During the Roaring Twenties would anyone have believed you if you told them about the depression and the dust-bowl years that were soon to come? Would they have believed their celebratory excesses during such a “strong economy” could possibly leave them collapsing into the dustbin of history that followed?

I don’t think so. If I gauged what I say in times like these by the public’s willingness to believe me, I wouldn’t have much that is worthwhile to say.

Thirteen fail factors too big and too obvious to deny

Without going into any of the analysis used in my recent series of Patron Posts to explain and substantiate how deeply distressed our economy is, I want to give everyone a quick point-by-point summary of just how ugly this pig really is. (There is not enough lipstick in the world to make it pretty.) So, here goes:

- CEO and consumer sentiment have fallen relentlessly to levels of dread that can truly only be compared to the dot-com bust and the Great Recession and the market and economy’s 2020 polar-bear plunge.

- Food shortages appear highly likely to become a global catastrophe late in the year for many in the world and highly inflationary for all the rest who have enough money to buy their way out of suffering actual hunger. Hunger could easily start to feel like we’ve entered the dust-bowl years by the end of this year.

- Inflation is burning everyone’s face off all over the world with central banks losing credibility because of their astoundingly foolish belief (or claim) that inflation was transitory, forcing them to now show their mettle by doing something about it, which means they will be highly reluctant to lose face even more by caving in on all of their new-found tough talk in order to revert to easing when things get rough as they have in the past whenever the Fed has tightened.

- Corporate and consumer debt have climbed back to extreme levels just as interest is soaring. Bonds and all interest will continue to rise rapidly now that the Fed has released its stranglehold on bond prices. As a result, defaults will rise until we have another Lehman moment that multiplies them so they rise faster. Who knows where that will happen, but it will certainly happen, as it did in the Great Depression and the Great Recession. We are only in the beginning of the crushing central banks will deliver as they rupture the many fault lines of our debt-based economy under the weight of higher interest.

- Sovereign debt, high as it was already, exploded during the Covidcrisis and now MUST face much higher interest, once again raising the specter of nations defaulting with the likelihood of the kind of civil unrest the Eurozone saw during its last episode of default and borderline defaults. Already we see the euro crashing relative to the dollar.

- The housing market is finally stalling due to soaring mortgage rates, and while it may not become the crushing calamity that it became in 2008 when it drove the collapse, it will certainly be an additional heavy weight on an economy that is foremost consumer oriented, which is largely fueled by home construction and all the jobs that construction creates throughout many industries, not just housing, because of all the components that go into housing.

- Civil unrest will begin to seethe because there is so much more to be angry and anxious about after years of feeling crushed by Covid austerity, silenced by censorship, and outvoted by voting machines to where, no matter which way the vote goes, the winner is “not my president.” The US has never been more politically polarized (at least, not since the 60s) and unable to agree on a solution for anything.

- Covid isn’t done, and China is still strangling its own economy in lockdowns. Ports will become more clogged than ever once the Chinese logjam finally breaks. Thus, there will be no immediate end to supply-chain breaks even when China reopens for business. And now governments and the WHO want to convince everyone that Monkeypox is the next pox upon us because the world has seen a whopping 83 cases or something like that. Not to be caught off guard in its ambition to vaccinate everyone, the Biden Admin. has ordered tons of new smallpox vaccines, implying the possibility of new mandatory vaccines to come.

- Energy is entering a serious global crisis due to sanctions that make the OPEC oil embargo of the 70s look smallish and due to years of diminished capital expenditures and tightened regulations. The new sanctions that have particularly exacerbated the shortages will tighten over time as nations sort their way through how they’re going to implement them. Russia isn’t about to retreat, and Ukraine is not about to surrender, making sure those sanctions stay in play for months to come.

- The savings rate in the US has fallen off a cliff. Combine that with what I said above about consumer debt suddenly soaring, and it all indicates consumers are in trouble and will be less resilient to weather any kind of storm.

