Wolf Richter wolfstreet.com, http://www.amazon.com/author/wolfrichter

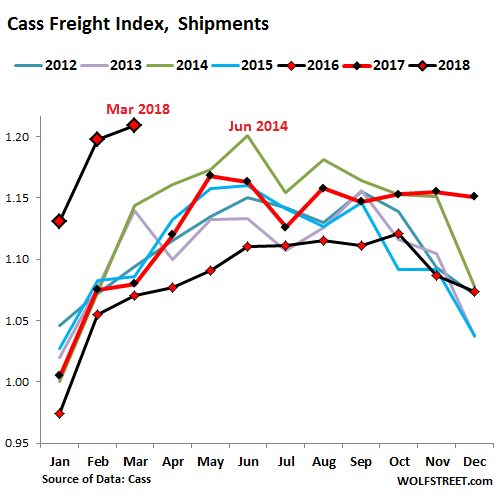

Shipment volumes in the US by truck, rail, air freight, and barge combined surged 11.9% year-over-year in March, according to the Cass Freight Index. This pushed the index, which is not seasonally adjusted, to its highest level for any month since 2007 and for any March since 2006:

After the US transportation recession in 2015 and 2016, the industry was recovering at an every faster pace. In the chart above, note how the red line (2017) outpaced the black line (2016). And 2018 has turned into a transportation boom. March is normally still in the slow part of the year, but this March blew past even June 2014, the banner month since the Financial Crisis!

“Volume has continued to grow at such a pace that capacity in most modes has become extraordinarily tight,” Cass explained. “In turn, pricing power has erupted in those modes.”

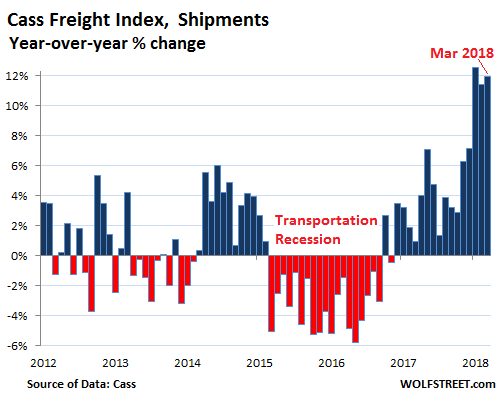

The chart below shows the year-over-year percentage changes in the index for shipment volumes. Note the double-digits spikes over the past three months:

The index, which is based on $25 billion in annual freight transactions, according to Cass Information Systems, covers all modes of transportation — rail, truck, barge, and air — for consumer packaged goods, food, automotive, chemical, OEM, and heavy equipment but not bulk commodities, such as oil, coal, or grains.

This kind of surge in volume has consequences in this cyclical business. During the “transportation recession,” orders for heavy Class 8 trucks collapsed, triggering lay-offs and throughout the truck and engine manufacturing industry. The opposite is now the case: Orders for heavy trucks are hitting records.

Earlier in April, FTR Transportation Intelligence reported that in March, orders for North American Class 8 trucks had surged 103% year-over-year to 46,300, the third highest on record. And orders for the first quarter “were the largest totals of any quarter in history”:

Fleets are attempting to add capacity as fast as possible in a dynamic market. Some OEMs had exceptional order months as fleets scramble to lock in order slots for this year.

The current capacity crisis may be the worst ever. Capacity is extremely tight and expected to remain this way for months. Fleets need more trucks to handle huge freight demand and continue to order trucks at record setting rates. OEM 2018 build slots are quickly filling up.

