The Urban Institute has an interesting paper entitled “The Preferred Stock Purchase Agreements Will Hamper Access to Credit.”

“The changes that Trump administration officials made to the preferred Stock Purchase Agreements (PSPAs) – the contracts that govern Fannie Mae and Freddie Mac’s relationship with the US Treasury – would restrict the volume of “high risk” loans they can purchase, as well as the volume of second homes and investor properties. These changes will likely prove binding once the current refinance wave ends and, they will further limit access to mortgage credit and disproportionately affect Black and Hispanic borrowers, as well as the goals of the Biden administration to advance racial equity. In this brief, we review the impact of the changes to the PSPA on credit availability, as well as on future policy actions, and call on the Biden Administration to revisit these contracts to ensure equitable access to the mortgage market.”

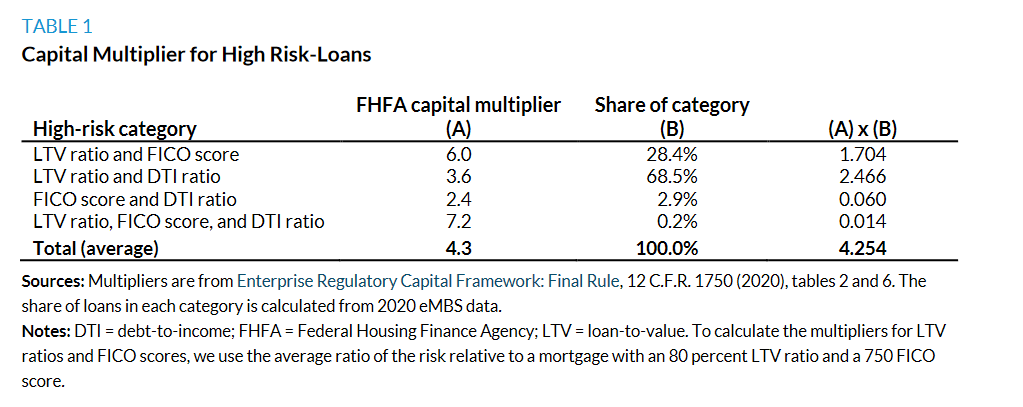

Capital requirements for high-risk purchase loans using the FHFA capital multiplier.Based on the multipliers and the share of 2020 loans in each bucket, we estimate that the high-risk loans will require 4.25 times the capital of low-risk loans.

The median FICO scores, median combined loan-to-value (CLTV) ratios for purchase and refinance mortgages, and median DTI ratios by race and ethnicity in 2019. Black and Hispanic borrowers have lower FICO scores and higher CLTV ratios and DTI ratios than either non-Hispanic white or Asian borrowers.

Table 3 shows that for GSE purchase mortgages made in 2019, more than twice the share of Black and Hispanic borrowers versus white borrowers (8.75 percent versus 4.07 percent) would be considered high risk,as determined by FICO scores and LTV ratios only. This would make it more difficult to expand the credit box to incorporate more Black and Hispanic borrowers. Looking at purchase denials of conventional mortgages, we find 27.4 percent of denials of Black borrowers and 18.1 percent of denials of Hispanic borrowers were considered high risk, as measured by LTV and DTI ratios only. This compares with 8.0 percent of white borrowers and 5.3 percent of Asian borrowers. The refinance denials also show a higher share of Black and Hispanic borrowers in this high-risk category, as defined by the PSPAs, although the absolute numbers are much lower.

If the FHFA is trying to reduce taxpayer exposure to Fannie Mae and Freddie Mac credit losses, then the groups (Black and Hispanic) with poorer credit characteristics like FICO and DTI will suffer more than groups with better credit characteristics (Asian and non-Hispanic white).

This is not in line with what the Biden Administration has in mind. This is called ‘throwing the baby out with the bath water.”