- That means the job market will flip on its head as people finally have to rush back to work again. Powell will be surprised at how short-lived his buffer is there. People will be looking for jobs just as production is slowing because people cannot afford to buy the things produced and because of the supply and energy shortages that are stopping production and inflating the cost of everything.

- Stocks are grossly overvalued and have not even begun to catch down to where the Fed has to go in order to stop inflation. The S&P, so far, is only halfway back to its mean, yet the old justifications for even stopping at the mean have disintegrated for the reasons above. Usually, when the market finds a bottom from a major fall, it overshoots the mean by as much as it was above the mean. Therefore, the stock market will continue to fall as much as it already has fallen as it comes to grip with all of these things that investors have been blithely denying, and that is if it just reverts to its mean and no further. Existing bonds will also continue to fall in value (rise in yield) as the Fed pushes interest rates higher. The ongoing crash of stocks and bonds will cause an anti-wealth effect that is every bit as devastating to the economy as the wealth effect was stimulative, resulting in a further downward spiral for the economy, causing markets markets to plunge below their mean. To put it simply, stocks have so far to fall, they will create their own downdraft for the economy and for themselves.

- Yet, with all of that, the Fed has not even begun to start its quantitative tightening, and we saw how horribly QT went last time when it was FAR smaller than the amount of money the Fed has promised it will start sucking out of the economy by rolling bonds off its balance sheet on a much more accelerated track in June. QT1 was not “as boring as watching paint dry” and did not “continue on autopilot,” as promised, because the Fed was unable to pull that off during vastly better times than the present. Wait until you feel that downdraft from QT2 hit the present already-declining economy and markets, especially when the Fed doubles the speed at the end of summer … if they ever get that far before everything is reduced to a pile or rubble under their feet.

Fabulous Fed fails

Anyone who thinks this economy is strong and that markets stand even a ghost of chance in weathering all of that is delusional at best. If you’re going to fly Fed Scarelines, you had better pack yourself in a massive bouncy suit if you want that soft landing because it is going to be the thrill ride of your life. A major wakeup call is in the works as markets realize the Fed is not going to come and save them this time. Previous big Fed fails would have been far worse if the Fed had not reversed its promised course and gone back to full-on QE. The Fed cannot so readily do that this time around, and its promised tightening is much more severe than the times when it tried to back away from stimulus, as it did in 2011 only to go back into it in 2012 because its recovery was failing, or when it tried to actually tighten and failed spectacularly as it did in 2018.

The current consumer (and CEO sentiment) downturn can be most accurately compared back to when US Census Bureau sentiment fell to this same level just before the dot-bust and its recession and to when U-Mich sentiment fell to the present sentiment level just before the Great Recession. A much less significant drop in each measure of sentiment occurred in 2011 as we came out of the Great Recession when people suddenly feared we were going into a second dip of the recession because the Fed had pulled life support, which recession was only averted by even greater QE from the Fed. That kind of recession-averting Fed reversion back to easing will not be so readily forthcoming this time, and that drop in sentiment back in 2011 was a mere stumble compared to the present plunge:

As you can see, plunges in sentiment like we are seeing right now only go this far during a recession. People don’t need the government to tell them we are in a recession to start feeling like we are in a recession. They may need the government to say it before they will admit their feelings were right. 2020, of course, was the cliff dive of all dives because of the unprecedented global lockdowns and fear of a plague upon us. Even so, the U-Mich survey has plumbed a far deeper level than it did in 2020 and is now back at the bottom it hit in the pit of the Great Recession. Census Bureau reported sentiment, however, always runs higher at first and then alway plunges lower. So, it has some catching down to do just as it did in 2000.