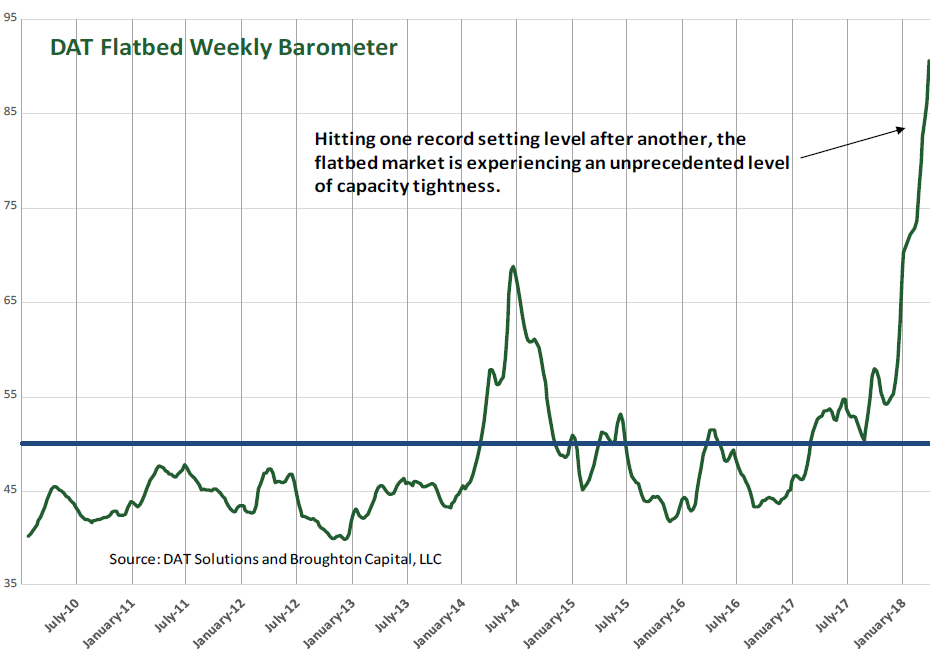

Freight growth continues to climb at a rapid rate. The vibrant economy is pushing dry van and refrigerated van loads to elevated levels and renewed oil drilling is generating a tremendous amount of flatbed freight.

Concerning this demand in the flatbed market, Cass provides an astonishing chart of the DAT Flatbed Barometer that is “hitting one record-setting level after another,” as this end of the market is “experiencing an unprecedented level of capacity tightness”:

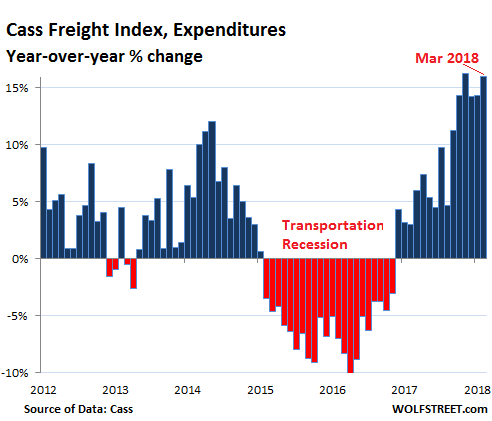

With shipping volumes surging and capacity getting tight, pricing power among transportation companies has “erupted,” as the report put it, and freight rates have increased and the total amount spent on shipping has soared. In March, the Cass Expenditure Index – which tracks the amounts spent on freight by rail, truck, barge, and air, and includes fuel surcharges – soared 15.6%, the sixth month in a row of double-digit increases:

The price of diesel fuel was up “as much as 75%” year-over-year in 2017, and the fuel surcharges, which are included in the index, contributed to the increase in expenditures. But the report cautions: “That said, the year-over-year increase attributable to fuel is now diminishing (up an average of 17.8% on a year-over-year basis in March),” and so the more recent increases in the expenditures index is also due to “pricing power of truckers and intermodal shippers.”

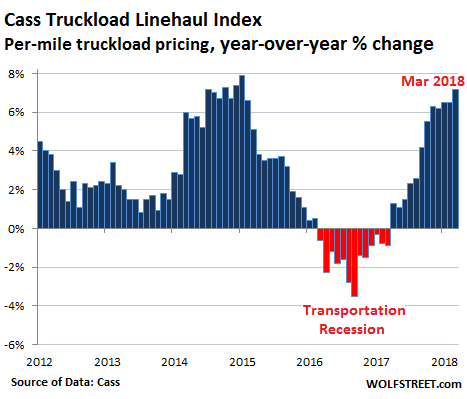

This is confirmed by the Cass Truckload Linehaul Index, which tracks per-mile truckload pricing and does not include fuel – and is therefore not impacted by fuel-price increases – rose 7.2% in March compared to a year ago, the largest increase since January 2015.

Similar trend in shipments by rail: The Association of American Railroadsreported that in March US railroads shipped 6.5% more containers and trailers (intermodal) than in March last year.

Transportation is a boom-bust business. This type of demand, capacity constraints, and pricing power causes transportation companies to increase capacity – hence the record Class 8 truck orders. This will ultimately cause overcapacity to set in, as it always does, and if this coincides with demand that might have peaked by then, the cycle starts all over again. But until then, the boom is on, and prices are rising and capacity is tight, in an environment where inflation is already being pushed up by other factors.

Inflation day didn’t disappoint on inflation day. And “Underlying Inflation” was hottest since July 2006. Read… Fed Warns Markets: Don’t Get Spooked about Coming Spike in PCE Inflation