By Wolf Richter for WOLF STREET.

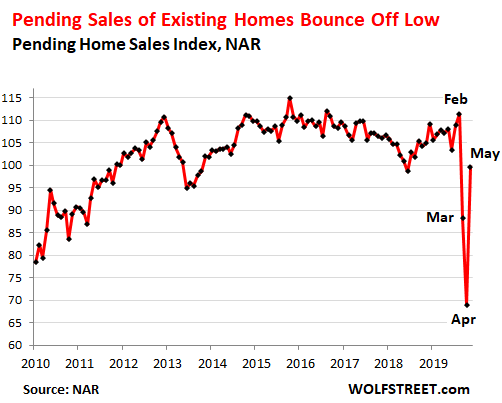

Pending sales of existing houses, condos, and co-ops in May – these are contracts that were signed in May but didn’t close in May – bounced off the brutal pandemic low in April, but remained down 10.6% from February 2020 and down 5.1% from May 2019, according to the National Association of Realtors this morning:

The index of pending sales was set at 100 for the average contract activity in 2001. Pending sales in May are an indication of what closed sales might look like in June and July.

That sales volume collapsed in this historic manner in March and April was a sign that amid the uncertainty, the market had essentially frozen up, with sellers pulling their homes from the market or not listing them in the first place, and buyers staying away in droves.

While many potential sellers still remain reluctant to put their homes on the market, the market is functioning again. The industry has figured out how to deal with the requirements of social distancing, with sellers’ worries about having potentially infected strangers traipse through their home, and with the concerns of everyone else involved in the transaction.

And according to the NAR, “More listings are continuously appearing as the economy reopens, helping with inventory choices.”

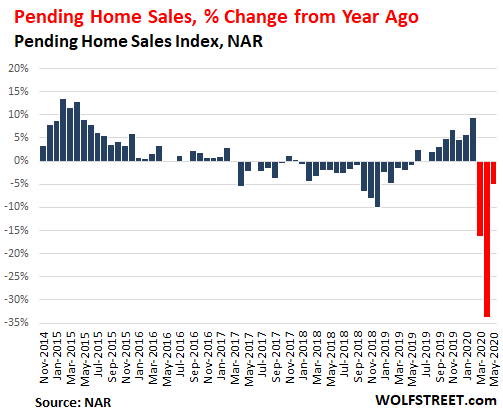

The chart below shows the year-over-year percentage change in pending sales. The three months of year-over-year declines during the pandemic – March, April, and May – are marked in red:

In terms of US regions: Pending sales fell in May 2020 compared to May 2019 in three of the four regions:

- Northeast: -33.2% year-over-year to an index level of 61.5.

- Midwest: -1.4% year-over-year to an index level of 98.8.

- South: +1.9% year-over-year to an index level of 125.5.

- West: -2.5% year-over-year to an index level of 89.2.

This market is facing a historic mess.

Over 30.6 million people are on unemployment compensation, meaning 20% of the labor force, and they’re now out of the housing market.

In addition, 8.5% of all mortgages, or 4.2 million mortgages, are now in forbearance, according to the Mortgage Bankers Association, meaning these homeowners have stopped making payments after getting their lenders to agree not to exercise their rights under the provisions of default.

In the rental market, eviction halts and deals with landlords allow renters to forego paying rent.

Auto lenders too have entered into forbearance agreements with their borrowers rather than repossessing the vehicles due to non-payment.

“Extend and pretend” has become the national policy. No one knows how to get out of it. But extend and pretend doesn’t work forever. And it causes all kinds of long-run damage.

Part of the economy is running on stimulus payments, the extra $600 a week in federal unemployment benefits, massive bailouts of all kinds, and nearly $3 trillion that the Fed threw at the financial markets in a span of three months to inflate stocks and bonds – though those efforts have now halted. So this is a sick puppy we’ve got here.