Young investors are taking on personal debt to invest in stocks. I have not personally witnessed such a thing since late 1999. At that time, “day traders” tapped credit cards and home equity loans to leverage their investment portfolios.

For anyone who has lived through two “real” bear markets, the imagery of people trying to “daytrade” their way to riches is familiar. The recent surge in “Meme” stocks like AMC and Gamestop as the “retail trader sticks it to Wall Street” is not new.

It wasn’t long after the turn of the century that “day traders” learned the harsh lessons of valuation and bullish extremes. The bull market of the 90s sucked in retail and professionals alike. It was then Jim Cramer published his famous list of “winners” for the decade in March of 2000.

A recent study by Magnify Money shows that while “this time seems different,” some things remain the same.

Takes Money To Make Money

“It takes money to make money, or so the saying goes. But if you don’t have money to invest, should you take on debt to try to make more?” – Magnify Money

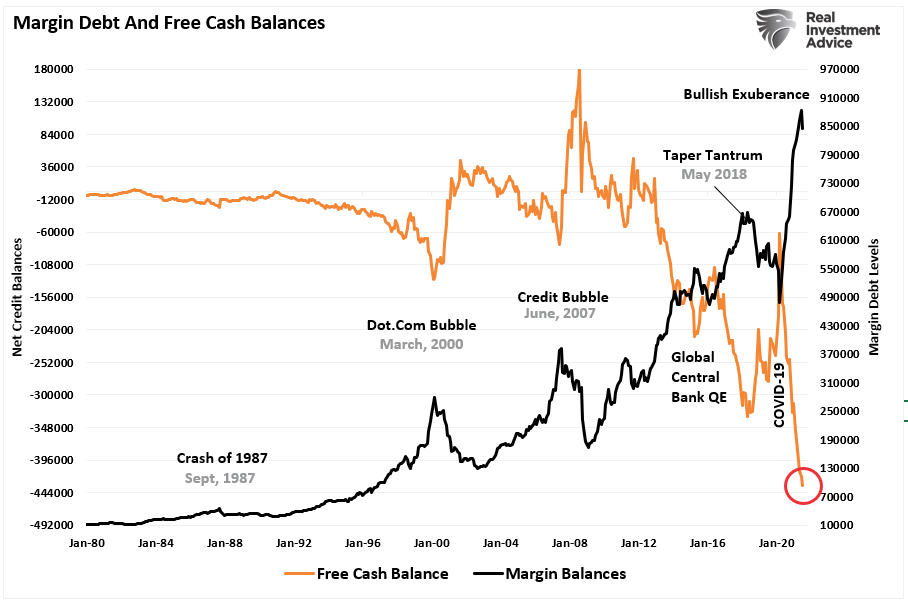

Since the “Pandemic Shutdown,” investors piled into equities. In fact, equity inflows through the first half of 2020 are a record. However, this was not a record by a little, but rather magnitudes above anything seen in the previous history.

Of course, given that discretionary incomes haven’t risen much since the pandemic lows, the money came from successive rounds of “stimulus” payments and, not surprisingly, leverage. As shown, margin debt is near the highest level on record, and “free cash balances” are the lowest.

Of course, the problem with margin debt is that you can only borrow ~50% of the account’s value (depending on the underlying collateral.)

So, when individuals run out of the ability to margin their account, where do they pull from next?