When sentiment merely stumbled a little back in 2011, the Fed intervened with a huge preemptive move back to QE — something that cannot happen as a lifeline this time. Back then, the Fed had only minor 3% inflation to deal with. So, it didn’t even attempt to raise interest rates, much less to reduce its balance sheet. It just leaped back to QE when the economy faltered, and the economy did not falter as much as it already has. The lowest quarter in that period was over 1% GDP growth, not minus 1.4%.

This time, unliked all others, the Fed is facing the inflationary battle of its lifetime due to its own grossly misguided policies, and the current drop in sentiment for scale looks much more like the plunge that preceded the Great Recession than like the dip in 2011. So, hang on because sentiment — how you and I and everyone else on average feel — is going to get a whole lot worse going down the hills before us as the Fed attempts the greatest tightening in the history of the world.

What the graphs say to me is that everyone is feeling it, even while few are openly acknowledging it. Trust your gut on this one. The graphs show nearly everyone’s gut from — CEOs to floor sweepers — is feeling a downturn they don’t want to admit out loud.

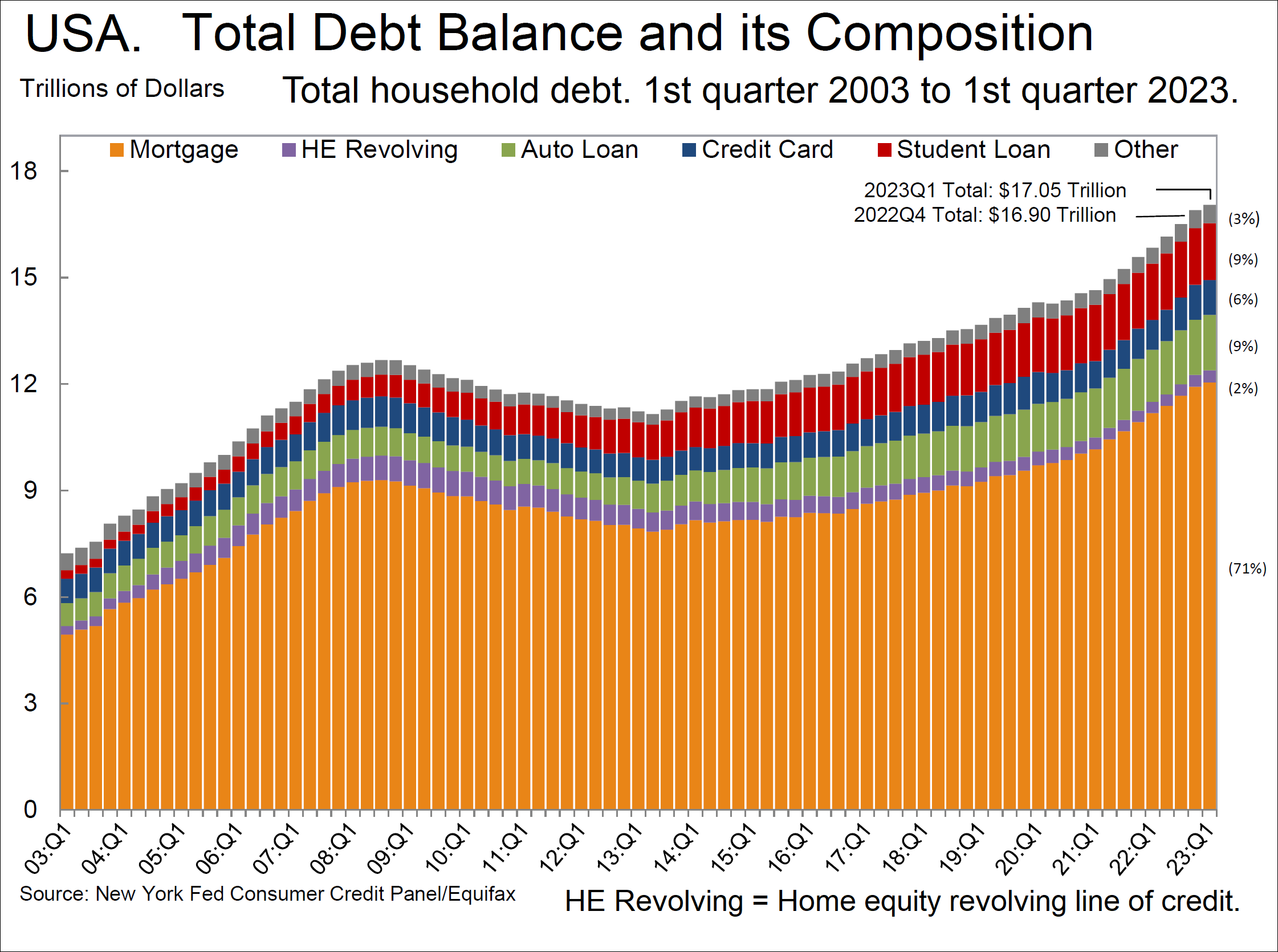

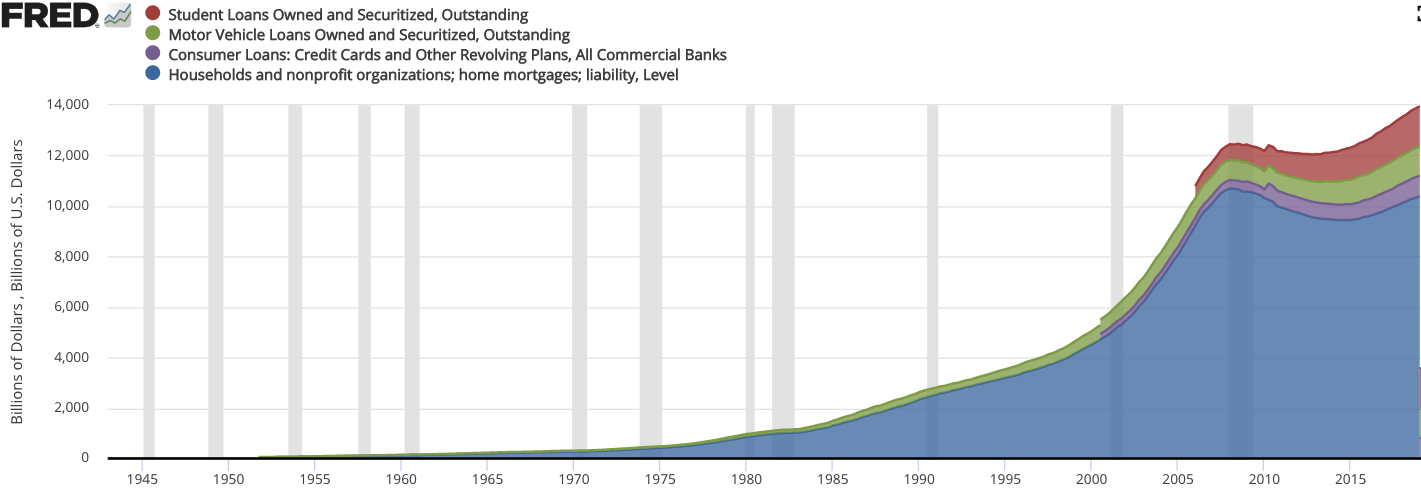

That’s the exploded view. On the longer scale, that looks like this:

Clearly, this unprecedented mountain of consumer debt, which I mentioned in my list, leaves us far less resilient to withstand the Fed’s plan to rapidly raise interest rates in an already badly flailing economy and simultaneously start sucking money out of the economy in June. It’s a suicide pact.

Imagine you are going to ski down that mountain of debt from its ultimate summit and then fly off the lower summit like it’s a ski jump … and for scale you’re that little blip to the right of the jump. It’s going to be a heck of a leap! Better pack on the bubble wrap, Buttercup, because you’re about to jump off the Everything Bubble!