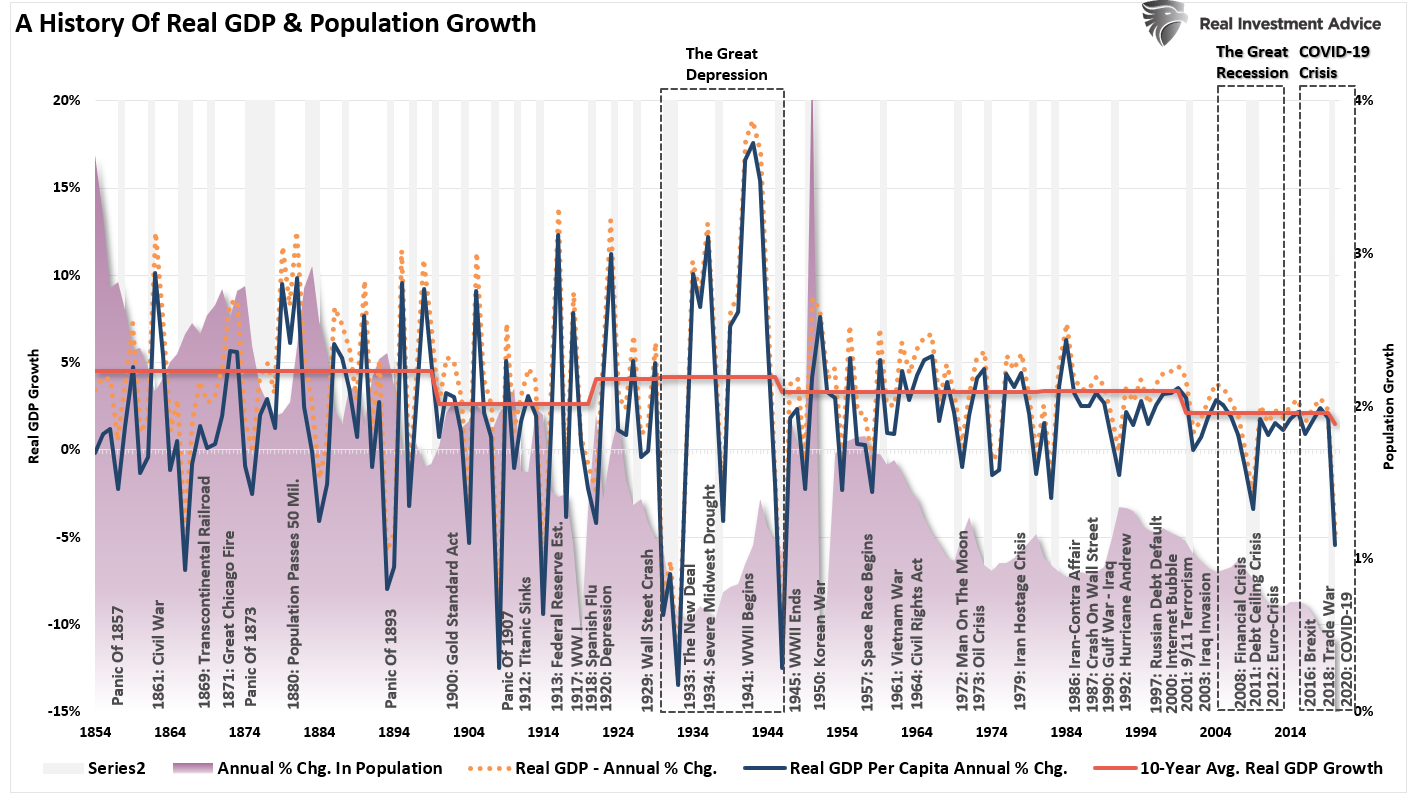

A Demographic Challenge

The chart below shows both the long-view of real, inflation-adjusted, annual GDP growth and on a per-capita basis. I have also included the annual growth rates of the U.S. population. [Data Source: MeasuringWorth.com]

There are some interesting differences between the “Great Depression” and the “Great Recession.” During the depression, the economy grew at 13% and 18% on an annualized basis. Today, the current economic cycle of 2.5% and 2.7%. What plagued the economic system during the depression was the actual loss of wealth following the “Crash of 1929” as a rash of banks went bankrupt, leaving depositors penniless, unemployment soaring, and consumption drained. While the government tried to assist, it was too little, too late. The real depression, however, was not a statistical economic event but rather an absolute disaster for “Main Street.”

During the current period, real economic growth remains lackluster. In addition, real unemployment remains high, with millions of individuals simply no longer counted or resorting to part-time work to make ends meet. Finally, with more than 100-million Americans on some form of government assistance, the pressure on “Main Street” remains.

One crucial difference is the rate of population growth which, as opposed to the depression era, has been on a steady and consistent decline since the 1950s. This decline in population growth and fertility rates will potentially lead to further economic complications as the “baby boomer” generation migrates into retirement and becomes a net drag on financial infrastructure.

Today, despite trillions of dollars of interventions, zero interest rates, and numerous bailouts, the economy has yet to gain any real traction, particularly on “Main Street.”

The End Of The Bond Bubble

The problem with most forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds.

However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American’s participation in the domestic economy. Interest rates, however, are an entirely different matter.

While there is not much downside left for interest rates to fall in the current environment, there is not a tremendous amount of room for increases. Moreover, since interest rates affect “payments,” increases in rates quickly negatively impact consumption, housing, and investment.

Will the “bond bull” market eventually come to an end? Yes, eventually. However, the catalysts needed to create the economic growth required to drive interest rates substantially higher, as we saw previous to 1980, are not available today. Such will be the case for decades to come. The Fed has yet to conclude we are caught in a “liquidity trap” along with the bulk of developed countries.

Over the following 5000-years, rates will eventually rise. But for now, I am long bonds and continue to buy more whenever someone claims the “Great Bond Bull Market Is Dead.”