Gen Z’ers Lead The Charge

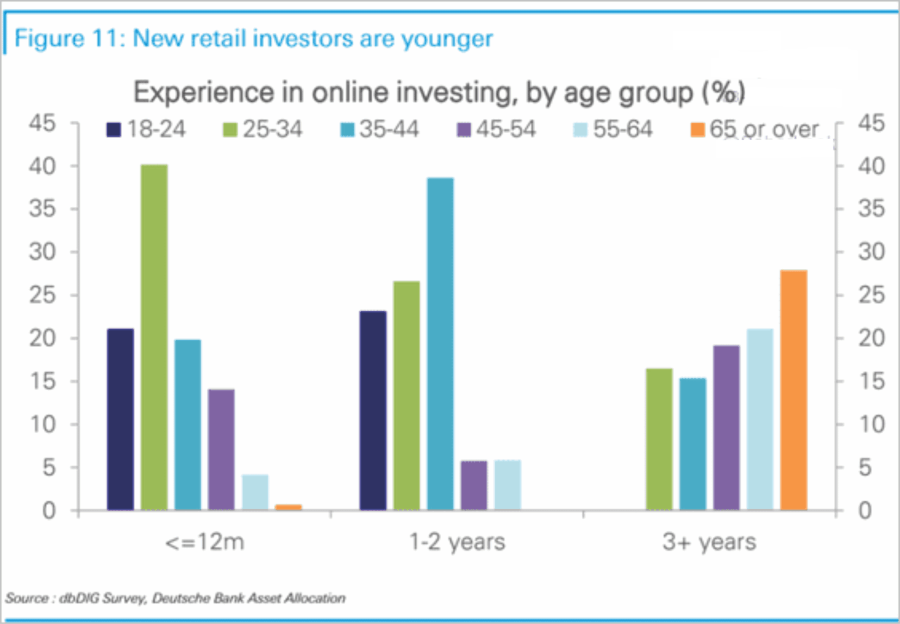

According to Magnify Money’s survey, out of the 40% of investors that took on debt to invest, Gen Z’ers lead the charge. Here are the survey findings:

- Many consumers have taken on debt to invest, with Gen Zers leading the charge. 40% of investors said they have taken on debt to invest. This includes 80% of Gen Zers, 60% of millennials, 28% of Gen Xers, and 9% of baby boomer investors.

- Personal loans were the most popular choice for those who took on debt to invest. Borrowing from friends or family came next. 38% of those who went into debt to invest took out a personal loan, while 23% borrowed from friends or family.

- When it comes to taking on debt to invest, many went big. Of those who took on debt to invest, nearly half (46%) borrowed $5,000 or more.

- Saving for the future was the biggest motivator among indebted investors. 37% went into debt to beef up their retirement plan. Others wanted to buy a specific stock (32%) or participate in day trading (31%).

- Should you invest when you have debt? Americans were split almost down the middle. 49% said yes, because it’s important to build wealth for the future, while 51% said no because people should pay off debt before investing.

- Most said taking on debt to invest won’t be a one-time occasion. Of those who previously took on debt to invest, 61% would do it again and 33% would consider it.

As we have stated before, one of the significant benefits of a “bull market” is that it “forgives” investing mistakes. Investors have taken on personal debt, and according to the survey, would do it again because the result has been profitable.

The problem comes when it isn’t.

All Debt Is Not Equal

When you dig down into the survey, you find that investors taking on debt to invest has long-term consequences.

While I don’t condone speculating “on margin” in an investment account, the debt gets collateralized by the underlying holdings of the account. During a “bear market,” investors are forced to cover their margin debt by selling the underlying securities in the account. If a liquidation event occurs, the WORSE thing that happens to the investor is they lose everything in that account. In most cases, the liability to the individual ends there.

However, individuals are now taking on debt that can have life-altering consequences. As shown in the survey, many took out personal loans or went into credit card debt.

The disadvantage of personal loans and credit card debt is that when the portfolio loses a substantial chunk of its value, it does not get forgiven. Unlike margin debt, that gets tied to the investment account, personal debt, home equity lines, and credit card are with you “forever.”

Therefore, when the crash eventually comes, the individual loses their capital but gets left with payments plus interest for the term of those loans. For a credit card, that payment could well impact an individual for 40-years or more if only paying the minimum amount.

Such an outcome can alter the course of a young person not only in the near term but for most of his productive years.

Lot’s Of Confidence

As we discussed in“Long On Confidence:”

“It should not be surprising we see such rampant ‘speculative’ behavior in the markets. After a decade of monetary injections, investors believe there is an ‘insurance’ policy against losses. This insurance policy is most commonly known as the ‘Fed Put.’

Since the ‘Fed Put’ began following the ‘Financial Crisis,’ it is primarily young investors lulled into that complacency. Armed with only a couple of years of investing experience and a fresh ‘stimulus’ check, the ‘casino’ is open.”

