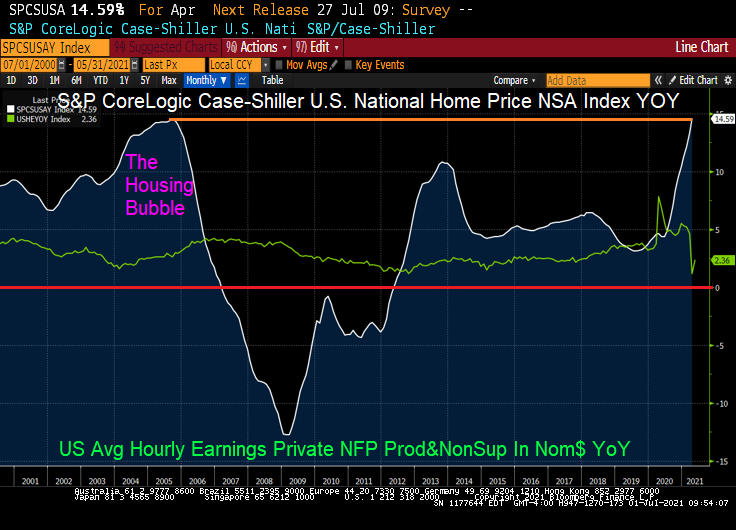

The spread between home price growth and wage earnings is back to the days of the US housing bubble that peaked in 2005. But this time it is different. The 2005 housing bubble was driven by shoddy credit and limited documentation lending. This time the housing bubble is driven by The Federal Reserve.

(Bloomberg Businessweek) — Why, again, is the Federal Reserve adding $40 billion a month to its holdings of mortgage-backed securities when the mortgage market does not seem to be in need of federal assistance?

After all, the national average for 30-year fixed-rate mortgage loans is 3.02%, according to the latest survey by mortgage buyer Freddie Mac Corp. That’s up only a bit from its historic low of under 2.7% in January and February. Cheap loans are fueling a historic rise in home prices that’s making homeowners rich on paper but crushing would-be first-time buyers: The S&P CoreLogic Case-Shiller index of U.S. property values climbed 14.6% in April from a year earlier, the biggest gain in data going back to 1988.

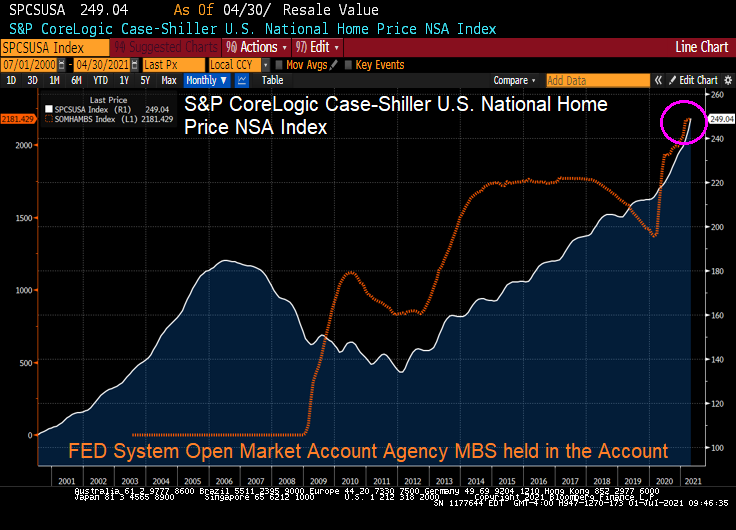

When you get a loan from a bank or a non-bank lender, there’s a good chance it will be packaged into a mortgage-backed security and sold to investors, and there’s a good chance that the ultimate holder will be the Federal Reserve. Which means the Fed could be financing your mortgage. In the week ended June 23, the Federal Reserve owned $2.35 trillion in mortgage-backed securities, according to the Fed’s H.4.1 statistical release. According to the Securities Industry and Financial Markets Association, there were $8.44 trillion in MBS guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae at the end of 2020, so the Fed owns more than a quarter of the MBS market.

The Fed bought 47% of the net issuance of MBS in the fourth quarter if you go by the Fed’s $120 billion quarterly increase in holdings and the SIFMA figures showing that the total of outstanding MBS grew by $257 billion. True, not all mortgages are packaged into agency MBS that the Fed buys. The government-sponsored enterprises’ share of first-lien mortgage originations in the third quarter of 2020 was 61.9%. That share fluctuates, as does total issuance. Back of the napkin, though, multiplying 47% by 62% gives you around 30% of the overall U.S. mortgage market that’s financed by the Federal Reserve.

On June 29, Federal Reserve Governor Christopher Waller said it might be time to start cutting back on the Fed’s support for housing. “I think it’s an easy sell to the public,” he told Bloomberg Television. “The housing market is on fire. We should think carefully about doing MBS purchases, and if we were to taper those first that wouldn’t necessarily be a big issue.”

Fed Chair Jerome Powell is trying to keep the Federal Open Market Committee united behind continuing to buy mortgage-backed securities and Treasuries as a way of holding down interest rates to promote economic growth. The recovery, he says, is incomplete. The U.S. still had 7 million fewer people employed this May than in February 2020, before the pandemic struck.

But Powell hasn’t done a wonderful job of articulating why buying MBS is the right medicine for the economy. It is not, he says—not—a way of supporting the housing market. Read this somewhat confusing excerpt) from the Fed’s official transcript of the FOMC press conference in April, where Powell responds to a question from Greg Robb of MarketWatch:

CHAIR POWELL. Yes. I, I mean, we’re—we started buying MBS because the mortgage-backed security market was, was really experiencing severe dysfunction, and we’ve sort of, sort of articulated, you know, what our exit path is from that. It’s not meant to provide direct assistance to, to the housing market. That was never the intent. It was really just to keep that as—it’s a very close relation to the Treasury market and a very important market on its own. And so that’s, that’s why we, we bought as we did during the Global Financial Crisis; we bought MBS too. Again, not, not an intention to send help to the housing market, which was, which was really not, not a problem this time at all. So—and, you know, it’s, it’s a situation where we will, we will taper asset purchases when the time comes to do that, and those, those purchases will come to zero over time. And that time is not yet.

A better argument might have been, “Look, we’re a big player so we try to spread our money around. Yields on Treasuries and MBS are linked because investors choose between them. Buying MBS helps hold down interest rates on Treasuries and vice versa. All kinds of other interest rates that consumers and businesses pay are pushed down when we buy Treasuries and MBS.”

Or something like that. A market intervention as big and enduring as the Fed’s intervention in housing finance requires a strong and understandable justification.

The various Federal Reserve Presidents like to say that they are in favor of raising rates a pinch … next year or the year after. Meanwhile, the house price bubble grows.