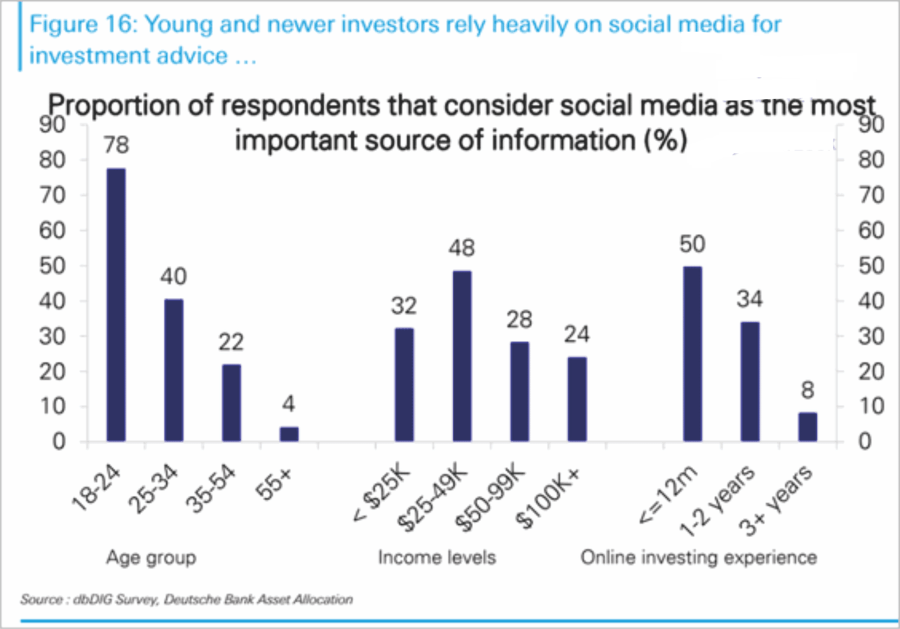

One of the most troubling aspects of where individuals are getting their investing guidance. The youngest and least experienced investors use social media as the “most important” source of information. Considering most social media users are the younger generation, this is the very definition of the “blind leading the blind.”

Jason Zweig summed up the problem with this very well:

“As surely as the sun rises in the east, promoters will be touting these returns. A small-stock fund manager who’s up 40% over the past year can hype that gain in ads and on social media; 40% is a big, beautiful number! Only by reading the fine print would you be reminded that a 40% return underperformed the average by more than 10 percentage points.

You knew I would tell you this but I’m saying it anyway. These returns won’t last indefinitely. Enjoy them while they last, but you’d be crazy to count on such giant gains becoming common.”

The biggest problem for most young investors is the lack of research on the stocks they buy. They are only buying them “because they were going up.” However, when the “season does change,” the “fundamentals” will matter, and they matter a lot.

Such is something most won’t learn from “social media” influencers.

The Most Stupid Of Reasons

“Many people taking on debt to invest have their eye on the future. More than a third reporting they did to invest in a retirement plan. The stock market is the other major motivator, with buying a particular stock and day trading following closely behind as reasons for taking on debt. One in 10 investors said they took on debt to buy cryptocurrency.”

Going into debt to “save” is a terrible idea.

In 2000 and 2001, I spent most of my time working with individuals as a debt counselor more than a financial advisor. Not surprisingly, the crash in the stock market left many individuals with a lot of personal debt and no assets with which to pay it off.

While creditors are more forgiving today of bankruptcies and poor credit, such will still keep younger individuals from advancing in life as expected.

After more than a decade of a strong bull market, investors are once again lured into the financial markets, believing it is a “can’t lose” opportunity.

As Ray Dalio once quipped:

“The biggest mistake investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was a good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.”

Investing is a game of “risk.” It is often gets stated that the more “risk” you take, the more money one can make. However, the actual definition of risk is “how much you will lose when something goes wrong.”

Following the “Dot.com crash,” many individuals learned the perils of “risk” and “leverage.”

Unfortunately, for Gen-Z’ers, such is a lesson that is still waiting to get learned.